Abstract

District (pargana)-level land revenue administration in late-Mughal south Gujarat was run mostly by Hindu and Jain family firms which operated within a multilingual environment featuring Gujarati and Marathi as well as Persian. Similar arrangements continued under early East India Company control but, by the 1820s, the British had done away with land-revenue family firms and their contextual multilingualism, replacing them with directly-employed village accountants writing only in Gujarati. This article argues that pargana-level officialsâ multilingualism and relative autonomy were not an 18th-century aberration but a key feature of Mughal administration, dislodged with difficulty by the British.

1 The Tax Experts1

In 1773, a couple of months after the British captured the cotton-rich district of Bharuch in south Gujarat, an emissary named James Morley sat down with two local officials, the desÄÄ«, Jamiat Rai, and the majmÅ«Ê¿dÄr, Lallubhai, to elicit a âmore clear and distinct accountâ of all the taxes that used to be levied from the district during the period of the former nawwÄbs (nawabs, lords running semi-independent successor states).2 After two years of negotiations and an expensive seaborne campaign, Morleyâs superiors in Surat and Bombay were anxious to know what they could expect to squeeze from their new possession, but, lacking local knowledge and languages, the British were entirely dependent on resident experts such as Jamiat Rai and Lallubhai to help them assess and collect the revenue. Having fled when Bharuch was invaded, these officials were at the time guests of the ruler of neighbouring Baroda who was unwilling to share them with the British. Morleyâs meeting had taken weeks to negotiate and took place only on condition that the men returned to Baroda after three days. When the meeting finally took place, the two officials were suspicious of the British and of each other and were nervous about the Baroda rulerâs spies.3 The only information Jamiat Rai would share was his schedule of estimated taxes from six years prior, for the year 1766-67.

Jamiat Rai and Lallubhaiâs influence in the âlittle kingdomâ of Bharuch depended on their control of the local information order.4 When the larger edifice of Mughal governance was crumbling in the 18th century, and there were multiple contenders for power over any given territory, some of the most effective operators were those who were able to control and direct information between the military-fiscal entrepreneurs and the peasantry at the district level.5 At the time of Morleyâs meeting, colonial officials were deeply ignorant about how the countryside was governed, despite the fact that the British had been active in the trading world of south Gujarat for a century and a half. It was not only the British who were ignorant of revenue management; the erstwhile Mughal authorities had been wringing their hands for decades as district-level officials became increasingly autonomous and powerful on the one hand and, on the other, more secretive about what they knew.6 As Sumit Guha remarks, âcontrol of records was ownership of powerâ7 and pargana officials were able to manipulate information for three major reasons. First, they were proficient in the prevalent linguistically-organized information order. Persian carried the greatest prestige in this order, but Gujarati, Hindi, Marathi, and English each played their parts along with a plethora of scripts and accounting systems. Pargana officials wielded, or employed scribes who could wield, multiple languages. Second, they were able to control and direct not just the passage but also the legibility of information between languages and genres. By virtue of their state-granted authority, their clerical training, their family business practices, and their Hindu or Jain upper-caste positions, they had access to the courtly texts of literature and epistolography, the legal documents of contracts and decrees, and the commercial language of accountancy, making them accumulators of a vast amount of useful knowledge. The third reason for their ability to manipulate information was their access to âpatrimonialâ local knowledge, âthe deep knowledge acquired by magnates with roots in the villages and the political sympathy which comes from ties of belief, of marriage and from a sense of inhabiting the same moral realm.â8 By switching between linguistic registers and genres, and by strategically proffering or withholding information, they were able to render their activities indispensable yet opaque. The most politically astute of such officials wielded considerable power in these times, in Gujarat and beyond.

Parganas preceded the Mughals. John Richards argued that parganas were the âprimary building blocks of political controlâ in the Indian countryside and often functioned as miniature kingdoms led by local lineages which exerted claims to taxes, tributes, and labor from subordinate inhabitants. From the start of the Mughal empire, the challenge was to manage rivalries between pargana-based lineages and to incorporate them into the hierarchy of the empire. Under the Mughal emperor Akbar in the late 16th century, contiguous parganas were grouped into revenue circles (sarkÄrs) with karorÄ«s, or revenue officials, deputed to survey and measure the fields in each revenue circle for the production of data for revenue assessment. Pargana officials, whether related to the local ruling lineage or not, often retained their powers and received percentages of the revenue and revenue-free grants in return for their services in collecting and recording the revenue. The pargana thus functioned as a âhard-shelled structureâ that the Mughals tried, and only partially managed, to penetrate.9

In a similar vein, East India Company (EIC) officials trying to interpret local governance and adapt it to their needs struggled with pargana politics, in particular the accessibility, languages, scripts, legibility, and categories of record-keeping. The efforts of early colonial officials to decipher revenue records and render them legible went along with their efforts to acquire a predictable, measurable revenue stream.10 Initially they had limited success on both counts, continuing to require the services of district officials to whom they constantly feared losing funds and credibility, but, several decades after Morleyâs initial encounter with Jamiat Raiâs accounts in 1773, the British constructed a system to impose transparency and order on revenue practices. Returning to Bharuch in 1803 after a two-decade-long hiatus when they were forced to give Bharuch up to the Marathas, the Company launched, from 1812, detailed surveys and censuses of all its possessions in south Gujarat âin its attempt to identify the Ricardian rent it believed was its right as sovereign to collect.â11 The linguistic complexity and ambiguity controlled by Mughal-era district officials, the desÄÄ«s and majmÅ«Ê¿dÄrs, and their links to village leaders (pat̤els) were set aside by appointing salaried village-level accountants (talÄt̤īs), to report directly to newly-appointed British district collectors. Prior systems of record-keeping were discarded as inefficient and illegible. Captain Barnewall, the assistant collector of Kheda, said in 1816 that the village accounts kept by pat̤els, or headmen, âwere in most cases framed in a way so complex and unsatisfactory as to be entitled to little or any confidence.â12 In the new regime, talÄt̤īs were required to maintain detailed village registers (moje jarÄ«f) as well as kalambandhÄ« volumes (from Persian qalambandÄ«, signed document or agreement) to be stored in district record offices.

There was little multilingualism or opacity about the jarÄ«f or kalambandhÄ« books.13 Ever since they were produced, they were referred to as âvernacularâ records, which in this context meant that they were written in the Gujarati language in the Nagari script. While I have not examined the kalambandhÄ« records of Bharuch, should they survive, there is one survey of Kajipura village from Bharuch district in 1820, written in Gujarati and annotated in English, demonstrating the language, script, and categories of information sought by British surveyors at this point, that I will examine closely in the latter part of this article. The survey of Kajipura demonstrates that by elevating village accountants and their Gujarati records and making them directly subservient to British collectors, the British effectively snuffed out the multilingual, cryptic, âpatrimonialâ authority of late-Mughal pargana officials such as Jamiat Rai and Lallubhai and imposed a tidy, utilitarian order on revenue practices. What changed between 1773 and 1820 that allowed the British to penetrate and overhaul the hard-shelled pargana? The transition from Jamiat Raiâs enigmatic accounts in 1773 to the âvernacularâ jarÄ«f book of Kajipura in 1820 was not a mere bureaucratic reorganization: it offers an index to the political, legal, and linguistic shifts that accompanied the establishment of British rule.

2 Jamiat Raiâs Account Books

Writing about India in the late 18th century can be tantalizing. The fact that a lot of material survives seduces one into thinking one can reach back and figure out almost anything. After I read Morleyâs letter to his superiors in Bombay, containing tables of local revenues in English, I immediately re-read it to see if he described Jamiat Raiâs account book in any detail. To my disappointment, all he said was âI have the Honour to Enclose you Sundry Papers containing the Informations I have received relative to the Broach Revenues.â14 Like most other non-English correspondence and documents of the era, Jamiat Raiâs account books were not preserved in the Companyâs archives. I do not know if Morley ever saw them. Nor do I know what language they were in.

In the late 18th century, as the Mughal empire gave way to successor states and European trading companies, Mughal revenue practice was becoming disarticulated from actual Mughal government. One location where such separation was taking place was Bharuch, a former Mughal revenue unit in south Gujarat ruled for half a century until 1772 by a lineage of nawabs, descendants of a Mughal-appointed jÄgÄ«rdÄr (land-right holder), who claimed a degree of independence from the Mughals while maintaining Mughal-style political and revenue-gathering practices.15 A desirable black-soil territory situated on the north bank of the Narmada river where it opened to the sea, Bharuch was made wealthy by cotton, ghee, and manufactures. It had a flourishing and taxable port and was a key way-station on the road from north India to Surat. Since 1756, the nawabs had shared their revenues (and sovereignty over Bharuch) with the neighboring Marathas of the Gaekwad family. When the British captured Bharuch in November 1772, they retained much of prevalent Mughal administrative convention, going to considerable trouble to retain the principal officials who ran its land revenue infrastructure.

Of the pargana-level officials involved in the assessment and collection of land revenue in Bharuch, south Gujarat, the most prominent were the majmÅ«Ê¿dÄrs, keepers or auditors of tax records, and the desÄÄ«s, in charge of the revenue assessment, jamaâ.16 Both offices had been active in Gujarat since the reign of the Mughal emperor Akbar (1556-1605), if not earlier. MajmÅ«Ê¿dÄrs and desÄÄ«s in Bharuchâand elsewhere in Gujaratâreceived revenue-free (inâÄm) grants of land in return for their services and were expected to serve as checks and balances on one another. In practice, the actual roles of majmÅ«Ê¿dÄrs and desÄÄ«s were not clearly distinguished: the two officials tended to work out a competitive coexistence.17 Whether or not these positions were originally designed to be hereditary, by the 1760s they were held by two Hindu families in Bharuch who functioned as family firms, presenting themselves as embodiments of the state to the peasants while also functioning as private corporate entities working in pursuit of their own interests.18 I have written previously that the proprietors of land revenue family firms were not strictly government employees, in that their income and influence did not derive exclusively from state patronage. Nevertheless, they represented the state (sarkÄr) to other entities such as farmers, moneylenders, and zamÄ«ndÄrs.19 It was their sarkÄrÄ« âstate-nessâ that gave them the credibility to function. As tax assessors and auditors, the desÄÄ« and majmÅ«Ê¿dÄr firms were the points of contact between the (transferable) Mughal office-holders (jÄgÄ«rdÄrs) and (stationary) village officials and other functionaries. The British inherited their servicesâand networksâfrom the Mughal-style administration of the nawabs.

After their meeting with Morley, and during the subsequent decade of British control over Bharuch (1772-83), Jamiat Rai and Lallubhai held on to their local knowledge; there is no evidence that they ever gave up their account books for British inspection. Lallubhai in particular worked closely with British officials, virtually resuming his position as the Bharuch majmÅ«Ê¿dÄr, but did not allow close scrutiny of his methods, a posture that caused chagrin among certain British officials who harrumphed about his outsize influence and saw his evasiveness as incapacity. When, in 1776, William Perrott embarked on the first comprehensive survey of Bharuch, grumbling that the desÄÄ«s and the majmÅ«Ê¿dÄrs were so ignorant of the lands they governed that they had ânever seen an account of the land said to belong to each,â part of his irritation was at local officialsâ ready access to information that was impenetrable to him.20 Even when the British obtained some of the information within these booksâas Morley didâtheir language, script, and classification schemes could remain opaque. If I have not been able to find Jamiat Raiâs accounts, it is by design. The land revenue family firms did not intend for outsiders to see their records.

3 Mughal and Pre-Mughal Languages of Revenue

As a pargana-level revenue official in a Mughal successor state that had formerly been a Mughal revenue district, did Jamiat Rai write in Persian or did he keep accounts in Gujarati? If the former, did he use Mughal siyÄq notations?21 If the latter, what script did he useâthe Nagari with which we associate Gujarati today, or one of the commercial scripts used by Gujarati business people? Further, what was the nature of his literacyâdid he personally write in his account books or did he dictate to a clerk? In the absence of his records, historical practice will have to provide clues.

Under the Chaulukyas of Gujarat (ca. 940-1244), revenue records were likely to have been in Sanskritâthe âvernacularâ or âJainâ Sanskrit of medieval textsâor in early Gujarati.22 Once Gujarat came under Delhi sultanate control in 1297, revenue records may have been transmitted in Persian, but probably continued to be recorded by local Hindu or Jain officials in Sanskrit or Gujarati. Letter templates preserved in an undated but probably pre-15th-century compendium of form-letters, Lekhapaddhati, were mostly in vernacular or business Sanskrit, some containing Gujarati fragments and phrases.23 This dual linguistic system likely persisted under the Gujarat sultans in the 15th and early 16th centuries. Pre-Mughal stone inscriptions in Persian, recording donations, grants, or transactions, often had a few lines in Gujarati.24

In north India, a few surviving Persian-Kaithi documents suggest a phase of documentary bilingualism that was probably the norm for the same period.25 In the early 16th century, the Afghan ruler Sher Shah Sur appointed two sets of district officials, one to maintain records in Persian (fÄrsÄ«-nawÄ«s) and the other in the local language, Hindi (hindÄ«-nawÄ«s), a measure which Najaf Haider sees as an important effort to expand âpolitical and fiscalâ control at the district level.26 Sher Shahâs increased emphasis on Persian as the language of upper administration continued under the third Mughal emperor Akbar (r. 1556-1605). Sometime between 1582 and 1584, Raja Todar Mal, senior financial administrator to Akbar, decreed that all administration was to be in Persian and in the âIranian style,â and to be staffed by a cadre of Iranian and Hindu clerks, secretaries, and scribes.27 It is generally accepted that after this decree, Persian became the dominant language of government throughout the Mughal realm and persisted in that capacity into early colonial India until the British made concerted attempts to replace it with English from the 1830s onwards.28 While Persian became the language of court and the Mughal elite, there is evidence that Persian language skills, in the form of âpragmatic literacyâ or âPersographia,â came to be found even among village-level revenue officials.29 The vast bulk of surviving official documentation from the directly-governed parts of the Mughal empire, ranging from royal or courtly orders (farmÄns) to deeds of sale, is in Persian. Nevertheless, most Mughal officials and scribes continued to be multilingual.

Although Persian became the dominant language of Mughal documentation, it is unlikely that it was the only official language, especially in sub-provincial revenue record-keeping. Insisting that Persian was the only language of government is a way of asserting that the Mughal stateâand its chosen language, Persianâbecame thoroughly indigenized and penetrated deep into Indian society.30 If Jamiat Raiâs books were in Persian, they would be evidence of the Mughal empireâs reach. If they were in Gujarati, in a commercial script, they could be evidence that the dominant Mughal language, and thereby the Mughal state, remained external to certain aspects of Indian political life. An exclusive emphasis on Persian risks masking a lively and context-sensitive documentary multilingualism that persisted through the 17th century and into the 18th. Perhaps we should cast the net wider; important new work is now challenging the notion of archives as spatially defined repositories and suggesting, instead, that we imagine more capacious circumstances of documentary production and memorialization.31 Certainly, the futile search for large colonial-style âofficialâ archives from the pre-British era has meant that household-held records, whether in the possession of land right-holders or information-specialist family firms such as those of Jamiat Rai and Lallubhai, have remained largely unseen and unremarked.

In advance of thorough study, it is premature to assume that district-level revenue records were invariably in Persian. In the Mughal heartlands of north India, there is plenty of evidence that âHindiâ record keeping was not abandoned. Of the large collection of orders and sale deeds from Vrindavan, a significant proportion is in Braj, in the Nagari script, or in Braj and Persian.32 More pertinently, an appointment order translated by J.F. Richards enjoined provincial officials to collect in each season âthe account papers of the several villages of every subdistrict (pargana), and translate them into Persian,â and then to send the translated accounts on to the emperor.33 The author of Richardsâ early 18th-century administrative manual evidently did not expect village records to be kept in Persian. Outside directly-governed Mughal territories, revenue records were often not in Persian. In the Rajput kingdoms, for instance, revenue records were kept in various local languages, albeit deeply imbued with the Mughal stateâs Persian vocabulary.34 The Adil Shahi rulers of Bijapur used written Marathi for local government, including revenue collection and judicial matters, as did the Nizam Shahis. The Qutb Shahis of Golkonda often issued bilingual (Persian and Telugu) edicts, while local revenue papers were largely in Telugu.35

In Gujarat, as in other parts of the Mughal empire, most of the official paperwork that has been archived and catalogued in public collections is in Persian, although there are few studies thus far of original correspondence and documents bearing seals, signatures, and other marks of having passed through official hands, still less of officialsâ revenue records.36 Nevertheless, it is clear that certain genres of official documents could be in languages other than Persian. A set of land records from Ahmedabad, for instance, suggests that a proportion of sale deeds of land (khatapatras) were in Gujarati, in the Nagari script, while a few were in Persian.37

Outside the state bureaucracy, Gujarati business firms kept records in Gujarati, and had done so since medieval times. A few surviving papers from the Geniza records suggest early commercial use of Gujarati, as do 17th-century inscriptions from Socotra.38 Hunḍīs, or promissory notes, and account books, were often in Gujarati. Some correspondence and paperwork was carried out in commercial scripts, such as versions of the MahÄjanÄ« script used throughout northwestern India.39 For the 18th century, an extraordinary collection of documents belonging to a Baroda-based banking firm gives us some idea of how documents were organized on multilingual lines (or were themselves multilingual). The Haribhakti papers include account books, ledgers, deeds, state documents, and correspondence from the early 18th to the early 20th century.40 Correspondence was often in Persian, while documents such as account books, most of which were not intended for the eyes of outsiders, were in Gujarati or Marathi, written in the MahÄjanÄ«-Muá¹á¸Ä« or Moá¸Ä« script, two of the many commercial scripts of western India.41 Yet other documents were in a Nagari-script rendering of Gujarati. Accounts were mostly in the Gujarati system, rather than the siyÄq accounts mandated by the Mughal bureaucracy. The collection of Haribhakti papers remains in need of thorough study, but preliminary surveys confirm the multilingualism of the familyâs transactions.

The welcome growth in the literature on Mughal-era revenue officials, scribes, and clerks has brought out the challenges in drawing precise distinctions between these occupations. It is clear that there were significant variations of status, function, and linguistic ability among such individuals, even those who bore the same titles. While some revenue officials kept their own books, others delegated record-keeping to specialist scribes.42 Certain Persian-trained clerks achieved renown for the literary merit of their writings, while others possessed only rudimentary skills in copying, letter-writing or accountancy.43 Some scholars have attempted to nuance these distinctions with compound terms such as âscribal-mercantile adjuncts,â âmanagerial elites,â âproto-bureaucrats,â and âportfolio capitalistsâ for the kind of revenue officials and local magnates who had been entrepreneurial in expanding their repertoires and political influence while others have chosen to use self-identifiers that appear in the texts.44 In spite of the careful work done thus far, it is not always possible to assess an individualâs literacy or numeracy based on their job title or to figure out what languages they actually used.

For the context I have described here, more work needs to be done to establish whether officials such as Jamiat Rai possessed scribal and accountancy skills themselves or whether bookkeeping and correspondence were carried out by clerks in their employ. The ability to speak a language did not, at this time, necessarily mean literacy but even a basic or functional grasp on the language allowed elite men to guide the productions of specialist munshÄ«s.45 From another source I know that Jamiat Raiâs colleague and rival Lallubhai knew multiple languagesâHindi, Marathi, and Persianâin addition to his native Gujarati, and that he understood some English. He prized Persian literature and âthose who revealed literary talent.â In the 1790s, he commissioned a compilation of official Persian letters whose name, MajmÅ«âa-yi dÄnish or compendium of wisdom, was a play on his title of majmÅ«âdÄr.46 The MajmÅ«âa-yi dÄnish contains a number of letters sent by or to Lallubhai, suggesting that he, like other officials of his rank, communicated with jÄgÄ«rdÄrs and other functionaries of the Mughal order through correspondence in Persian dictated to munshÄ«s. I know much less of Jamiat Raiâs linguistic talents, but, considering he was of comparable status and background, it is fair to imagine he was also multilingual, with some grasp of Persian in addition to Gujarati, Marathi, and Hindi. While bureaucratic correspondence was in Persian (or in Marathi, if dealing with the Marathas), dealings with village-level officials including pat̤els (village headmen), talÄt̤īs (accountants), and mehtÄs (scribes) must have been in Gujarati, whether verbally or in writing. If we are to believe William Perrott who noted in 1776 that the district officers rarely visited the lands whose taxes they administered, communication between the Bharuch-based desÄÄ« and majmÅ«âdÄr and the villagers must have been by couriers carrying verbal or written missives in Gujarati.

Having conducted negotiations with the nawab for a year before this meeting, Morley was already acquainted with Lallubhai, and the three men are likely to have had enough common linguistic resources to communicate verbally or had interpreters or scribes to help. As Morley does not mention reading or copying the records personally, perhaps Jamiat Rai or his munshÄ« read the accounts aloud, including the long lists of figures. If so, Morleyâs summary is a transliteration of what he heard followed by a translation into English, which would mean we are at several removes from the written contents of Jamiat Raiâs books. As the language of Jamiat Raiâs books cannot be determined, we now turn to the content he shared with Morley for clues to the linguistically-inflected organization of revenue information.

4 Revenues, Language, and the Law, 1760s

The British had turned their sights on Bharuch because of its reputation for wealth, largely from land revenue and customs dues, and, at the start of British rule in 1772, the newly captured territory seemed full of promise. After the conquest, expectations were scaled down. The Bharuch expedition had been sold to the Companyâs directors based on a wildly optimistic expectation of 7,00,000 rupees of annual returns. Now, they were willing to accept a more modest estimate of about Rs. 3,20,000 from a year of good harvest. When, in January 1773, Morley sat down with Lallubhai and Jamiat Rai to elicit a summary of the taxes that used to be levied from the district during the period of the late nawabs, he was hoping that it was not already too late to assess and collect taxes on the past seasonâs crops.

As we shall see, Morleyâs report shows that local land-revenue practice encompassed both Persian and Gujarati vocabulary, comprising normative Mughal-Persianate legal terms as well as indigenous Gujarati jargon. First we learn that the Bharuch territory contained 179 villages, of which eight belonged entirely to the Gaekwads.47 Three were deserted. Nine of the 179 villages were alienated to prominent local individuals. These included the majmuâdÄr Lallubhai and the desÄÄ« Jamiat Rai who each possessed an inâÄm village, paying no taxes to either the Gaekwads or the nawab. The remaining seven villages were given in hereditary waáºÄ«fa grants to Muslim clerics who paid no taxes to the nawab but did pay the Gaekwads.48 Such tax exemptions were reported in the Mughal stateâs Persian vocabulary: inâÄm, or gift, waáºÄ«fa, or stipend. Leaving aside the villages that were exempted or deserted, or which belonged to the Gaekwads, Morley listed 159 villages that paid regular land revenue, the proceeds of which were divided between the Gaekwads and the nawab in the proportion 3:2.

Jamiat Raiâs schedule of estimated taxes for 1766-67 amounted to Rs. 4,03,334, three annas and one paisa.49 Each village paid two kinds of taxes: âain and vero (âverrawâ in the original). Morley does not explain what âain is but we may take it to mean ârealâ or âtrueâ land revenue, abbreviated from the Persian âain jamaâ or âain al-mÄl. âAin jamaâ was a commonly-used term used for the statutory, Mughal-Persianate estimate of land revenue (jamaâbandÄ«), or for the gross realized land revenue.50 In certain contexts, âain jamaâ could comprise two parts: first, âain al-mÄl or âain mÄl, the assessed land revenue, and second, bÄqÄ« (P) or khot̤ verÄ (G), additional cesses to make up for any losses in preceding years.51 In either case, Jamiat Raiâs (or Morleyâs) âain seems to represent the traditional share of the produce the sovereign elicited from the subject. In Bharuch, the sovereign was dual: the nawab and the Gaekwad.

VerÄ (singular vero) were additional dues, charged by the ruler in addition to the basic land revenue. The common, modern, meaning of vero is simply tax or cess, or, as defined in the mid-20th-century Gujarati lexicon BhagvadgÅmaá¹á¸Ì£al, cash (rokaḠrakam) charges for government needs levied on farmers over and above land revenue, that could be charged from either individuals or corporate bodies and could include octroi, import and export charges.52 The latter is the sense of vero that appears in Jamiat Raiâs accounts.

Earlier in the 18th century, however, the word verÄ carried a connotation of forced taxes. The word first appears with frequency in the 18th century in the Persian accounts of Gujarat, the MirâÄt-i AḥmadÄ« and MirâÄt al-ḥaqÄâiq, where it is spelt bÄ«vara, and usually means illegal or extra-legal taxes or fines.53 The author of the MirâÄt-i AḥmadÄ« remarked that he had never heard the term before coming to Gujarat, but that, in his day, this forced tax was imposed by courtiers in Gujarat âon various excuses such as differentiation in trade, community, head counting, house counting, etc.â54 From the Mirâat al-ḥaqÄâiq, it appears that verÄ could be imposed not only by rulers but by other powerful individuals as well, such as the banker Khushhal Chand who was instructed to raise a million rupees either through bÄ«vara or from his own firm.55 The term also appears in Gujarati records with much the same meaning, such as in a land deed from 1725 that records that Hamid Khan, the deputy governor (nÄâib subadÄr) of Gujarat, in alliance with the Marathas, had collected three kinds of taxesâkhaá¹á¸aá¹Ä« (protection money), fourfold jÄ«jÄ«o (jizya), and veroâfrom the 84 castes of Ahmedabad.56

As far as I can determine, the terms vero/verÄ or bÄ«vara do not appear outside Gujarat, nor do they appear before the 18th century. Under the Gujarat sultans (1407-1572) several similar such taxes were charged, for porterage, letter-writing, police dues, on stalls selling various commodities, and so on, but, at least as represented in the mid-18th century MirâÄt-i AḥmadÄ«, such taxes were listed under the Persian terms ḥÄá¹£il (realized revenue) or sÄâir (property tax, customs, or octroi).57 In the Mughal system, taxes over and above land revenue were classed as wujÅ«hÄt or bÄb (Persian, plural abwÄb), or, as in an explainer (sharḥ) pertaining to Aurangzebâs farmÄn of 1666, ḥÄá¹£il and muḥtarifa. There were two forms of jihÄt, one set (mÄl-o-jihÄt) closely tied to land revenue and intended for the payment of revenue officials, and the second, sÄâir-jihÄt, including taxes on markets, occupations, octroi, and so on.58 Both sets were included in the jamaâ, the assessed revenue. Additional cesses levied by officials or local landholders that did not appear in the jamaâ included farÅ«âÄt or farÅ«âiyÄt.59 The term bÄb was used for non-agricultural taxes in the Hindu kingdom of 17th-18th-century Marwad, as in other parts of north India.60 In eastern Rajasthan, sÄâir jihÄt was the term commonly used. In the Maratha territories, verÄ-like additional taxes were collectively called, from Persian, siwÄy (or sawai) jamaâ. Meanwhile the âain al-mÄl or jamaâbandÄ«, the assessed revenue, remained constant, and the siwÄy jama could change based on the rulerâs needs.61

There are two possibilities for the origin of the word vero/verÄ. The first is that it is an indigenous Gujarati word linked to Sanskrit vyavahÄra (transaction, business, trade), Sanskrit/Prakrit dvÄra (door, gate), Gujarati vepÄr (trade), or vevÄr (dealings).62 If the term is an indigenous one, it does not appear in early sources. In the predominantly Sanskrit vocabulary of the Caulukyas of Gujarat are several non-agricultural taxes that were functionally similar to verÄ but none that sound similar.63 A second possibility is that it is a vernacularization of farÅ«âiyÄt, a Persian term used in 17th-century Gujarat for âforbidden taxes.â64 If the latter, it is interesting that later Persian writers such as âAli Muhammad Khan, Mithalal Kayasth, and Iâtimad Khan âPersifyâ the Gujarati word vero as bÄ«vara instead of using the Persian farÅ«âiyÄt, a proceeding that suggests vero was an accepted part of Gujarati tax lingo for 18th-century writers.

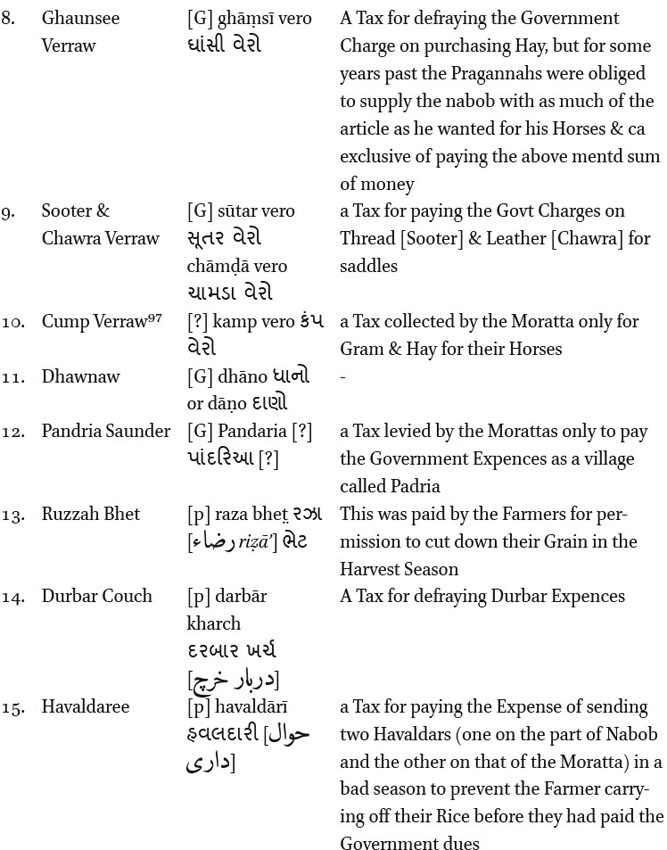

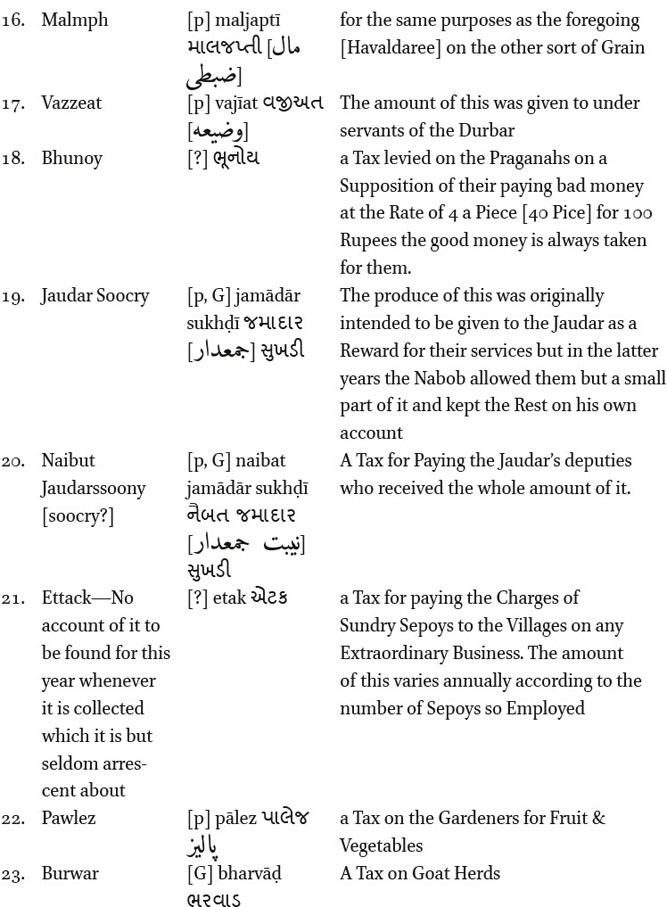

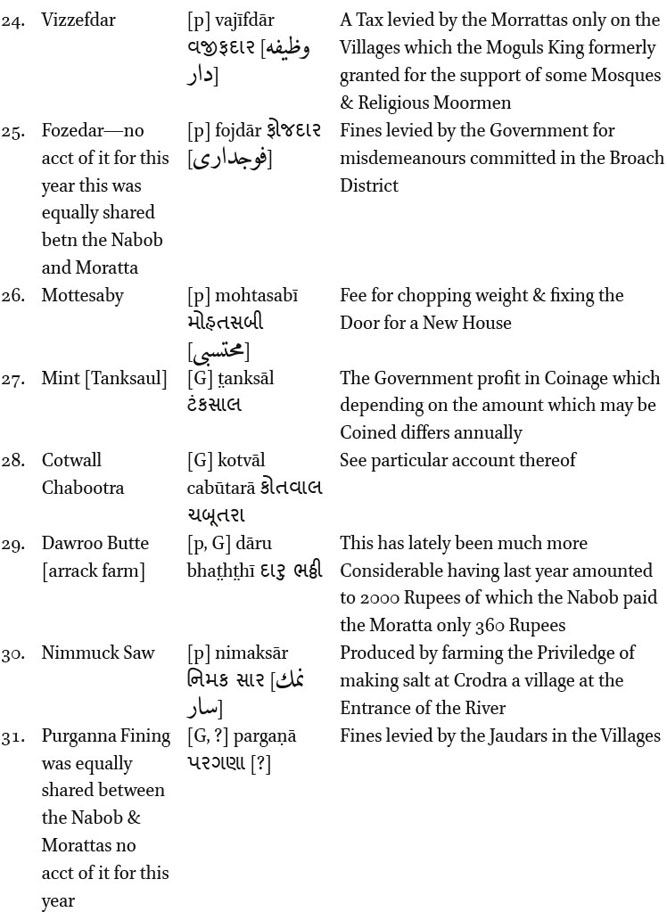

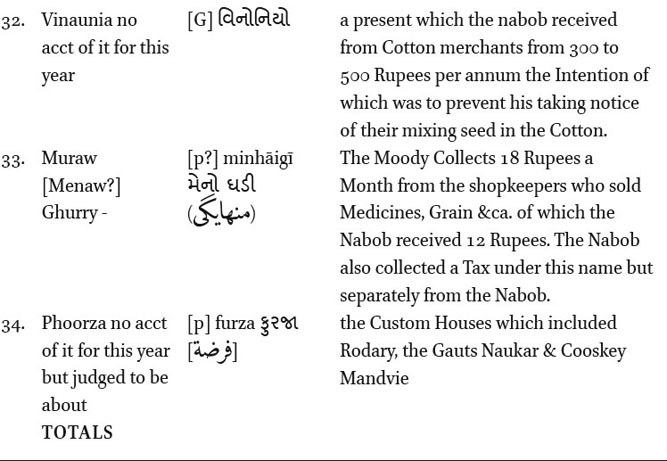

Jamiat Raiâs record for 1766-67 listed no less than 34 kinds of verÄ, dues levied by the nawab in addition to the âain taxes. The proceeds of each were divided between the nawab and the Gaekwads. While the âain taxes were always higher than the verÄ, the latter represented a substantial additional amount from each village, occasionally even up to 95% of the âain.65 Morleyâs list, followed by his helpful glossary, contains 34 kinds of vero of which I can reliably translate 27 (See Appendix 1 for a full translation). Of these, 16 terms include Persianate words, often in compounds with Gujarati terms for taxes, such as: Cummy verraw (kamÄ« (

A few terms were derived from Persian words in common use: Pawlez, or pÄlez, from the Persian for kitchen-garden or melon-field, was a tax imposed on market-gardeners, Phoorza (furza) represented customs dues, and Nimmak Saw (namak sÄr,

The Gaekwads received a 60% share on six of the line items above. âCump Verraw,â âDhawnaw,â âPandria Saunder,â âMenaw Ghiry,â and âVizzefdarâ were levied only by the Gaekwads. Most others were shared equally with the nawab. âKey verrawâ, described as âA Tax which was first levied about 20 years ago and has ever since been continued to reimburse the Govt for the Expenses of Digging a Ditch around a small fort at a Village called Soryareâ was also levied, in that year, only by the Gaekwads. A number of verÄ were designed to pay for gifts or gratuities to officials. There was a tax levied on a festival (âDusraputtyâ or Dasera tax âdefraying the Charge of presents which the Nabob made on the Occasion to the head Jumadar, Patells and principal People of the Town.â67 The kÄrkun pat̤t̤ī used formerly to be levied by the desÄÄ« âto pay for Presents he gave annually to the principal people of Government to engage their Interest in his Favour,â but in late years the amount had gone to the nawab.68

In some cases it is clear who the taxpayers were. It is noteworthy that many of the levies were imposed on relatively low-status professionals such as fruit and vegetable growers, shopkeepers, and goatherds whereas high-status individuals enjoyed tax remissions in the shape of inâÄm or waáºÄ«fa grants.69 Farmers had to pay for permission to reap their grain in the harvest season, and homeowners paid for the privilege of cutting wood and fixing doors in new homes. Arrack and salt production were farmed to the highest bidders who paid taxes for the privilege. The modÄ« or chief grocer collected 18 rupees a month from the shopkeepers, handing over 12 to the nawab and keeping the rest. In other cases, it is not entirely clear who paid certain dues. Taxes were levied (from farmers? townspeople?) for particular government needs, for example the purchase of ammunition, hay, thread, leather, and grain.70 Although the ghÄá¹sÄ« vero was a tax to pay for hay, in recent years the villages had supplied the nawab with free hay for his horses in addition to paying the tax. Certain one-time expenses turned into annual taxes: a levy to pay for digging a ditch around a small fort, levied twenty years prior, had become a regular fee, as had the sonÄ« vero (levied on goldsmiths or gold transactions?), previously levied to help the government in the case of an emergency.

There is no line item for paying regular soldiers in this table. In other words, the basic requirements of military fiscalism must have been borne by the nawab from his regular (âain) share of the revenues. The verÄ paid for additional court and military costs: durbar expenses, for soldiers to be sent âon any Extraordinary Business,â and for policemen (one each to represent the nawab and the Gaekwads) to catch tax defaulters. Of course some of the verÄ no longer went to their original intended recipients; for example, the jamaâdÄr sukhá¸Ä« and naibat jamaâdÄr sukhá¸Ä« originally levied to benefit the military commander and his deputies had in recent years been largely appropriated by the nawab.

Some taxes were devices to keep the wheels of government running. There was a tax to make up for any deficiency in the taxes collected the previous year. There was a tax levied against the possibility that taxes might be paid in âbad money.â Taxes on the mint varied with the amount of coinage minted annually. There was even an amount, between three and five hundred rupees annually, which the nawab received from the cotton merchants, âthe Intention of which was to prevent his taking notice of their mixing seed in the Cotton.â71 Finally, if the nawab and the Gaekwads needed to make presents to each other, additional verÄ would be levied.

If we are to treat Morleyâs notes as accurate, we have a fascinating picture of the nawabâs sources of revenue. He received a âregularâ or âain taxed amount from each village which was based on the jamaâ, the pre-assessed estimate of revenue. In addition, he received the verÄ amounts, which were generally less than the âain amount. Sixty percent of the âain amount and some of the verÄ were shared with the Gaekwadsâwhich suggests the verÄ had been common since the revenue-sharing agreement was made in 1740. Clearly, the âain amounts were insufficient to run the government and to pay its employees and representatives. The verÄ filled in the gaps. If the nawab needed extra money, he would not increase the âain amounts, which were pre-assessed and collected in the old Mughal way. He could simply add verÄ, as he did in 1772 when he was trying to raise money to pay the British for customs dues they insisted were owed to them:

And after a few days he explained the amounts [raqam-i maâmulÄt] on which they had agreed, and asked his relatives and subjects in the city for help. He divided the amount into four parts: one share which he would undertake, the second to be borne by his relatives, the third by the Muslims of the city and the fourth by the Hindus. Thereupon, a huge turmoil rose and the people of the city started to curse [bad-duâa]⦠A command was issued to the administrators to collect a bÄ«vara [verÄ] of gold, so that over three months through a thousand kinds of hardships and tortures and punishments, one assigned share amounting to 35,000 rupees, was collected.72

It is worth considering whether the nawabs deliberately under-assessed the âain. This suspicion is borne out in a letter extolling Nawab Muâazzaz Khanâs policy of keeping land assessments low to enable cultivators to pay their assessed taxes.73 Such a dodge would appear as a gesture of benevolence towards his subjects but it could have two additional functions: to reduce the amount the nawabs were obliged to pay to the Gaekwads (and, previously, to the imperial treasury), and perhaps also to allow for the proliferation of verÄ.

In the absence of imperial regulation, there was little check on verÄ. The nawab couldâand didâimpose additional burdensome verÄ when he needed the money. Officials, such as the desÄÄ«, were authorized to impose verÄ, just as the banker Khushhal Chand was so authorized in 1725. The exaction of extra-legal taxes, whether by state bureaucrats, bankers, revenue officials, or little princes such as the nawabs of Bharuch, was a common practice in late-Mughal South Asia, and was constrained only by the fearâor threatâof reducing future trade and productivity.74 Describing a similar situation in 17th-century Marwar, Divya Cherian remarks that only âcustomâ and resistance from taxpayers could limit such taxation.75 In the 18th century, the levying of ever more extortionate verÄ was a feature of a time when fiscally-challenged new contenders for power, including Mughal-appointed but increasingly autonomous officials, engaged in entrepreneurial revenue gathering.76

The distribution of Persian and Gujarati vocabulary in Morleyâs tables may be read as an index of the relationship between the imperial and the local. The Mughal (Persian) revenue arrangements represented by the âain jamaâ continued to be the indispensable scaffolding for revenue extraction but were inflexible and unsuited for entrepreneurial politics. It was the additional verÄ, acknowledged as commonâif reviledâlocal practice since the 16th century, that facilitated the networks of hierarchy and obligation that kept the empire going and expanded to fuel the new entrepreneurial politics. The two systems were intertwined. Mughal-granted authority to collect the âain conferred on an aspirant the authority to additionally solicit verÄ, which is why 18th-century political entrepreneurs continued to seek charters from the hollowed-out Mughal crown. The relationship between the static âain and the burgeoning verÄ in the 18th century was, on the one hand, a symptom of the increasing disarticulation of the imperial and the local. On the other hand, it was an indication that verÄ were intrinsic to the Mughal system, part of a longer history in which revenue intermediaries exercised functional and linguistic autonomy, using a scaffolding of the mandated Persian terminology while continuing to foster the hierarchical, tributary, and affective relationships suggested by the Gujarati terms. The Persian-Gujarati compound phrases demonstrate these relationships, with Persian terms generally used for offices (jamaâdÄr, kÄrkun) and Gujarati terms for entitlements (verÄ, sukhá¸Ä«, pat̤t̤ī). However, Persian revenue terminology was not imposed on the vernacular Indic world through conquest, as nationalist historiography would have it. The âain (Persian) and vera (vernacular) constituted each other in a distinctively Mughal system.

Further, in Gujarat, there was one significant difference from elsewhere in the empire. Unlike Hindu kingdoms such as the Marathas and various Rajput states that adopted the Mughal Persian terminology for non-agrarian taxes (bÄb, sÄâir jihÄt, sivÄy jamaâ), the term used in the directly-ruled parts of Mughal Gujarat was the vernacular vero. Even if it was a vernacularization of the Persian farÅ«âiyÄt, it was understood by contemporary Persian writers as a Gujarati usage. Correspondingly, whether Jamiat Raiâs accounts were in Gujarati or Persian, in a commercial script, Nagari, or Perso-Arabic, or a mixture, the Persianate vocabulary of Mughal power was uniquely woven through with the Gujarati vocabulary of indigenous capital (vyavahÄra, vepÄr, vero, bÄ«vara).

5 Monier Williamâs Field Book, Village Kajipura, 1820

Almost half a century later, much had changed in Bharuch. In 1782, the British had been forced to give up the district to the Marathas who displayed little respect for the entrenched land-revenue firms and forced them to bid to farm Bharuchâs revenues. Lallubhai, who fell into debt trying to raise money for his bid, was thrown into prison and died in 1800.77 The British regained Bharuch in 1803 as part of the settlements in the wake of the Anglo-Maratha wars and soon turned their attention to its revenues again. By this time, Jamiat Rai was dead and his and Lallubhaiâs successors had considerably less influence in Bharuch.78 Meanwhile, the bottom was dropping out of the market for cotton fabrics and the local weaving industry was disintegrating. In 1825, Monier Williams, collector of Bharuch in the 1820s, wrote that as high-quality English cloth could be purchased at âabout half the price of the dotees and baftas, even on the spot where they are made, this manufacture is of course going rapidly to decay.â79 With the hereditary district officers out of the way, and the district only of value for its raw cotton and land revenues, Bharuch became a test location for experiments in revenue surveying.80

Illustrating British officialsâ attempts to systematize revenue record-keeping is a âfield bookâ or jarÄ«f-no chopá¸o containing the assessment and revenue records of the village of Kajipura in the pargana of Matar, Bharuch district, from 1820, at which time the British had been re-established in Bharuch for seventeen years. From the collections in the Bodleian Library of the Sanskritist Sir Monier Monier-Williams, presumably inherited from his father, the erstwhile collector of Bharuch, the field book is a rare surviving example of a village-level revenue survey of the early colonial period.81

The field book demonstrates continuity as well as change in land-revenue practices since the 1770s. It is in Gujarati with copious interlinear annotations in English, either by the senior Monier Williams or by the superintendent of the revenue survey, Lieutenant Ovans, who declared the document to be âOriginal.â82 (For translation, see Appendix 2.) The book sprawls over 46 foolscap-like folios, drawn up with space for extensive annotation. The numerical calculations are simple and neatly compiled. JarÄ«f-no chopá¸o, as the book identifies itself on the first complete page, is a Persian-Gujarati composite term comprising jarÄ«f from Persian jarÄ«b, a unit of land or area, and chopá¸o, Gujarati for book. The terms suggest that the language of Persianate/Mughal-style revenue assessment still prevailed in the 1820s, but, as we shall see, the British had now put in place changes that included English interpolations and vernacular elaborations.

The annotator tells us in English that two copies were always made of the field book. The calculations in the second copy were made by a second person and were entered and added up in reverse to ensure the veracity of the original. The corresponding Gujarati text has more details, explaining that the measurements and figures of the jarÄ«f (here abbreviated from jarÄ«b-amÄ«n, or surveyor) were on top and those of the talÄt̤ī, village accountant, were below. The manuscript begins with a section on the measurements employed: the basic measure was of a bamboo rod, exactly 5 âhandsâ or 8 English feet long. The units of measurement were gaj and lÄ«g. 25 lÄ«g made up one vasvÄá¹sÄ«, 500 made one vaso, and 10,000 made one vÄ«ghu (bÄ«ghÄ). Apart from âlÄ«g,â these are all Mughal measurements found in the ÄâÄ«n-i AkbarÄ«.83

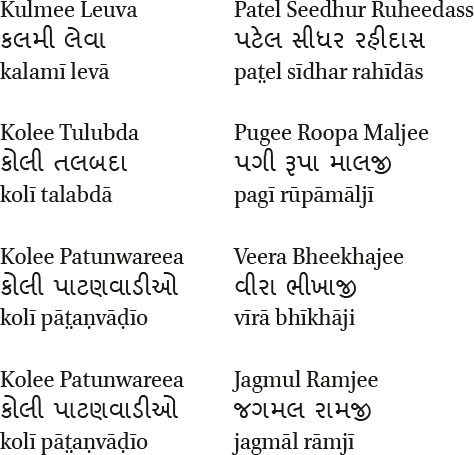

The next page explains what the book is: a book of the measurements of the fields produced under the superintendence of Lt. Ovans. The fields were measured by officials from neighboring villages: the amÄ«n pat̤el ĪsapjÄ« MiÄnjÄ« of village Khojbal and the amÄ«n Mugat̤rÄm HarirÄm of village Dora. The Arabic-Persian term amÄ«n refers to a village-level official appointed to measure lands; amÄ«n pat̤el was a village or community headman who held the title of amÄ«n.84 The measurement was carried out in the presence of representatives of the village farmers: one member each from the Kalmi Leva and Koli Talabda communities, two from the Koli Patanvadia community, and the talÄt̤ī or village accountant, an Audich brahmin named HarÄ«nÄraá¹ GovandrÄm. It is worth noticing that the farmers are classified by jÄti, endogamous group, with all belonging to middling- or lower-status groups. While the talÄt̤īâs brahmin status is identified, the aminsâ community affiliations are not provided, although one may surmise that ĪsapjÄ« MiÄnjÄ« was a Muslim and Mugat̤rÄm HarirÄm a Vaishnava.

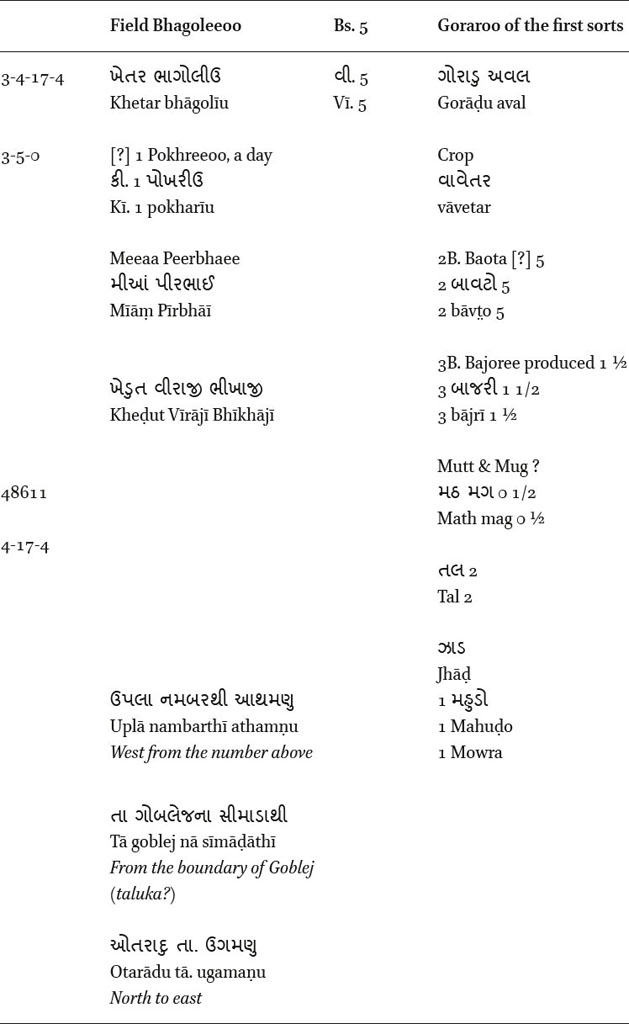

The book continues with 33 pages of measurements of the holdings of individual farmers with details of their dimensions, the kind of soil, the crops being produced (including trees, such as mango or the alcohol-producing mahuá¸o), and the assessed revenue. Duly recorded is the name of the landlord, the tiller of the soil (in a few instances they are the same), and whether any of the land is disputed. At the end is a calculation of the total area under cultivation in Kajipura village, including all cultivable land, wasteland, villages, ponds, and so on.

Next follow memoranda (Gujarati Ä«ÄdÄs, Persian yÄddÄsht) of different aspects of revenue assessment and collection in the village. One demonstrates incentives offered for the bringing marginal, marshy lands under rice cultivation. The tax was assessed per bÄ«ghÄ of land and varied based on the crop being grown and the quality of the soil. If fallow or uncultivated land was turned into rice-growing land, the vighot̤ī, or tax assessment per bÄ«ghÄ, could be frozen for a period of five years. Marginal lands taken into cultivation would pay lower annual rates, rising gradually (one rupee per bÄ«ghÄ for the first year and 1 ¼ the following year).

Another memorandum is on the payment of salÄmÄ«âa Persian term for tributeâto the government on lands either mortgaged (ghareá¹iu) or alienated as tax-free gifts (pasÄitu). It is noteworthy that the government continued to receive a small income even on alienated lands. Another memo explained that of the rice produced in the village, half was the cultivatorâs while the other half went to the government, with Rs. 3 deducted from the cultivatorâs share to pay village servants. Of the second crop of the year, usually barley, wheat or chÄ«no (sugarcane?), three-fourths went to the cultivator without any deduction. There are memos on pasÄita and chÄkariÄ lands granted to village servants in lieu of services andâas before!âadditional verÄ demanded by the government.85 For every plough pulled by two bullocks, the farmer paid two rupees, and for a one-bullock plough, a rupee. If these charges were paid, the village would be freed from paying further charges for cowdung cakes, firewood and grass.

One schedule deals with the jamaâ-kharch (receipts and disbursements) of the village in the year 1819, with disbursements including payments to the accountant for paper and salaries. At the end is a Ä«ÄdÄs fÄragatÄ«nÄ«, memorandum of release, from the Persian yÄddÄsht (memorandum) and fÄrigh-khaá¹á¹Ä« (deed of release), a declaration signed by the village pat̤el and talÄt̤ī, promising that they had paid for the village measurements and that no monies had changed hands other than those authorized by the government.

A key feature of the field book was a village census or kul-vastÄ«, a Persian-Gujarati compound meaning total habitation. The census has ten columns. The first column contains a list of household heads organized by jÄti, or endogamous âcaste.â The village contained members of four jÄtis: Kalmi Leva (3 households), Koli Talabda (6 households), Koli Patanvadia (36 households), and one household of Vasvayas. The remaining 9 columns listed the number of homes, men and boys, women and girls, total number of humans (153), oxen and male calves, cows and female calves, buffaloes and calves, carts, and ploughs belonging to each household.86 One woman of the Koli Patanvadia jÄti named Pardesan Rupa lived alone with her bullock; all the other households were headed by men. In its formâa jÄti-wise enumeration of persons and animalsâthe census bears a closer resemblance to precolonial household registers like Munhata Nainsiâs lists from Marvad in the late 17th century than to the colonial census that began in 1871.87

In the absence of a corresponding field book from an earlier period, such as one that might have been kept by Jamiat Rai, it is possible in this document to discern changes from precolonial practice as well as significant elements of continuity. The first change is the very availability of the field book as well as its legibility in Nagari-script Gujarati with English annotations. The second change is from the pargana to the village as the key unit of revenue management. Correspondingly, the crucial official is now the talÄt̤ī or salaried village accountant rather than the entrepreneurial desÄÄ« or majmÅ«Ê¿dÄr. The talÄt̤ī was the author of the field book which was to be delivered directly to government, in the shape of Lt. Ovans, without any intermediary. There was now a direct and unmediated flow of information from village to government.

What persists is threefold. First, there is a continuity in the notion of superordinate government, sarkÄr, that is conceptually undifferentiated from the âain- and verÄ- extracting government of Jamiat Raiâs records.88 In spite of the fact that two embodiments of prior governmentâthe nawabs as well as the desÄÄ«s and majmÅ«Ê¿dÄrsâhad by now been dislodged, the British had merely replaced their predecessors as sarkÄr. As before, officials were appointed by the sarkÄr, fields measured for the sarkÄr, and taxes or crop shares paid to the sarkÄr. The field book recognizes that the sarkÄrâs personnel were British (sÄheb) but otherwise makes no distinction between any prior government and the current one.

Second is a durability in the categories of information sought and in the methods of collecting it. The bulk of the document consists of measurements of holdings, documentation of land ownership, and assessments of crops and yields. The kul-vasti is organized on precolonial lines and, as in the rest of the document, records fiscal and hierarchical information that was equally critical to the organization of the precolonial and colonial state. Just as in Jamiat Raiâs accounts, we see close attention paid to taxes and tax-free grants of land.

Finally, there is a continuity in the transregional Mughal and Persianate revenue terminology (e.g., bÄ«ghÄ, bÄ«svÄ) that suffused a text written in Gujarati for British administrators. The terms for length and area correspond, with the exception of the words lÄ«g and feet, to Mughal equivalents. Dates are according to the Gregorian as well as Vikram Samvat calendars. The field book contains characteristic Gujarati usages such as vero, as discussed above, ghareá¹iu for mortgaged land, and pasÄitu, tax-free land for village servants, all of which terms appear in earlier records, and there are in addition a number of Persian-Gujarati compound terms. During almost a half century of transition from early Company rule in 1772 to unquestioned control in 1820, Persianate Gujarati and its association with government proved to be resistant to regime changes. Even if the colonial stateâs village-level documentation was exclusively in Gujarati and according to a set template of required information, Gujarati now had a baked-in Persianate vocabulary. While the whole stratum of revenue personnel was now replaced by salaried village accountants, prevalent technical terms and unitsâand corresponding conceptual categoriesâwere harder to dislodge.

Conclusion

With important exceptions, a significant part of theorizing on precolonial land revenue has been based on normative or prescriptive texts.89 There are several reasons why historians have relied primarily on such sources. The first is that prescriptive texts offer a tidy picture of land relations and suggest a well-functioning, centrally-controlled imperial machinery, a picture of Mughal order and intent that appealed to the anti-colonial impulses of postcolonial historians. For instance, the AâÄ«n-i AkbarÄ« offers a reassuring image of imperial benevolence when it came to customary taxes over and above land revenue. Deeming such charges to be âtroublesome and vexatious to the people,â the emperor Akbar had âin his wise statesmanship and benevolence of rule carefully examined the subject and abolished all arbitrary taxation, disapproving that these oppressions should become established by custom.â90 Another reason is that texts of practice are hard to come by, probably by design, because they formed a critical part of the knowledge capital of land revenue family firms such as those of Jamiat Rai and Lallubhai. Even when found, they are not easy to interpret (a feature that led British officials to cast them as illegible or disorganized) and offer a messier picture of land relations that can be at odds with the orderly vision of the prescriptive texts. While more records will undoubtedly come to light, the problem of apparent scarcity of sources might also be addressed by regarding archives as activities, or as sets of âcultural and social practicesâ rather than as spatially-defined repositories.91

Further, texts of practice are often sidelined as evidence of localized or deviant conventions rather than as manifestations of how the system worked because they reveal that the system was, in spite of Akbarâs stated benevolence, always extractive and entrepreneurial, only constrained on the one hand by a thin layer of often unenforceable imperially-mandated norms and on the other, by the exigencies of local politics and customs. As more land revenue texts maintained by family firms come to light, and as our attention turns to a wider range of documents and documentary traces, the better we will be able to explicate the âsocial logicâ of paper cultures.92 I expect further research will continue to destabilize normative pictures of state activity and demonstrate a lively stratum of district-level expertise and entrepreneurship that functioned within the broad framework of Mughal Persianate law but with only sporadic oversight by the higher reaches of the Mughal bureaucracy.

Their early experiences with the likes of Jamiat Rai and Lallubhai set the British against the entrepreneurial family firms, now cast not only as âtroublesome or vexatious,â as they were by Akbar, but as ignorant and inscrutable interlopers who obscured the proper functioning of government. As the British listed all prevailing taxes and measured the land, placing the elicited information in Gujarati-language docketed archives, they succeeded in cutting into the complex, multilingual webs of knowledge and authority wielded by the family firms in a way that had been impossible for the Mughals.93 By edging out such âprivatizedâ desÄÄ« and majmÅ«Ê¿dÄr firms, and replacing them with subservient village talÄt̤īs, the early colonial state rooted out revenue entrepreneurship and staked control over the invaluable commodity of the revenue archive. Revenue records, safely and legibly organized in record rooms, were deemed to have been rescued from the domain of entrepreneurial commerce and restored to the domain of the law and the state. By claiming direct access to revenue records to establish an imperial system of rights and privileges, it might be argued that Company officials were not putting in place a nascent British empire. Rather, they were restoring the benevolent Mughal imperium as imagined in Persian by Abuâl Fazl.94

What exactly changed between the late-Mughal/early colonial period and the 1820s? First, as we have seen, emboldened by their victories in the Anglo-Maratha wars, the British pensioned off or dismissed the long-established, patrimonial, semi-autonomous district (pargana) officials on whom they had relied in the early days, appointing in their stead salaried village officials overseen by British revenue collectors. Such officials had already been weakened by the Maratha interregnum (1783-1803), when they were forced to bid for the farm of the districtâs revenues. Second, they succeeded in mandating the replacement of the contextual multilingualism of revenue practice, operated in south Gujarat by district officials and comprising written and oral versions of Gujarati, Persian, Hindi, Marathi, and English, by written Gujarati in Nagari script, overseen by English. Multilingualism and opacity allowed its practitioners to withhold information and resources from the state; Gujarati-English bilingualism and standardization facilitated transparency. In theory, at least, the board of governors of the EIC could examine and weigh in on revenue collection in Bharuch in a way the Mughals had never achieved. Third, the emphasis in record-keeping shifted from the relational language of hierarchy and obligation, as witnessed in the plethora of customary dues, to the dawning of Cohnâs survey and enumerative modalities.95 No longer could village patels register political discontent by failing to proffer a sukhá¸Ä« or claim protection in return for a whip-round vero. The new imperial system was equally extractive and perhaps even more violent but was impersonal by design.

Ultimately it doesnât really matter what language Jamiat Rai scribbled in; what matters is that multilingualism and entrepreneurship in land revenue administration was too unruly, opaque, and reliant on affective relationships for the increasingly profit-driven new administration. By forcing in place a new subservient Gujarati monolingualism, the British had succeeded, by the 1820s, in siphoning up the flow of information and resources in a way the Mughals had desired but never realized. This was not the end of the story, of course, but the consequences of the new system in the later 19th century, including the recurrence of patrimonial authority within the colonial system, the rise of modern Gujarati, and the emergence of new forms of peasant protest, are beyond the scope of this paper.

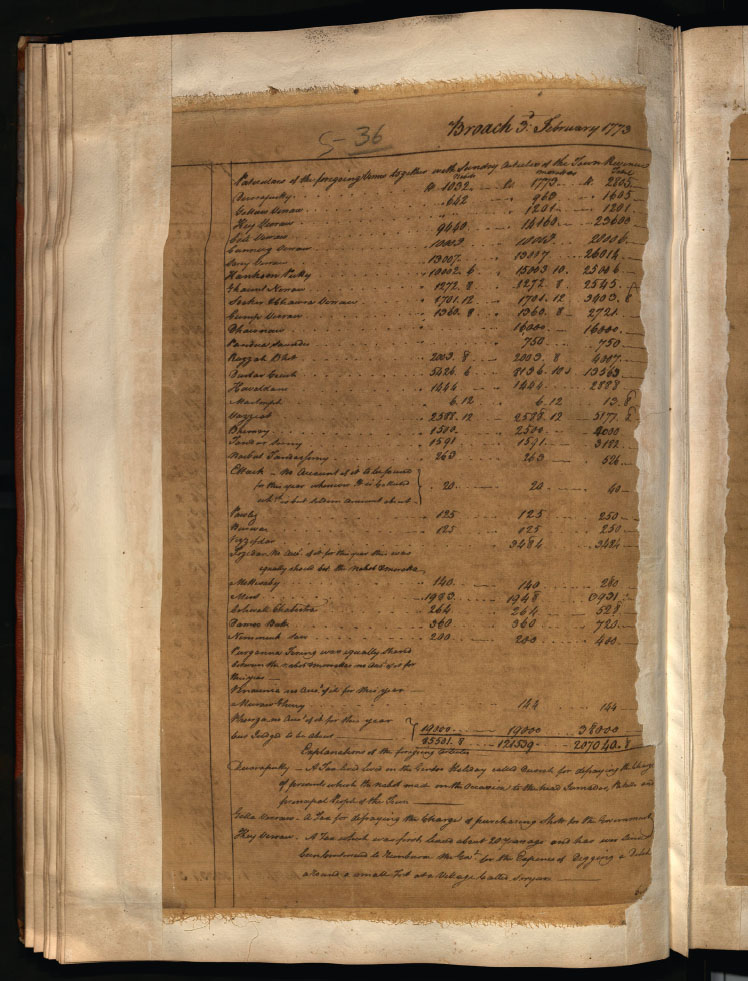

Appendix 1: Particulars of the foregoing Verrow together with Sundry Articles of the Town Revenues96

Figure 1

Citation: Journal of the Economic and Social History of the Orient 64, 5-6 (2021) ; 10.1163/15685209-12341551

Citation: Journal of the Economic and Social History of the Orient 64, 5-6 (2021) ; 10.1163/15685209-12341551

Appendix 2: The Field Book of Kajipura, Pargana Matar, 182098

Figure 2

Citation: Journal of the Economic and Social History of the Orient 64, 5-6 (2021) ; 10.1163/15685209-12341551

f. 1a [a page of text in Nagari script, presumably in Gujarati, although only individual words can be made out. Not transcribed here.]

f. 1b [a page of text in Arabic, comprising verses attributed to âAli b. Abi Talib, al-Mutanabbi, the pre-Islamic poet Antara b. Shaddad, and an unidentified poet, written diagonally across the page. Not transcribed here.99]

f. 2a

[In English] Purguna Matur

[Gujarati script]

[Transliterated from Gujarati] Pargaá¹emÄtar

Village Kajeepoora

MojekÄjÄ«purÄ

[In English] Of this Book a duplicate is always found in which all the calculations are made by a Separate person, at a different time and by reversing the figures. This is done to verify the original. It is afterwards left at the village in the care of the people. The memorandum of the village Dara, or mode of collecting the government revenueâthe Juma Khurch or account of village Receipts & disbursements & the Statement of the population are therefore not inserted in the duplicate.

f. 3a-b Purguna Matur

Pargaá¹emÄtar

Village Kajeepoora

MojekÄjÄ«purÄ

The Standard Basis, or Rod, is in length 5 Hath, or 8 feet English exactly.

SarkÄrÄ« vÄá¹slÄá¹ bÄme hÄth 5 pÄá¹ch barÄbar chhe tÄ. [tathÄ] fÄ«t̤ 8 Ät̤h aá¹ grejÄ« barÄbar chhe

The government bamboo rods are exactly 5 hands or exactly 8 feet English.

All the measurements are made & set down in Chains, Dusans [?] & Hath

Sarve mÄpvanu kÄm sÄá¹ kal tÄ. gaj tÄ. lÄ«g thÄ« chÄle chhe

All the measuring work is in chains and gaj and līg100

One Chain contains 3 Dusans, and one Dusaus contains 10 Hath.

SÄá¹ kal 1 ek nÄ gaj 3 taraá¹ chhe gaj 1 ek nÄá¹ lÄ«g 10 das chhe

One chain has 3 gaj and 1 gaj has 10 līg

All the calculations are made in Hath

sarve gaá¹vÄnu kÄm lÄ«gthÄ« chÄle chhe

All measurements are in līg

25 Hath make one Wis-wussa. 500 Hath make one Wussa, and 10,000

lÄ«g pachÄ«sno vasvÄá¹sÄ« 1 ek chhe lÄ«g 500 pÄñchse[so] no vaso 1 ek chhe lÄ«g 10000 das hajÄrnu

25 lÄ«g make vasvÄá¹sÄ«. 500 lÄ«g make 1 vaso. 10,000 lÄ«g make

Hath make one Beega, Square measure.

vīghu 1 ek chhe

1 vīghu [bīgha]

Add the two perpendiculars together, multiply their sum by the diagonal

Äá¸Ä« sÄá¹ kal ekat̤hÄ« karvÄ« ne lÄmbÄ« sÄá¹ kal sÄthe bhÄá¹ gaá¹Ä« karvÄ« ne te

Join the perpendicular chains and multiply the sum by the long chain and

and half the product will be the contents of the figure in Hath.*

nu aá¸adh karvu tehenÄá¹ vÄ«ghÄá¹ tÄ. vasÄ ta. vasvÄá¹sÄ« thÄe chhe

halve it; that will be the bighÄ, vasa, vasvÄsÄ«

In this Field Book the number & contents of the field by the measurement

E jarÄ«fnÄ chopaá¸ÄmÄá¹ jarÄ«fno nambar ta.[tathÄ] jarÄ«fnÄá¹ vÄ«ghÄá¹ upar chhe ta.

In the Jarif book, the Jarif number is above the Jarif measurements in bīgha

are placed above, and the number of the field & its computed quantity by the village Tullateeâs accounts, are placed below.

talÄt̤īno nambar ta. ÄsrÄno vÄ«ghÄá¹ nÄ«che chhe

The talÄt̤īâs number is below the estimated measurement in bÄ«ghas.

[In English] * This is, of course, only applicable to the Trapezium, which is the figure always used with the exception of the Triangle occasionally.

f. 4a-b Purguna Matur

Pargaá¹e MÄtar

Village Kajeepoora

Village KÄjÄ«purÄ

Field Book of the measurements of the fields; Sumwut 1876, Wueesakh

khetarÄnÄ« jarÄ«fno chopaá¸o saá¹vat 1876 nÄ vaisÄkh sud vÄr bharespat tÄ.

The book of the measurement of the fields (field book) [was done on] Thursday, of Vaisakh Sud, 1876 date

Sud; War Bhresput. Thursday the 20th April AD 1820. Under the

20

20 mÄhe aparel sanne 1820 Ä«svÄ« haste laft̤enat̤h ovÄn sÄheb nÄ«

20[,] month of April year 1820 Christian [Era] at the hands of Lieutenant Ovan Saheb

Superintendence of Lieutenant Ovans. Measurers of the fields Eesup Mee-

hajÅ«r jarÄ«f nÄ khetarÄá¹nÄ amÄ«n pat̤el Ä«sapjÄ« mÄ«ÄñjÄ« moje khojbal

[who was] present for the measurement of the fields Amin Patel Isapji Mianji of village Khojbal,

-ajee of Khojbul and Moogutram Hureeram of Dora, both in the Baroche

na pargaá¹e bharuch tÄ. amÄ«n mugat̤rÄm harÄ«rÄm moje dorÄnÄ pargaá¹e bharuch

district Bharuch and Amin Mugatram Hariram of village Dora, district Bharuch.

Present at the measurement

moje majkurnÄ« jarÄ«f vakhat hÄjar

Present at [the time of] the measurement of the aforesaid village

Citation: Journal of the Economic and Social History of the Orient 64, 5-6 (2021) ; 10.1163/15685209-12341551

Tulatee Hurree Narun Govindram, Oodeech Brahmun

t̤alÄt̤ī harÄ« naraá¹ govand rÄm ganÄte bharÄmaá¹ avadÄ«ch

The talÄt̤ī Hari Naran Govand Ram of the Audich Brahmin jati

The numbers and computed quantities of the fields are taken from the village Tulatees account for Sumvut 1876

t̤alÄt̤īnÄ nambar khará¸o saá¹vat 1876nÄ« fasalno chhe te uparthÄ« mapu chhe

The talÄt̤īâs numbers and computed quantities are from the yield [fasÌ£al] of Samvat 1876 and are measured from them.

[f. 5a-36b are individual pages of measurements of individual fields, including information on zamindar, farmer, type of soil, what is grown, etc. One sample page is included here]

Citation: Journal of the Economic and Social History of the Orient 64, 5-6 (2021) ; 10.1163/15685209-12341551

[more measurements and calculations, not included]

[Note at the bottom, in English]: (See No. 79 for further translation. The above are considered sufficient for examples of the intermediate fields.)

f. 37a Number 24 of 0 ½ Beega and Number 30 of 3 Beegas, of this Tulateeâs account are

e jamÄ«nmÄá¹ talÄt̤īno nambar 24 chovÄ«smo vÄ«ghu 0 || (1/2) moje goblej sÄthe

In that land, half a bÄ«ghÄ of the talÄt̤īâs Number 24 and 2 bÄ«ghÄs of the talÄt̤īâs number 30 are in dispute with the village Goblej

in dispute with Goblej & do not appear in this memorandum.

kachÄt̤īu chhe temaku nathÄ« tÄ. talÄt̤īno nambar 30 tÄ«smo vÄ«ghÄ 2 moje goblej sÄthe kachÄt̤īu chhe temaku nathÄ«

and are not listed.

ff. 38-40a columns of numbers

f. 40b [Columns of measurements, not included.]

[at bottom]

Citation: Journal of the Economic and Social History of the Orient 64, 5-6 (2021) ; 10.1163/15685209-12341551

Memorandum of the custom practised in this village of collecting the Government Revenue

Ä«ÄdÄs sarsatÄnÄ« vÄ«got̤ī vagarenÄ moje kÄjÄ«purÄno

Rice ground is Bhagwutueeâor paying in Kind,

kÄeá¸ÄnÄ« bhÄgbat̤ÄÄ« haá¸dho bhÄg kheá¸uno ta. [tathÄ] haá¸dho bhÄg sarkÄrno

The prevailing system of crop-sharing [is] half share to the farmer and half share to the government.

half is the Cultivatorâs and half goes to Government.

tÄ. kÄeá¸o 1vÄ«. 1. Å«dhaḠchhe Ru 3 lakhenÄ chhe jamÄ«n gorÄdunÄ« vÄ«gho

and the prevailing system the first fallow/unmeasured is Rupees 3 [is written][.]Yellowish wet soil bīgha land

There is one Beega let at a fixed rent of 3 Rupees an-

t̤ī dar vÄ«ghe 1 Ru 2 ¼ parmÄá¹e navu bhÄge tehenÄ« vÄ«ghot̤ī kÄeá¸ÄnÄ«

-nually. Goraroo is Beegotee, or paying so much

vÄ«ghe 1 Ru 2 ¼ parmÄne varas. 5 sudhÄ« e parmÄá¹e bhare tÄr 5 chhe

p. Beega; here at the rate of 2 ¼ Rupees. Goraroo made into Rice ground is Beegotee for 5 years at the rate

bhÄg bat̤Äi haá¸dho haá¸adh Äpe

of 2 ¼ Rupees p. Beega, after which it becomes Bhag wuttaaee. Waste Goraroo taken into cultivation pays

gorÄdu navu bhÄge tehenÄ« sÄth dar vÄ«ghe 1 Ru 1 ½ parmÄá¹e pehele var

the first year 1 ¼ Rupee p Beega, and afterwards 2 ¼ Rupees p. Beega

s [varas] Äpe tÄr pachhÄ« Ru 2 ¼ parmÄá¹e har sÄl Äpe

Goraroo of an inferior kind (Kharor) when newly taken

ta. gorÄá¸u khÄroá¸e madhe thÄ« bhÄge navÄ« bhÄge tehenÄ« sÄth dar vÄ«ghe 1

into cultivation, pays the first year 1 R p. Beega & [?] afterwards 1 ¼ R p. Beega annually.

Memorandum of the Sulamee or payment to Government from land exempted from the regular assessment.

salÄmÄ«ÄnÄ« Ä«ÄdÄs

Memorandum of the Collections in aid of Govt from Irrigated Rice ground. The first or Rice crop is equally divided between the Cultivator and the Govern-

kuvetar kÄeá¸o 1 sarkÄrÄ«o chhe tem ghe á¸Ängari mÄá¹ bhÄg haá¸adh hiá¸adh

-ment, a deduction, however, being made previously to the division, of about 3 Rp

ta. jav tÄ. ghahu tÄ. 2 vÄ« chÄ«á¹o vagareno chotho bhÄg Äpe

and given to Wuswaeeas or certain village servants. The second crop generally consisting of Barley, Wheat or Cheena, is Shared in the proportion

bhÄg 1 sarkÄr mÄá¹ Äpe ta. bhÄg 3 kheá¸unÄ

of three fourth to the cultivator and one fourth to the Government, without any deduction.

p. 41b Memorandum of the Pussaeeta and Chakureea, or land held for Service, to the village community. All free.

pasÄatu vagare nakaru chhe

Memorandum of the Veras or extra collections on account of Government

halvero hal 1 baladh 2 Ru 2 lekhe tÄ. baladh 1 hoe to Ru. 1 parmÄá¹e

For every plough with two Bullocks 2 Rupees and with only one Bullock, 1 Rupee. The payment being made, the village is relieved from any requisition (Vit?)

Äpe e rupÄ«Ä sarkÄr adÄlatnÄ« vet̤h chhÄá¹Ä lÄká¸Ä tÄ. ghÄsnÄ gÄdÄ

of the Adaulut for Chaua (dried cowdung cakes for fuel). Firewood and

bÄbat le chhe e rupÄ«Ä ÄpÄ«e chhÄ«e tÄre vet̤he mÄp chhe e savae

Grass. There is no other Vera or Collection of any kind in this village.

bÄ«jÄ« kaÄ« pedÄs tÄ. vero nathÄ«

Memorandum of the Village Tulateeâs Numoonus, or Statements of the [?] for Sumvut 1876

Ä«ÄdÄs moje kÄjÄ«purÄ pargaá¹e mÄtar nÄ gÄm saá¹vat 1876 nÄ« fasal no namuno

[More measurements of the arable land and other village characteristics; not included.]

f. 42a-b [List of all cultivable land, waste land, well, pond, etc. with totals. Not included here]

f. 43a The Juma Khurch, or Account of receipts, and disbursements, of the village of Kajeepoora, Matur Puga. for the Season of Sumvut 1875

moje kÄjÄ«purÄno jame kharach pargaá¹e mÄtarnÄ gÄmÄno saá¹vat 1875nÄ« fasalno

-----------------------------------

--------------------------------- om --------------------------------

[Calculations, not included here]

f. 44a blank

f. 45a-45b Statement of the population of the village of Kajeepoor. Sumvut 1876 Waesakh. April AD 1820

Khará¸o kul vasatÄ« no mÄá¹as tathÄ jÄnvar no moje kÄjÄ«purÄno saá¹vat 1876 nÄ vaisÄkh mÄhe Äparel sane 1820

[Table with 10 columns displaying headers as below]

GÄmnÄ« vasatÄ«nÄ« jÄt

Ghar

Marad tÄ chhokrÄ

Orat tÄ chhokrÄ«

Kul mÄá¹as

Baladh tÄ vÄchhaá¸o

GÄa tÄ vÄchhaá¸Ä«

Bheso tÄ pÄá¸o

GÄá¸Ä

Hol

[46 Rows listing each household head, arranged into jÄti groups as below. Names and numbers not included here.]

KalamÄ« levÄ; KolÄ« talabdÄ; KolÄ« pÄt̤aá¹vÄá¸Ä«a, vasvÄÄ

f. 46a [Tallied totals of the census, listing 46 households, 79 men and boys, 74 women and girls, 153 persons in total, 43 bullocks and bull calves, 12 cows and female calves, 34 buffaloes and calves, 7 carts, and 16 ½ ploughs.]

f. 47a The general Acknowledgement and Receipt

Ä«ÄdÄs fÄragatÄ«nÄ«

We the undersigned Patell, and Tulatee of the village of Kajeepoora

lÄ. ame pat̤elo tÄ. talÄt̤ī moje kÄjÄ«purÄnÄ khetaro tÄ. jamÄ«n dekhÄá¸Ä«ne

declare that we pointed out the field, and lands of our village and were present at their measurement.

bharÄvÄ« ne bhartÄ« vakhat hÄjar hatÄ jat

their Batta as ordered by Government, and nothing more or less

sÄ [paisa] sarkÄrnÄ hukam parmÄá¹e ÄpÄ chhe hukam savae ek damá¸Ä« jÄda tÄ kam

was given or received.

ÄpÄ« lÄ«dhÄ« nathi.

Superintending Officer or by any of his servants, whether from

Äpo tenÄ paisÄ tÄ. nokar chÄkar loknÄ kharach khurÄki vagere je kaÄ« vÄá¹Ä«

the Buneea or from any other person belonging to the village

Äne [vaá¹iÄne] tÄhÄthÄ« tÄ. gÄm mÄá¹thÄ« lÄ«dhu hase te sarve nÄ paisÄ dÄm daram darobast ha-

has been duly paid for to the people themselves to the village

-sÄb karÄ«ne vÄlÄ« lÄ«dhÄ chhe hÄve thÄ« e jarÄ«fnÄ kÄm samandhÄ«nu levu devu koi joá¸e

[and something] and [?] on accounts of this measurement

rahu nathi ne hasÄb vÄlÄ« leine fÄragatÄ« lakhÄ« ÄpÄ« chhe e lakhu sahÄ« saá¹vat 18

nothing whatever remains [unstated?] and this acquittance is

76

76 nÄ pahela jet̤h vad 5 vÄr gareÅ« tÄ. 1 mÄhe jun sane 1820 Ä«svÄ«

given accordingly. Sumwut 1876, 7th Jeth wud 5th Thursday 1st June AD 1820

Acknowledgments

For comments on this paper I am grateful to the participants in âTransactions and Documentation in the Persianate world,â a workshop of the Lawforms project, Exeter (July 2018), âNew Directions in South Asian Economic History,â a workshop at the University of Pennsylvania (May 2019), and to three anonymous reviewers and the editing staff at JESHO. Thanks especially to Ashkan Bahrani, Nandini Chatterjee, Faisal Chaudhry, Divya Cherian, Sumit Guha, Najaf Haider, Prashant Kidambi, Françoise Mallison, Dipanjan Mazumder, Sudev Sheth, Amrita Shodhan, Ramya Sreenivasan, Musa Subramaniam, Elizabeth Thelen, David J. Wasserstein, Dominic Vendell, and Steven Vose for their help. All errors remain mine. I thank the European Research Commission and the Lawforms project for providing funds to publish this article, and the entire issue, in Open Access format.

Bibliography

Unpublished Sources

Surat Factory Diaries. Mumbai: Maharashtra State Archives.

Broach Factory Diaries. Mumbai: Maharashtra State Archives.

Revenue Department Diaries, Mumbai: Maharashtra State Archives.

1785. Ḥaqīqat-i Bandar Bharūch. Oxford: Bodleian Library.

1820. JarÄ«f-No Chopá¸o (Measurement Papers and Records of the Village of KÄjipurÄ, Parganah MÄtar, in the Broach District of Bombay). Oxford: Bodleian Library.

Published Sources

1845. Debates at the India House: August 22nd, 23rd and September 14th, 1845, on the Case of the Deposed Raja of Sattara and the Impeachment of Col. C. Ovans. London: Effingham Wilson.

Abbott, N.J. 2018. Bringing the SarkÄr Back In: Translating Patrimonialism and the State in Early Modern and Early Colonial India. In State Formations: Global Histories and Cultures of Statehood, ed. J.L. Brooke, J.C. Strauss and G. Anderson. Cambridge, Cambridge University Press: 124-137.

Abuâl Fazl. 1891. ÄâÄ«n-i AkbarÄ«, trans. H.S. Jarrett, 2 vols. Calcutta: Asiatic Society of Bengal.

Alam, Muzaffar and Sanjay Subrahmanyam. 2004. The Making of a Munshi. Comparative Studies of South Asia, Africa and the Middle East 24/2: 61-72.

Alam, Muzaffar and Sanjay Subrahmanyam. 2010. Witnesses and Agents of Empire: Eighteenth-Century Historiography and the World of the Mughal Munshī. Journal of the Economic and Social History of the Orient 53/1-2: 393-423.

Alam, Muzaffar. 1998. The Pursuit of Persian: Language in Mughal Politics. Modern Asian Studies 32/2: 317-349.

Alam, Muzaffar. 2003. The Culture and Politics of Persian in Precolonial Hindustan. In Literary Cultures in History: Reconstructions from South Asia, ed. Sheldon Pollock. Berkeley: University of California Press: 131-198.

Alam, Muzaffar and Seema Alavi. 2001. A European Experience of the Mughal Orient: The IâjÄz-i ArsalÄnÄ« (Persian Letters 1773-1779) of Antoine-Louis Henri Polier. New York: Oxford University Press.

Anooshahr, A. 2012. Author of Oneâs Fate: Fatalism and Agency in Indo-Persian Histories. Indian Economic and Social History Review 49/2: 197-224.

Asani, A.S. 1987. The Khojkī Script: A Legacy of Ismaili Islam in the Indo-Pakistan Subcontinent. Journal of the American Oriental Society 107: 439-449.

Bagheri, M. 1998. âSiyÄqatâ Accounting: Its Origin, History, and Principles. Acta Orientalia Academiae Scientiarum Hungaricae 51: 287-301.

Bayly, C.A. 1996. Empire and Information: Intelligence Gathering and Social Communication in India, 1780-1870. Cambridge: Cambridge University Press.

Bellenoit, Hayden. 2014. Between Qanungos and Clerks: The Cultural and Service Worlds of Hindustanâs Pensmen, c. 1750-1850. Modern Asian Studies 48/4: 1-39.

Bellenoit, Hayden J. 2017. The Formation of the Colonial State in India: Scribes, Paper and Taxes, 1760-1860. London and New York. Taylor & Francis.

Belsare, M.B. 1993. An Etymological Gujarati English Dictionary. New Delhi: Asian Educational Services.

Bhadani, B.L. 1999. Peasants, Artisans and Entrepreneurs: Economy of Marwar in the Seventeenth Century. Delhi: Rawat Publications.

Bhagvatsiá¹hjÄ« and CandulÄl Pat̤el. 2008 (original publication 1944-55). Bhagavadgomaá¹á¸al. Rajkot: PravÄ«á¹ PrakÄÅan. (GujaratiLexicon.com).

Chatterjee, Kumkum. 2009. The Cultures of History in Early Modern India: Persianization and Mughal Culture in Bengal. Delhi: Oxford University Press.