Abstract

This study explores the roles of workers, producers, and buyers in the Honduran coffee supply chain, focusing on how market structure, bargaining power, and value flows shape market outcomes. Using a mixed-methods approach — combining a literature review, secondary data analysis, and in-depth interviews — it investigates the relationships among farmers, workers, cooperatives, intermediaries, exporters, and roasters. The findings highlight critical bottlenecks, such as issues with price transmission, quality differentiation, and traceability, compounded by weak bargaining power among workers and producers. The study suggests that while some challenges stem from market dynamics, others arise from misperceptions, particularly towards intermediaries. Applying a bargaining model, the study identifies opportunities to improve transparency, strengthen cooperative capabilities, and support farmers in selling high-quality coffee. This research provides actionable insights for policymakers and industry stakeholders aiming to enhance market coordination, fair trade practices, and value chain sustainability.

1. Introduction

The global coffee industry is shaped by complex supply chains where market structures, power dynamics, and coordination mechanisms between workers, producers, intermediaries, and buyers determine the distribution of value. Persistent challenges affect all actors in the value chain: smallholder farmers often face low bargaining power, limited access to markets, and poor price transmission, which hinders their ability to capture a fair share of the value of their coffee. Workers face precarious conditions, including low wages and a lack of social security benefits. Cooperatives struggle with low membership and financial instability, while private buyers, essential for aggregation and financing, often face reputational challenges. Exporters are increasingly pressured by sustainability requirements and regulatory demands, such as traceability standards, adding complexity to their operations.

This paper seeks to offer a deeper understanding of value flows across the coffee supply chain. While many of these challenges are rooted in structural issues, others stem from biases or misperceptions that have been historically directed towards certain groups. A rigorous study is necessary to separate these biases from the real dynamics at play, offering a clearer understanding of the underlying factors affecting value distribution and market efficiency. By examining the interactions between various actors through a bargaining perspective, this study aims to identify how power dynamics and coordination mechanisms influence value capture. The Honduran coffee supply chain serves as an ideal case study due to its complexity and the roles played by smallholder producers, cooperatives, exporters, and roasters, all operating within a weak institutional structure.

Using a mixed-methods approach that integrates a systematic literature review, stakeholder consultations, and secondary data analysis, this study characterizes dyadic relationships between key actors — producers, workers, cooperatives, intermediaries, and exporters — based on the market outcomes they experience, which can be either positive or negative. The analysis of secondary data help us link this outcomes to broader issues within the sector. Finally, we draw from the frameworks of Sexton (1990) and Swinnen and Van de Plas (2015) to understand how these outcomes relate to theorized issues around imperfect competition in local markets and poor information transmission. By applying these theories, we uncover bottlenecks and potential interventions that could improve value distribution across the supply chain.

The analysis of the Honduran coffee supply chain reveals key bottlenecks and opportunities for improvement. Limited quality contracting and labor scarcity are interlinked, as the inability to secure contracts that reward quality hampers farmers’ ability and incentives to improve production, harvesting, and processing methods, ultimately affecting wages and labor conditions. An opportunity to address this is through the sale of dry parchment coffee, which enables better quality assessment and access to higher-value markets, improving both farmer incomes and labor stability. Mismatched bargaining power between farmers, small aggregators, and large intermediaries/exporters results in unequal value distribution, with larger market actors capturing a disproportionate share of the value. Strengthening the managerial and commercial capabilities of cooperatives offers an opportunity to better position smallholder farmers, improving coordination, increasing market access, and enhancing collective bargaining power. Additionally, improving the transparency and fairness of intermediary transactions presents another opportunity to address power imbalances and improve outcomes for smaller actors in the value chain.

Our study also helped dispel several myths about the dynamics of the Honduran coffee sector. One misconception was that intermediaries were systematically shortchanging farmers, a belief fueled by outdated conversion rates outlined in the IHCAFE trading manual. These rates were much higher than the actual market conditions, leading intermediaries to apply more accurate, lower conversion rates. This resulted in confusion among farmers, who felt penalized due to the discrepancy between the official rates and the market rates. Another myth was that the lower quality of Honduran coffee was the primary reason for the price discrepancy, even as Honduras improved its quality. While Honduras did indeed produce lower-quality coffee initially, this was due to insufficient processing capacity, which lagged behind the rapid expansion of production; the country’s ability to process coffee effectively could not keep pace with the growth in production. As processing capacity improved and coffee quality increased, Honduran coffee’s reputation had already been damaged, and the country continued to fetch lower prices compared to its regional counterparts. A further myth centered on the perceived effectiveness of cooperatives as a means to improve outcomes for farmers. While cooperatives have been successful in some regions, there is a long history of cooperative bankruptcies in certain areas, severely damaging farmers’ trust. As a result, many farmers are now reluctant to work with cooperatives. We identified a need to strengthen cooperative governance while also investing in other supply channels, such as private intermediaries, especially in regions where trust in cooperatives has been irreparably eroded.

2. Methods

This study examines the Honduran coffee value chain by focusing on dyadic relationships between key actors — producers, workers, and buyers — and how these relationships shape market dynamics and value distribution. We structure our analysis around understanding these interactions and their impact on value capture across the chain. To do this, we employed a mixed-methods approach, combining a systematic literature review, stakeholder consultations, and secondary data analysis. Once we had characterized these dyadic relationships, we applied the imperfect competition and bargaining model of Sexton (1990) and Swinnen and Van de Plas (2015) to interpret the dynamics and identify key bottlenecks and opportunities for improving value flow and market coordination.

We began with a systematic literature review, following an adapted protocol from Liverpool-Tassie et al. (2020), to analyze interactions among key actors — workers, farmers, intermediaries, processors, cooperatives, and exporters. The review focused on economic relationships and market structures, particularly in terms of price formation, quality transmission, and coordination mechanisms. We searched multiple databases, including Google Scholar, Scopus, AgEcon Search, and CGIAR’s CGSpace repository, reviewing both peer-reviewed and high-quality grey literature. Each relationship was assessed based on its impact on market efficiency, value retention, and producer outcomes.

To complement these insights, we conducted 36 semi-structured interviews with key stakeholders between November 28 and December 22, 2023. Interviewees included farmers, intermediaries, cooperatives, and exporters, providing firsthand perspectives on how they navigate commercial relationships, price negotiations, and logistical constraints. Table 1 provides an overview of the actors interviewed during the consultation process.

Actors interviewed during the consultation process.

Citation: International Food and Agribusiness Management Review 2026; 10.22434/ifamr.1303

To further contextualize our findings, we analyzed secondary data from sources such as the Instituto Hondureño del Café (IHCAFE) and the International Coffee Organization (ICO). These data provided a broader perspective on production trends, price transmission, and market fluctuations, reinforcing and expanding on the evidence gathered through literature and interviews. Integrating these three sources of information allowed us to develop a structured mapping of the primary and secondary causes of inefficiencies, offering a comprehensive view of the dynamics shaping market performance.

Beyond identifying constraints, we examined strategies that stakeholders had implemented to navigate market challenges and improve coordination, price transmission, and quality upgrading. We explored unrealized strategies by asking stakeholders to reflect on interventions that had yet to gain traction but held potential for improving supply chain coordination and producer outcomes. These discussions provided a forward-looking perspective on possible advancements in the sector, highlighting adoption challenges and the conditions necessary for scaling new practices. A full list of interview questions is available in Appendix A.

3. Results

The initial database screening identified 105 publications that met the search criteria. After removing nine duplicates, 36 additional publications were excluded based on the research protocol criteria. Two additional papers, suggested by experts, were included, bringing the final count to 62 relevant publications. Each of these studies assessed at least one relationship between key value chain actors. The final dataset included 20 theses (30%), 17 journal articles (25%), 14 reports (21%), 13 working papers (19%), two conference proceedings (3%), and one book (2%) (Figure 1A). Research on the Honduran coffee value chain remained steady throughout the study period, with the number of publications ranging from six (2000–2004) to a peak of 19 (2016–2020) (Figure 1B), indicating sustained academic and institutional interest in the sector.

(A) Distribution of publications by type. (B) Distribution of publications by year published.

Citation: International Food and Agribusiness Management Review 2026; 10.22434/ifamr.1303

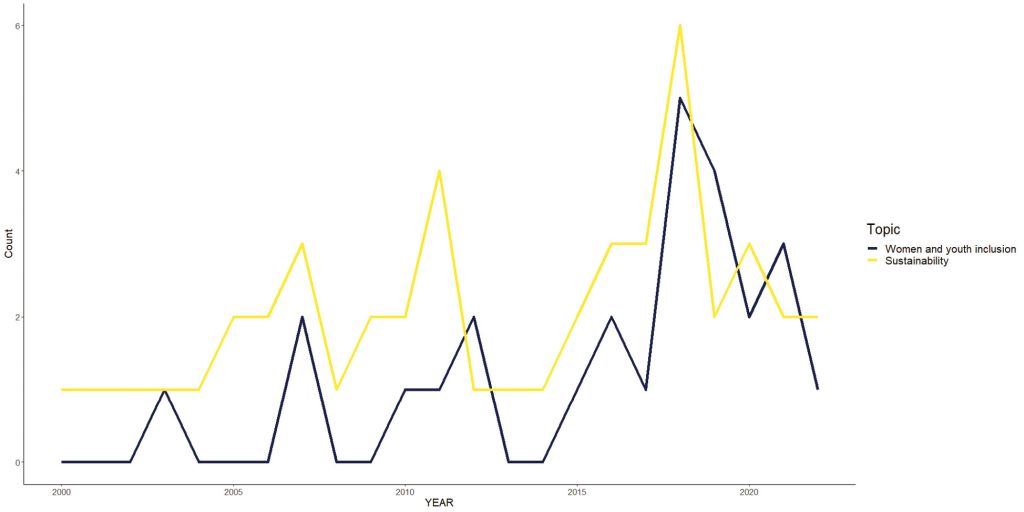

The literature demonstrated an increasing focus on environmental issues. Seventy-five percent of studies referenced environmental sustainability within the Honduran coffee supply chain, with 40% of these mentions appearing in the last six years. In contrast, gender and youth inclusion received significantly less attention, appearing in only 42% of publications. However, interest in these topics has grown, as two-thirds of these mentions were published within the last six years (Figure 2).

Number of publications that included a focus on women and youth inclusion, and on sustainability, per year.

Citation: International Food and Agribusiness Management Review 2026; 10.22434/ifamr.1303

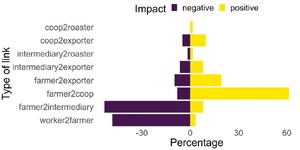

Figure 3 shows how studies assessed relationships between value chain actors. The farmer-intermediary relationship had the highest proportion of negative outcomes, with 52% of studies highlighting negative impacts and only 8% reporting positive outcomes. Limited bargaining power for farmers and weak incentives for intermediaries to improve farmer income or quality were the main concerns. However, the literature also noted that intermediaries are perceived as stable partners who have maintained long-term relationships with farmers. The worker-farmer relationship was the second most negatively portrayed, with 45% of studies reporting negative outcomes and only 3% highlighting positive aspects. Issues such as informal labor arrangements, lack of social protection, and worker exploitation were the most commonly cited problems.

Positive and negative impacts of actor-to-actor relationships in the Honduran coffee value chain.

Citation: International Food and Agribusiness Management Review 2026; 10.22434/ifamr.1303

In contrast, 60% of studies reported positive outcomes for farmer-cooperative relationships, with only 8% describing negative impacts. Cooperatives were recognized for providing services such as training, consolidation, processing, and marketing, which help improve the commercial prospects of affiliated farmers. However, their history of financial mismanagement and past bankruptcies have harmed their reputation, leading to distrust among producers. Other actor relationships shown in Figure 2 received minimal attention, suggesting either mutually beneficial interactions or a lack of research on these links.

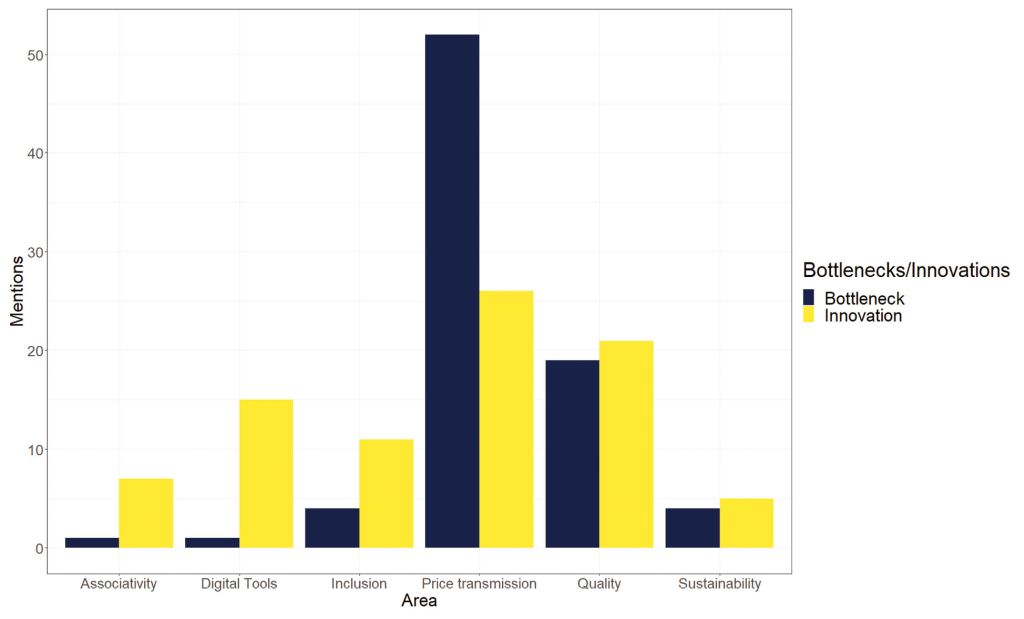

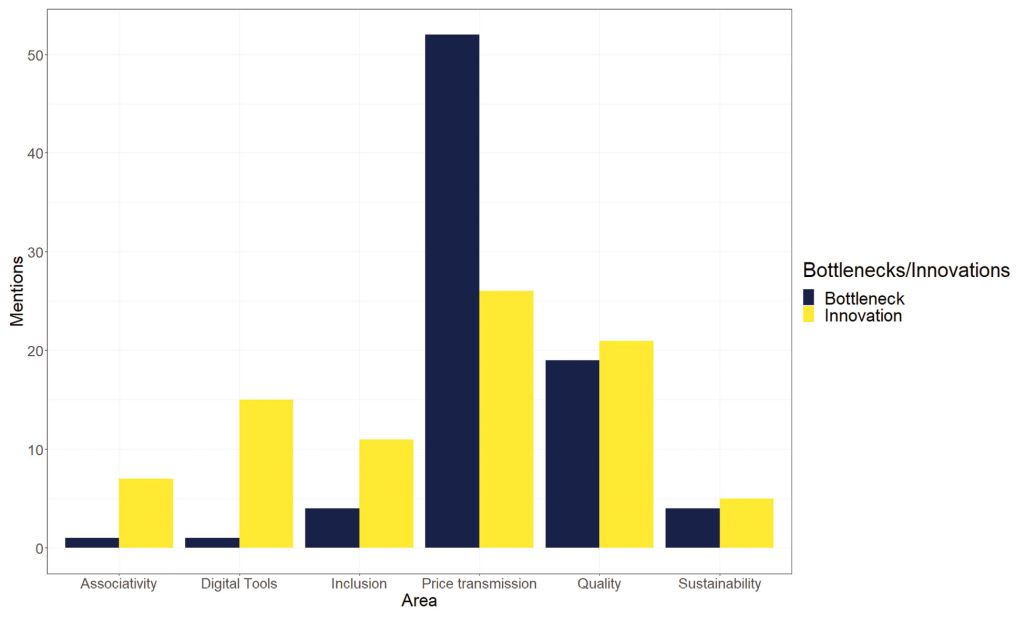

Across all areas of coffee production and trade, the literature cited 147 bottlenecks. These were classified into six broad categories: limited vertical coordination and price transmission, poor quality control, limited use of digital tools for information transfer, negative sustainability effects, and lack of gender and youth inclusion. Of these, 81 bottlenecks were retained for further analysis, while 66 were excluded as they did not align with the study’s core areas of interest. Table 2 presents the disaggregation of bottlenecks by focus area.

Bottlenecks identified through consultations.

Citation: International Food and Agribusiness Management Review 2026; 10.22434/ifamr.1303

Price transmission emerged as the most widely cited constraint, appearing in 64% of cases. Quality control followed, identified in approximately one in five studies. In contrast, gender and youth inclusion, along with environmental sustainability, received minimal attention, with only four mentions each. Associativity and digital tools for market information were scarcely discussed, with only one mention recorded in the literature.

3.1 Prioritization of problems

Three persistent conditions define the structure of the Honduran coffee value chain: the dominance of small and scattered producers and intermediaries, the bulky and perishable nature of coffee, and limited processing infrastructure. These conditions create constraints that are common in many commodity markets, particularly those involving smallholder production and perishable crops.

First, coffee production in Honduras is dominated by smallholders operating in geographically dispersed areas. This fragmentation makes it difficult for producers to coordinate, scale operations, or negotiate favorable terms with buyers. High transaction costs and low bargaining power leave producers as price takers, dependent on intermediaries who have greater control over market conditions. Similar dynamics are observed in other agricultural sectors where smallholders operate in fragmented markets with limited access to collective bargaining or market information.

Second, coffee is a bulky and perishable commodity that requires timely processing to maintain quality. High transportation costs, combined with inadequate infrastructure, force producers to sell quickly and locally, reducing their ability to take advantage of price fluctuations or access broader markets. These constraints are not unique to Honduras — smallholder farmers in many developing economies face similar logistical challenges when moving perishable products to market.

Third, the Honduran coffee sector lacks sufficient wet and dry processing infrastructure, limiting producers’ ability to add value and maintain quality consistency. Without access to processing facilities, farmers are often forced to sell at lower prices to intermediaries, missing opportunities for product differentiation and premium pricing. Similar processing constraints are seen in other agricultural sectors where small-scale producers struggle to access post-harvest handling and value-added processing.

Applying Sexton’s (1990) and Swinnen and Vandeplas’ (2015) framework, we identify the central challenge in the Honduran coffee value chain as a persistent inequity in bargaining power among actors. The structural conditions described above both enable and reinforce this imbalance, placing small producers at a disadvantage relative to larger intermediaries and exporters. Consultations with sector stakeholders confirmed key barriers to equitable market participation, including limited commercial skills, distrust in business relationships, and high fragmentation within the value chain. These findings align with broader trends in global agricultural markets, where smallholders frequently face disadvantages in negotiating power and value capture (Liu and Wang, 2021). Interviewees highlighted that small farmers often operate in areas with poor road infrastructure, with inadequate access to transportation, which increases transaction costs and limits market access.

This power asymmetry results in inefficiencies and an unequal distribution of value, limiting producers’ ability to capture the returns from their own production. As a result, many smallholder farmers remain trapped in cycles of low income and economic vulnerability, a challenge that extends beyond the Honduran coffee sector to other commodity markets characterized by weak producer bargaining power and high reliance on intermediaries. Key issues raised by interviewees also included the lack of adequate infrastructure for drying and wet processing, which limits farmers’ ability to improve quality and therefore capture higher premiums. The limited mechanization and poor post-harvest handling further undermine quality, leading to inconsistency between harvests and within the same harvest, which damages the reputation of Honduran coffee.

Our analysis highlights three key challenges shaping outcomes in the Honduran coffee value chain, which also hold relevance for understanding similar dynamics elsewhere (see Table 2): small, dispersed producers, a bulky and perishable product, and limited processing facilities. The lack of capacity in processing, coupled with insufficient drying methods, particularly mechanized drying, often results in low-quality coffee, even as the sector faces increasing market pressures to improve quality and traceability.

Main challenge: Mismatched bargaining power between farmers, small aggregators, and large intermediaries/exporters – Larger market actors capture a disproportionate share of value, while small producers and aggregators receive minimal returns. This imbalance fosters distrust and weakens vertical coordination across the supply chain (Martínez and Rodríguez, 2020).

Secondary challenge: Labor scarcity and informality – Low returns in coffee production contribute to persistent labor shortages. Informal employment arrangements further constrain productivity and sustainability while keeping rural wages low.

Secondary challenge: Limited quality contracting – Producers struggle to secure contracts that consistently reward quality. The absence of well-structured quality-based contracting mechanisms weakens incentives for improving coffee quality and restricts access to premium markets.

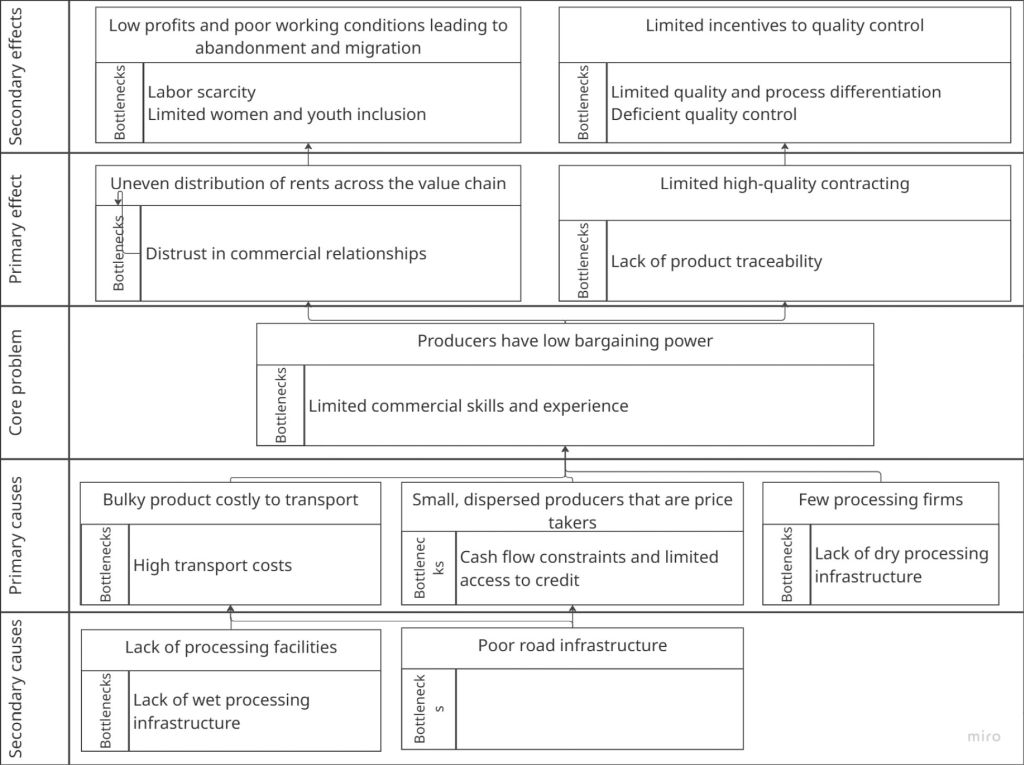

While these challenges are analyzed in the context of the Honduran coffee sector, they reflect broader structural issues in agricultural value chains where smallholders, perishable commodities, and limited processing capacity shape economic outcomes. Addressing these issues requires interventions that go beyond improving technical efficiency, instead targeting the institutional and market structures that influence bargaining power and value distribution. Figure 4 presents a problem tree based on the work of Sexton (1990) Swinnen and Vandeplas (2015), mapping how structural conditions — such as fragmented production, high transaction costs, and weak coordination — reinforce power imbalances and inefficiencies in the value chain. This framework highlights the interconnected nature of these challenges and the need for comprehensive strategies that address both market governance and producer agency.

Problem tree.

Citation: International Food and Agribusiness Management Review 2026; 10.22434/ifamr.1303

3.2 Mismatched bargaining power between farmers, small aggregators, and large intermediaries/exporters

Honduran coffee farmers face significant challenges due to their role as raw coffee producers and their limited capacity for collective bargaining. Without on-farm drying infrastructure, 85% of coffee is sold in its perishable form, either as cherry or wet parchment (Ruben et al., 2018). This creates significant logistical challenges for consolidation and processing into dry parchment (Álvarez, 2018). Transporting bulky, perishable coffee is costly, a problem exacerbated by chronically poor rural road infrastructure (Salazar et al., 2016). Farmers without their own transportation are forced to sell to local intermediaries, who then deliver the coffee to processors (Solstad, 2007; Smith and Loker, 2012; Romero et al., 2016; Ruben et al., 2018; Wiegel et al., 2020). Moreover, coffee production has outpaced processing capacity, making the value chain increasingly dependent on a small number of processing firms that establish relationships with intermediaries (Donovan, 2004; Silveira, 2005; IICA, 2011; Zhu, 2012; Peligros-Espada et al., 2018).

Intermediaries play a significant role in the Honduran coffee value chain, often acting as the only actors willing to absorb the transaction costs associated with sourcing coffee from small, dispersed farmers (Ruben et al., 2018; USAID, 2019). They provide essential services such as financing, which helps farmers during lean months (Álvarez, 2018; Hernández, 2020; Ruben et al., 2018). However, their dominant position in the market allows them to capture rents that could otherwise benefit farmers, particularly in a more balanced market (Álvarez, 2018; Eakin et al., 2006; Fromm and Dubon, 2006; Hernández, 2020; IICA, 2011; Orellana, 2022; Palma, 2013; Peña, 2019; Pérez, 2016; Piñuela, 2016; USAID, 2019; Wiegel et al., 2020). While this dominance is often viewed as exploitative, it is, in fact, a rational response to the market’s structural inefficiencies, where limited infrastructure and weak coordination leave intermediaries in a position of power. Their role, though vital, is complicated by these systemic issues that result in an inequitable distribution of value along the supply chain.

The concentration of buyers in the market has two main negative effects. First, it reduces the share of rents captured by coffee producers, directly affecting their livelihoods, as well as those of their families and employees. Second, it undermines incentives for quality. Private consolidators and processors rarely pay premiums for high-quality coffee due to their dominant local position, instead blending lower- and higher-quality coffee at various processing stages to meet export standards (Díaz, 2018; IICA, 2011; Orellana, 2022; Romero, 2019; Ruben et al., 2018). The lack of processing facilities further threatens quality, as wet coffee is highly susceptible to over-fermentation and spoilage (Donovan, 2004; IICA, 2011; Peligros-Espada et al., 2018; Silveira, 2005; Zhu, 2012). Additionally, with increasing regulatory requirements for traceability, market fragmentation poses further challenges for compliance (Wiegel et al., 2020).

State intervention has the potential to balance the coffee value chain (Shleifer, 1985). The Honduran Institute of Agricultural Marketing (IHMA) already purchases basic grains to maintain the national grain reserve (Thiebaud, 1985) and buys coffee at approximately 20% above the market price, promoting local production, generating employment, and strengthening the economy. However, calls for greater government involvement in the coffee sector have intensified in recent years (IICA, 2011), with stakeholders advocating for stricter controls on intermediaries. Proposals include requiring intermediaries to obtain trading permits and mandating payment based on quality. Yet, past regulatory efforts, such as the National Council for Coffee’s Ordinance for Internal Coffee Trading, have had limited impact (IICA, 2011).

Horizontal integration through producer cooperatives offers another mechanism to break local oligopsonies (Sexton, 1990; Smith, and Loker 2012; Margadant 2016; USAID 2019; Palma et al., 2020). This model has achieved some success in Honduras, improving price transparency (Chacón, 2015), centralizing processing (Álvarez, 2018; Augustin, 2019; Barbier et al., 2003; Eakin et al., 2006; Lara et al., 2011; Orellana, 2022; Piñuela, 2016), and enabling higher prices through process and quality differentiation (Alvarado, 2018; Augustin, 2019; Chacón, 2015; Orellana 2022; Ruben et al., 2018; Solstad, 2007; USAID, 2019). Cooperatives also provide farmer training (Alvarado, 2018; Fromm and Dubon, 2006; Ruben et al., 2018; Silveira, 2005), support risk management (Lara et al., 2011; USAID, 2019), and promote gender and youth inclusion (Alvarado, 2018; Chacón, 2015; Ruben et al., 2018). However, despite these benefits, cooperative membership stagnated at 15–20% in the 2010s (IICA, 2011; Álvarez, 2018). Past cooperative bankruptcies have eroded trust (Álvarez, 2018; Chacón, 2015; Ruben et al., 2018). Two additional factors explain low membership: first, cooperatives lose their competitive advantage when market prices rise above the Fair Trade price floor (Solstad 2007); second, cooperatives often delay payment, whereas intermediaries provide cash upfront, which farmers prefer (Lara et al., 2011; Smith and Loker, 2012; Solstad, 2007).

Empirical evidence highlights the extent of the problem. Figure 5 illustrates the price received by Honduran and Guatemalan farmers as a percentage of the ICO’s indicative price for “Other Milds.” Guatemalan farmers started the 21st century earning 80% of the ICO price and have steadily increased to 92% by 2019, rarely earning below 70%. In contrast, Honduran farmers started slightly above 60% and remained at similar levels by 2019, except for a brief increase between 2010 and 2013 when high coffee prices temporarily strengthened their bargaining power.

Price paid to growers in Guatemala and Honduras as a percentage of the ICO other milds composite price.

Citation: International Food and Agribusiness Management Review 2026; 10.22434/ifamr.1303

The persistently low share of coffee rents captured by Honduran farmers over the past two decades suggests that buyer power remains dominant in local markets. As of 2018, 80% of coffee was traded through the producer-intermediary-exporter channel, while cooperatives, which allow direct trading between producers and exporters, accounted for only 20% (Álvarez, 2018). Stakeholder consultations reinforced these findings, identifying downstream-upstream price transmission as the most significant bottleneck, mentioned 53 times. A more granular analysis (Table 2) highlights limited commercial skills, distrust in business relationships, and high value chain fragmentation as key challenges.

Interviewees also noted that in some areas, a long history of cooperative bankruptcies has led farmers to distrust cooperatives and seek other channels for trade. While cooperatives have been beneficial in some regions, in others, farmers prefer to work with intermediaries due to the poor track record of cooperatives in those regions. This lack of trust in cooperatives has contributed to their low membership and has left farmers more reliant on private intermediaries.

While precise estimates of the problem’s prevalence are difficult to obtain, available data provides some insight. Previous studies indicate that up to 39% of smallholder coffee is sold at the farm gate to larger farmers and intermediaries (Álvarez, 2018). The upper bound estimate suggests that as much as 85% of coffee is traded in perishable form. The true figure likely falls somewhere in between.

3.3 Labor scarcity and informality

The coffee labor market in Honduras operates largely informally, affecting both workers and producers in ways that extend beyond the sector itself. Between 800 000 and 1 million permanent and seasonal workers participate in coffee harvesting and processing (Mogrovejo, 2020; Orellana, 2022). Despite their critical role in the value chain, working conditions remain precarious, characterized by a lack of social security, high health risks, and minimal protections (Ruben et al., 2018). A significant challenge also lies in the aging workforce, with many farmers being of advanced age, and the lack of generational renewal further complicating labor availability. Additionally, there is a notable absence of young people joining the coffee sector, with migration to urban areas and abroad exacerbating this issue, as reported by several interviewees. These vulnerabilities discourage long-term workforce participation, exacerbating labor shortages and creating instability in production (Bunn et al., 2018; Hernández, 2020; Mogrovejo, 2020; Palma, 2013).

The lack of incentives to improve labor conditions stems from structural economic constraints. Small-scale producers, operating on thin profit margins, often cannot afford to offer formal employment benefits (Donovan and Blare, 2018). As a result, most coffee workers rely solely on wages, with no access to basic protections (Ruben et al., 2018, 2019). The Honduran social security system, concentrated in major cities, provides limited coverage, effectively leaving nine out of ten coffee workers without access to medical services. This dynamic mirrors broader trends in rural labor markets, where informality, weak institutional support, and the absence of enforcement mechanisms limit worker protections.

The economic health of the coffee sector has long been tied to migration and crime dynamics (Dube and Vargas, 2013). Christian Aid (1999) documented how the economic downturn following Hurricane Mitch and declining coffee exports contributed to increased gang membership. Similarly, FHI (2017) found a correlation between sectoral decline and rising international migration. The impact of migration has worsened in recent years, as young workers leave for urban areas or abroad, leaving a void in the workforce, which contributes to labor shortages in coffee production, according to interviews with stakeholders. While emigration from Honduras was relatively limited before the 1980s, the devastation caused by Hurricane Mitch in 1998 accelerated this trend, particularly among coffee workers, many of whom have since engaged in temporary or permanent migration to the United States.

Labor shortages also directly impact producers, as labor accounts for 43% of production costs in Honduras and 49% in Guatemala (Promecafe, 2018). In recent years, rising migration rates have led to chronic deficits of seasonal harvest workers, known as corteros (Peña, 2019; Piñuela, 2016; Wiegel et al., 2020). A key challenge is the low productivity of available workers, combined with the intensive labor demands of coffee farming, which are physically taxing and lead to worker fatigue and sickness, as pointed out by several interviewees. Media reports illustrate the growing difficulty in securing labor: while 650 000 workers were needed for the 2020 harvest, demand exceeded one million by 2022 (Canal 8, 2022; El Heraldo, 2020). Despite this rising demand, some regions filled only 50% of their labor needs (Canal 8, 2022). Industry leaders warn that if recent migration waves have been “laborer caravans,” the next wave will be “grower caravans,” as producers increasingly abandon coffee farming due to untenable labor constraints (Sullivan, 2006).

While the direct consequences of weak labor markets affect both workers and farmers, their ripple effects extend nationally and internationally. Domestically, informal labor relationships and exploitative conditions place an additional burden on Honduras’ already strained public healthcare system (Donovan and Blare, 2018; Mogrovejo, 2020). Internationally, large-scale migration from Central America has contributed to a humanitarian crisis at the U.S.-Mexico border, influencing foreign aid priorities and policy responses across the region (Reuters, 2019). Other structural forces, such as climate change and broader economic instability, may further intensify labor market pressures (Semple, 2019).

Evidence underscores the magnitude of these challenges. Studies consistently report that coffee workers often earn wages below the national minimum (Mogrovejo, 2020; Ruben et al., 2018), and illegal child labor remains a persistent issue (Donovan and Blare, 2018; Mogrovejo, 2020; Ruben et al. 2018). Consultations conducted for this study identified labor scarcity as the primary bottleneck, alongside concerns about the lack of generational renewal in the workforce. The shortage is also compounded by the low levels of specialization within the workforce, particularly in tasks like coffee harvesting, where workers often do not properly select coffee for quality. This lack of specialized skills limits the potential for higher wages, as farmers and intermediaries cannot access higher-value markets or improve the quality of their coffee. As a result, wages remain low, and workers continue to face precarious conditions, as the value of the coffee produced is constrained by the quality issues arising from unskilled labor.

Estimates suggest that approximately 1 million people work in the Honduran coffee sector, 300,000 of whom hold permanent positions. While precise data on social security affiliation is lacking, Mogrovejo (2020) indicates that coverage rates within the sector are significantly below the national average. Assuming a 20% affiliation rate, at least 800 000 coffee workers lack social protections. Some estimates paint an even starker picture: the International Labor Organization (ILO) states that social protection provisions in the Honduran coffee sector are virtually nonexistent (ILO, 2024).

These patterns, while examined in the context of Honduras, highlight how the truncation of value flows to workers is not solely driven by farmers’ desire to pay less, but is also compounded by a lack of worker specialization and their itinerant nature. These challenges make it difficult for farmers to support workers with long-term social security benefits, as their labor is often seasonal and unskilled. The lack of specialization in the workforce limits the quality of coffee harvested and, in turn, affects the wages that workers can earn. Addressing this issue requires a multifaceted approach, focusing not only on providing economic incentives for formalizing employment but also on investing in skills development, improving labor conditions, and strengthening the capacity of the coffee sector to provide long-term, sustainable employment opportunities for workers.

3.4 Limited quality contracting

Lower-quality conventional coffee moves through intermediaries, while higher-quality differentiated coffee is more closely associated with cooperatives. Cooperatives focus on differentiated coffee as a commercial strategy to attract more producers by offering better prices. Some, such as the COMSA cooperative, the Marcala Denomination of Origin, and cooperatives in Western Honduras, leverage geographic branding to distinguish their coffee. At the highest end, gourmet coffee is sold through direct producer-exporter channels, although this accounts for less than 1% of the total coffee traded.

The configuration of these channels is shaped by the search, monitoring, and contracting costs incurred by buyers (Swinnen and Vandeplas, 2015). Both direct purchase and cooperative-led channels exemplify high-value contracting, but they address transaction costs differently. Direct purchase channels prioritize coffee quality and its potential for price premiums, making it feasible for buyers to source coffee directly. Meanwhile, cooperatives reduce search and monitoring costs by aggregating high volumes, attracting buyers, and securing more formal contracts (IICA, 2011). Even lower-quality coffee benefits from this approach. However, for 85% of Honduran coffee, search and monitoring costs exceed the price premiums achievable through high-value contracting, excluding it from these channels.

High-value contracting must contend with geographically dispersed growers and variability in processing and quality. While geographic and environmental conditions serve as rough proxies for coffee quality (Decazy et al., 2003; Mickle, 2009), the realized quality depends equally on agronomic practices, processing methods, and storage conditions. To bridge these gaps, local buyers rely on anecdotal information and experience to refine their selection. Because quality information is costly to obtain, it is guarded closely (Zhu, 2012), making it even more expensive for international buyers to assess.

Beyond identifying high-quality suppliers, buyers must also monitor compliance with sanitary standards and ensure that coffee is processed in ways that preserve its intrinsic characteristics. Some defects are visually detectable, but more subtle flaws require cupping, a costly process given the scale of Honduran coffee production.

Contract breaches are common in the Honduran coffee supply chain. Cooperatives, in particular, have faced a steep learning curve in global markets. Initially, their limited marketing capacity forced them to sell coffee locally at depressed prices when they failed to secure export buyers (Ruben et al., 2018; Smith and Loker, 2012). Over time, they improved processing to meet quality and consistency requirements. More recently, they have relied on sustainability certifications to gain a competitive edge when prices are low. However, Fair Trade price floors limit their profitability when market prices are high. In such cases, intermediaries offer better prices, making it difficult for cooperatives to secure the volumes needed to fulfill contracts (Smith and Loker, 2012). This inconsistent history partly explains why cooperative membership remains low and why their market share in direct exports is marginal. In 2018, cooperatives accounted for only 3.4% of Honduran coffee exports (Álvarez, 2018).

Empirical evidence underscores the extent of this problem. In 2022, less than half of Honduran coffee exports were conventional, fetching prices nearly identical to ICE Coffee C futures contracts. The remaining 54% fell under some form of differentiation, a growing segment in Honduras. On average, these coffees commanded a 40-cent premium over conventional coffee. However, the nature of differentiation varies. Only 5% of differentiated coffee was sold based on quality or origin, including categories such as Gourmet, Marcala Denomination of Origin, Project Origin, and Cup of Excellence, which commanded premiums exceeding five dollars per pound. The remaining 95% relied on sustainability certifications like Rainforest Alliance, Fair Trade, Organic, UTZ, 4C, C.A.F.E. Practices, and Lift Program (Donovan and Blare, 2018). While these certifications signal progress toward better market outcomes, they do not necessarily reflect higher intrinsic quality. The limited volume of coffee traded based on quality suggests that this market segment remains underdeveloped and still lags behind regional competitors (Figure 6).

Price of Guatemalan and Honduran coffee compared to ICO composites for other milds and Brazilian naturals.

Citation: International Food and Agribusiness Management Review 2026; 10.22434/ifamr.1303

The prevalence of low-quality contracting is difficult to quantify since coffee sales contracts are private. However, reasonable inferences can be made. Conventional coffee, which accounts for about half of Honduran exports, is likely sold through low-quality channels. If sustainable coffees are included in the definition of high-quality, the estimate narrows to 47–48%. However, if high quality is defined strictly as coffee with superior organoleptic characteristics or identifiable origin, then as much as 99% of Honduran coffee would fall outside high-value contracting. While Honduras has improved coffee quality over the last 16 years, it still lags behind Guatemala (Figure 7).

Coffee qualities exported by Honduras and Guatemala, 2005 vs 2021. HG, high grown; SHG: strictly high grown; SL, standard lot.

Citation: International Food and Agribusiness Management Review 2026; 10.22434/ifamr.1303

One of the primary challenges hindering high-value contracting is the lack of consistent quality management and limited infrastructure. Interviewees highlighted that many farmers still fail to properly select and process their coffee, leading to inconsistent quality. As one participant noted, “The management of post-harvest processes is poor, despite efforts by IHCAFE to improve quality. Producers often do not separate coffee by harvest date or mix lots, which leads to inconsistencies.” This lack of quality control contributes to Honduras’ reputation for inconsistent coffee, making it difficult for Honduran coffee to secure better prices in premium markets.

Another critical issue is the lack of awareness among producers about the financial benefits of improving quality. According to interviewees, many producers do not see the immediate returns of investing in better quality production practices, especially when market prices fluctuate. As one interviewee pointed out, “The producer does not understand that improving quality will lead to higher profits in the long run. They are too focused on the volatile short-term prices.” This perception further limits the transition to higher-quality coffee production.

Additionally, the lack of differentiation in the market and the focus on volume over quality have resulted in Honduras continuing to sell a significant portion of its coffee as conventional, despite improvements in quality over the years. The dominance of sustainability certifications, rather than intrinsic quality, further complicates this issue. Interviewees emphasized that, “Honduran coffee has improved in quality, but the market still focuses more on volume than on quality differentiation.”

4. Analysis of potential innovations

Stakeholders identified 178 innovations in all areas related to coffee production and sale. We focused on innovations related to the coffee value chain — vertical coordination, quality upgrading, information transmission through digital tools, and the two transversal areas of interest: environmental sustainability, and gender and youth inclusion. Eighty-five innovations are related to the coffee value chain. Table 3 shows the disaggregation of the innovations by area of focus:

Innovations identified through consultations.

Citation: International Food and Agribusiness Management Review 2026; 10.22434/ifamr.1303

The primary causes identified in this problem tree, which coincide with Sexton (1990), conditions for the existence of local oligopsonies, offer three lanes of action that have been explored to a larger or lesser extent. Three innovation areas for action are: (i) sell dry parchment coffee through high-quality contracts, (ii) strengthen cooperatives’ managerial and commercial capabilities, and (iii) sell their coffee through better, more transparent channels. Addressing bottlenecks in these three areas (Figure 8) can help break the hold of local oligopsonies. The remainder of this section looks at each alternative.

Number of bottlenecks vs innovations identified through consultations.

Citation: International Food and Agribusiness Management Review 2026; 10.22434/ifamr.1303

4.1 Farmers sell dry parchment coffee through high-quality contracts

Innovation 1 (Figure 9) addresses the sale of coffee in its perishable form, a critical issue given that perishable coffee is susceptible to quality deterioration in mild cases and product degradation that can pose health risks in extreme cases. Coffee begins to degrade rapidly after harvest, making drying one of the first steps in preserving quality. To meet international standards, coffee must be dried to a moisture content of 10–12%, reducing perishability and enabling safe storage for up to six months if properly handled. Two primary methods are used to dry wet parchment coffee: farmer-dried and industrial-dried.

Innovation tree.

Citation: International Food and Agribusiness Management Review 2026; 10.22434/ifamr.1303

Farmer-dried coffee relies on in-farm drying infrastructure, which can be solar-based or fuel-based. Solar drying typically involves raised beds covered with protective material to shield beans from rain, while fuel-based drying uses fossil fuels to generate heat, which is then circulated through the beans to remove moisture. Both systems have limitations. Solar drying depends on sufficient radiation, which varies by region and weather conditions, while fuel drying requires access to affordable fuel, which is not always available. Additionally, both methods require an initial investment that may be prohibitive for cash-constrained farmers.

By reducing perishability at the farm level, this innovation expands market opportunities, allowing farmers to sell dry beans directly to buyers. An estimated 31% of Honduran farmers could sell dry-bean coffee at the farmgate, bypassing intermediaries and increasing their market power. Others would still sell to processors and intermediaries but under improved conditions. In-farm drying has the potential to break existing market power asymmetries, enabling farmers to negotiate better prices. This model is already widely implemented in other smallholder coffee-producing countries, such as Colombia.

An additional benefit of on-farm drying is that it facilitates quality assessment. Dry parchment coffee undergoes physical, chemical, and biological defect screening, and its organoleptic qualities can be evaluated through cupping. These quality assessments are not possible with wet coffee, making drying a prerequisite for accessing quality-based price premiums.

4.2 Managerial and commercial capabilities of cooperatives are strengthened

Innovation 2 seeks to address the negative reputation of cooperatives among Honduran coffee farmers by revitalizing them to function effectively within the value chain, as they do in other countries. Strengthening cooperatives in networking, administration, and marketing can directly enhance the welfare of their members while indirectly increasing the competitiveness of coffee markets.

Agricultural cooperatives provide significant benefits to small-scale farmers. By pooling resources, farmers can negotiate better prices for their coffee, access more favorable markets, and attract buyers through collective bargaining. Cooperatives also improve overall market competitiveness, benefiting even non-member farmers by reducing market imperfections (Tennbakk, 1995).

Beyond market access, cooperatives facilitate financing, training, and technical assistance for small-scale farmers. They can secure credit from banks, government agencies, or other funding sources and lend it to members at competitive rates. This financial support enables farmers to purchase essential inputs such as fertilizers, pesticides, and equipment that would otherwise be unaffordable. Additionally, cooperatives provide training in certification compliance, best farming practices, pest and disease management, and post-harvest handling, improving both the quality and quantity of coffee production. These improvements enhance farmers’ income potential while also promoting gender empowerment and youth inclusion (Rubio-Jovel, 2021).

4.3 Intermediaries sell their coffee through better, more transparent channels

Private intermediaries dominate Honduras’ coffee market, often serving as the only actors willing to absorb the contracting costs associated with sourcing coffee from small, dispersed farmers. If Innovations 1 and 2 prove unfeasible, collaboration with intermediaries becomes essential. While private intermediaries tend to deliver worse welfare outcomes than public firms or cooperatives (Sexton, 1990; Tennbakk, 1995), they remain central to the value chain because they maximize private profit rather than social welfare.

However, some private intermediaries offer cooperative-like benefits. A key example is Beneficio Rio Frio in San Nicolás, Santa Bárbara, which has built strong social capital over three generations as the region’s main coffee buyer. As a result, it provides fair payment schemes and transparent weighing while purchasing coffee in cherry, wet, and dry parchment forms. The challenge is how to replicate this model in cases where intermediaries lack the deep-rooted social capital of Rio Frio.

One emerging solution is the growing demand for traceability, driven by both fair price transmission and sustainability requirements. Blockchain technologies have been introduced to enhance transparency, offering a potential mechanism to build trust and accountability among intermediaries, farmers, and buyers.

5. Conclusion

The Honduran coffee value chain is a complex and dynamic system involving smallholder farmers, intermediaries, and cooperatives, whose interactions shape the overall performance and competitiveness of the sector. Smallholder farmers are the backbone of the industry, responsible for most coffee production, yet they face significant challenges, including limited access to funding and technology, which hinder their productivity and profitability. Many operate within oligopsonistic local markets, where they sell coffee under disadvantageous conditions. Addressing these structural issues through in-farm drying facilities, improved road infrastructure, and centralized processing facilities can help break these imperfect markets.

Cooperatives play a crucial role in mitigating these challenges by providing smallholder farmers with access to markets, finance, and training, strengthening their competitiveness and bargaining power. By pooling resources, farmers can access opportunities that would otherwise be out of reach, including better market linkages and technical support. However, cooperatives in Honduras suffer from a reputation of instability due to frequent bankruptcies. Strengthening their networking, managerial, and commercial capacities could enhance their impact and restore trust in their role within the value chain.

Intermediaries, including domestic traders and exporters, also play a critical role by linking smallholder farmers to international markets and providing essential services to facilitate production and income generation. Despite their importance, they are often criticized for capturing a disproportionate share of the value chain’s rents. However, intermediaries are frequently the only actors willing to bear the transaction costs associated with sourcing small volumes of coffee from dispersed producers. This raises an important question: can their role be improved in a way that benefits all stakeholders? If so, how?

Acknowledgements

The CGIAR Research Initiative on Rethinking Food Markets and Value Chains for Inclusion and Sustainability sponsored this analysis. CGIAR launched Rethinking Markets with national and international partners to leverage markets and value-chains to address nutrition, livelihoods, and environmental concerns in food systems. Six CGIAR centers — International Water Management Institute (IWMI), Alliance of Bioversity International and the International Center for Tropical Agriculture (Alliance Bioversity-CIAT), International Institute of Tropical Agriculture (IITA), International Maize and Wheat Improvement Center (CIMMYT), International Center for Agricultural Research in the Dry Areas (ICARDA), and WorldFish — carry out the initiative at national and subnational levels in seven countries in Africa, Asia, and Latin America. We thank all funders who supported this research through their contributions to the CGIAR Trust Fund. Opinions are those of the authors and not necessarily those of CGIAR. We also extend our gratitude to those who have supported us throughout the research and writing of this document. Special thanks go to Mirian Colindres and Miguel Gomez for their assistance during the consultation phases. Their insights and expertise significantly contributed to the depth and accuracy of our analysis.

References

Christian Aid. 1999. In debt to disaster: what happened to Honduras after Hurricane Mitch. Christian Aid, London.

Alvarado, R.F. 2018. Diseño de un sistema híbrido renovable para una planta procesadora de café en Honduras. Available online at https://riunet.upv.es/handle/10251/108975

Álvarez, M.Á. 2018. Análisis de la cadena de valor del café en Honduras. Heifer International. Tegucigalpa.

Augustin, J. 2019. Análisis de indicadores de sostenibilidad en tres sistemas de producción de café: convencional, orgánico y especial, en los municipios de Morocelí, Marcala y Santa Elena, en Honduras. Available online at https://bdigital.zamorano.edu/handle/11036/6542

Barbier, B., R.R. Hearne and J.M. Gonzalez 2003. Trade-off between economic efficiency and contamination by coffee processing: a bioeconomic model at the watershed level in Honduras. Available online at https://agritrop.cirad.fr/515144

Bunn, C., M. Lundy, P. Läderach, E. Girvetz and F. Castro 2018. Climate smart coffee in Honduras. International Center for Tropical Agriculture (CIAT), United States Agency for International Development (USAID). Cali, Colombia. Available online at https://hdl.handle.net/10568/97530

Canal 8. 2022. Un millón de corteros se requieren para la cosecha de café. Available online at https://tnh.gob.hn/nacional/un-millon-de-corteros-se-requieren-para-la-cosecha-de-cafe/

Chacón, L. and O. Gabarrete 2015. Sistematización participativa de la experiencia de la cadena de valor del café de La Labor, Ocotepeque, Honduras. Available online at https://repositorio.catie.ac.cr/handle/11554/7199

Decazy, F., J. Avelino, B. Guyot, J.-J. Perriot, C. Pineda and C. Cilas 2003. Quality of different Honduran coffees in relation to several environments. Journal of Food Science 68: 2356–2361. https://doi.org/10.1111/j.1365-2621.2003.tb05763.x

Díaz, N.I. 2018. Análisis de factibilidad para establecer una central de beneficio húmedo de café en El Paraíso, El Paraíso, Honduras. Available online at https://bdigital.zamorano.edu/handle/11036/6249

Donovan, J. 2004. Rural enterprise development involving small producers: towards strategic specialty-coffee networks in Nicaragua and Honduras. Available online at https://repositorio.catie.ac.cr/handle/11554/10112

Donovan, J. and T. Blare 2018. Evaluation of UTZ certification with a focus on coffee businesses in Guatemala, Honduras and Nicaragua>. ICRAF Working Paper - World Agroforestry. Available online at https://www.cabdirect.org/cabdirect/abstract/20193289326

Dube, O. and J.F. Vargas. 2013. Commodity price shocks and civil conflict: evidence from Colombia. The Review of Economic Studies 80: 1384–1421. https://doi.org/10.1093/restud/rdt009

Eakin, H., C. Tucker and E. Castellanos 2006. Responding to the coffee crisis: a pilot study of farmers’ adaptations in Mexico, Guatemala and Honduras. Geographical Journal 172: 156–171. https://doi.org/10.1111/j.1475-4959.2006.00195.x

El Heraldo. 2020. Caficultores urgen de personal para cortar café en zona oriental. Available online at https://www.elheraldo.hn/honduras/caficultores-urgen-personal-para-cortar-cafe-en-zona-oriental-ABEH1432288

FHI 360. 2019. Coffee price risk management models: Guatemala and Honduras summary of findings and potential innovations. Available online at https://agrilinks.org/sites/default/files/resources/price_risk_management_deliverable_2_country_findings_and_prmms_potential_interventions_0.pdf

Fromm, I. and J.A. Dubón. 2006. Upgrading and the value chain analysis: the case of small-scale coffee farmers in Honduras. In: Conference on International Agricultural Research for Development, University of Bonn, October 11–13, 2006.

Hernández, J.O.L. 2020. Procesos y mecanismos de desigualdad en pequeños productores de café en la región occidental de Honduras. El caso de San Juan, Intibucá. Revista Latinoamericana de Estudios Rurales 5: e494. Available online at http://www.ceil-conicet.gov.ar/ojs/index.php/revistaalasru/article/view/494

IHCAFE 2016. Informe estadístico IHCAFE 2015–2016. IHCAFE, Tegucigalpa.

IHCAFE 2021. Informe estadístico IHCAFE 2020–2021. IHCAFE, Tegucigalpa.

IICA. 2011. Desarrollo competitivo de la cadena de valor del café en postcosecha y comercialización interna en Honduras. Instituto Interamericano de Cooperación para la Agricultura (IICA), Tegucigalpa. Available online at https://repositorio.iica.int/handle/11324/11826

International Labour Organization (ILO). 2024. Mapping the coffee value chain in Honduras. CLEAR Supply Chains project, ILO, Geneva. https://www.ilo.org/sites/default/files/2024-07/Honduras_Coffee_Value_Chain_Mapping.pdf

Lara, L., B. Rapidel, D. Stoian, J. Argüello, T. Gaitán and C. González 2011. Estudio de factibilidad para la implementación de seguros basados en índices climáticos en el cultivo de café en Honduras y Nicaragua. CATIE, Turrialba. Available online at https://repositorio.catie.ac.cr/handle/11554/9223

Liu, Y. and Q. Wang. 2021. Value chain analysis in the agribusiness sector: Challenges and opportunities for smallholder inclusion. International Food and Agribusiness Management Review, 24(2), 153–170. https://doi.org/10.22434/IFAMR2021.0123

Liverpool-Tasie, L.S.O., A. Wineman, S. Young, J. Tambo, C. Vargas, T. Reardon, G.S. Adjognon, J. Porciello, N. Gathoni, L. Bizikova, A. Galiè and A. Celestin. 2020. A scoping review of market links between value chain actors and small-scale producers in developing regions. Nature Sustainability 3: 799–808. https://doi.org/10.1038/s41893-020-00621-2

Margadant, F. 2016. Overcoming the thin months in coffee - how diversification can generate stable and higher incomes in Marcala (Honduras). Available online at https://www.poverty.ch/wp-content/uploads/2017/10/Fabiana_Margadant_MA.pdf

Martínez, R. and A. Rodríguez. 2020. Enhancing market efficiency in agribusiness value chains: Insights from Latin American agriculture. International Food and Agribusiness Management Review, 23(4), 405–422. https://doi.org/10.22434/IFAMR2020.0158

Mickle, E. 2009. Using GIS to locate areas for growing quality coffee in Honduras. Available online at https://digitalcommons.unl.edu/envstudtheses/3/

Mogrovejo, C.R. 2020. Incentivos y limitaciones para la mejora de la seguridad y salud en el trabajo en la cadena mundial de valor del café de Honduras. ILO, Geneva.

Orellana, E.L.R. 2022. Efectos de la cadena de valor del café en el desarrollo socioeconómico de los pequeños cafetaleros de Corquín, departamento de Copán-Honduras. Ciencia Latina Revista Científica Multidisciplinar 6: 1606–1623. Available online at https://ciencialatina.org/index.php/cienciala/article/view/3107

Palma, O.M., J.M. Díaz-Puente and J.L. Yagüe 2020. The role of coffee organizations as agents of rural governance: evidence from Western Honduras. Land 9: 390. https://doi.org/10.3390/land9100390

Peligros-Espada, C., J.U. Sevilla-Palma and O. Uña-Juarez. 2018. Importance of crop altitude range for coffee production: findings from Honduras. Journal of Agricultural Science and Technology 20: 879–892. https://www.researchgate.net/publication/324916039

Peña, J.H.O. 2019. Hacia otro paradigma de economía política del café y desarrollo humano en el occidente de Honduras. Revista Perspectivas del Desarrollo 4: 46–63. https://lamjol.info/index.php/RPDD/article/view/11965

Pérez, C.C. 2016. Estudio de factibilidad para la elaboración e implementación de un plan de capacitación y asistencia técnica para pequeños productores de café del municipio de Opatoro, departamento de La Paz, Honduras, Centro América. Available online at https://tzibalnaah.unah.edu.hn/xmlui/handle/123456789/2789

Piñuela, K.M.C. 2016. Análisis de las líneas de acción de valor agregado, calidad y fortalecimiento institucional del proyecto de cooperación Café AECID referentes a la obtención de la denominación de origen del café de Marcala (Honduras) y su aplicabilidad en Zamora Chinchipe (Ecuador). Available online at http://repositoriointerculturalidad.ec/jspui/handle/123456789/3033

Promecafe. 2018. El estado actual de la rentabilidad del café en Centroamérica. Central American Business Intelligence, Guatemala City.

Reuters. 2019. As promised, Trump slashes aid to Central America over migrants. Available online at https://www.reuters.com/article/us-usa-immigration-trump/as-promised-trump-slashes-aid-to-central-america-over-migrants-idUSKCN1TI2C7

Romero, J.P. 2019. Relevo generacional en la industria del café. Caso: Finca San Isidro, Honduras. Available online at https://bdigital.zamorano.edu/handle/11036/6620

Romero, Z.J.R., N. Sibrian and J. Francisco 2016. Estudio de la estructura de mercado de la comercialización del café en Honduras. Available online at https://bdigital.zamorano.edu/handle/11036/5874

Ruben, R., P. Sfez, T. Pensioen and N. Meneses 2018. Análisis integral de la cadena de valor del café en Honduras: informe final. Available online at https://library.wur.nl/WebQuery/wurpubs/fulltext/450336

Rubio-Jovel, K. 2021. Gender empowerment in agriculture innovations: what are we still missing? Evidence from a randomized-controlled trial among coffee producers in Honduras. Frontiers in Sustainable Food Systems 5: 695390. https://doi.org/10.3389/fsufs.2021.695390

Salazar, A., M. Nevo, D. Torres-Gracia, R. Rodríguez-Molina, E. Café, L. Montes, M. Romero, A. Monje, D. Corrales, T. Aliouat, M.C. del Puerto and N. Morales. 2016. Regional Road Integration Program II: Loan Proposal. Inter-American Development Bank, Washington, DC.

Semple, K. 2019. Central American farmers head to the US, fleeing climate change. The New York Times (13 April). Available online at https://www.nytimes.com/2019/04/13/world/americas/coffee-climate-change-migration.html

Sexton, R.J. 1990. Imperfect competition in agricultural markets and the role of cooperatives: a spatial analysis. American Journal of Agricultural Economics 72: 709–720. https://doi.org/10.2307/1242567

Sevilla-Palma, J.U. 2013. Análisis de la agroindustria de exportación de Centroamérica: evaluación económica y sostenible de la producción de café de Honduras. Tesis doctoral, Universidad Rey Juan Carlos, Madrid. Available online at https://burjcdigital.urjc.es/handle/10115/12287

Shleifer, A. 1985. A theory of yardstick competition. The RAND Journal of Economics 16: 319–327. https://doi.org/10.2307/2555505

Silveira, N.D. 2005. Sostenibilidad socioeconómica y ecológica de sistemas agroforestales de café (Coffea arabica) en la microcuenca del río Sesesmiles, Copán, Honduras. Available online at https://repositorio.catie.ac.cr/handle/11554/5553

Smith, E. and W. Loker 2012. “We know our worth”: lessons from a fair trade coffee cooperative in Honduras. Human Organization 71: 87–95. https://doi.org/10.17730/humo.71.1.w7x76q3n215h1301

Solstad. G. 2007. Organic and Fair Trade Coffee: Diverging Experiences Among Smallholders in Honduras. University of Oslo. Available online at https://www.duo.uio.no/bitstream/handle/10852/32684/1/solstad.pdf

Sullivan, M.P. 2006. Honduras: Political and economic situation and US relations. Library of Congress, Congressional Research Service, Washington DC.

Swinnen, J. and A. Vandeplas 2015. Price transmission in modern agricultural value chains: some conceptual issues. Food Price Dynamics and Price Adjustment in the EU 147: 148–166. https://doi.org/10.1016/B978-0-12-804114-7.00008-4

Tennbakk, B. 1995. Marketing cooperatives in mixed duopolies. Journal of Agricultural Economics 46: 33–45. https://doi.org/10.1111/j.1477-9552.1995.tb00996.x

Thiebaud, J.A. 1985. The role of the Honduran Institute of Agricultural Marketing (IHMA). Thesis, Kansas State University, Manhattan, KS.

United States Agency for International Development, FHI 360 2017. Honduras Labor Market Assessment. FHI 360, United States Agency for International Development, Washington, DC. Available online at https://www.fhi360.org/sites/default/files/media/documents/resource-honduras-lma-report.pdf

Wiegel, J., M. del Río, J.F. Gutiérrez, L. Claros, D. Sánchez, L. Gómez, C. González and B.A. Reyes 2020. The coffee market system in Honduras: opportunities for supporting renovation and rehabilitation. Alliance Bioversity and CIAT. Available online at https://hdl.handle.net/10568/108108

Zhu, L. 2012. A preliminary investigation of the impact of Union Micofinanza on coffee producers in La Union, Honduras. Available online at https://repository.upenn.edu/sire/13/

Appendix A: Protocol used in the systemic review of the literature

Search strategy:

We conducted a search of the following bibliographic databases, using the Publish or Perish app:

Google Scholar

Scopus

Additional searches will be conducted in the following databases and websites to capture additional peer-reviewed research, non-peer-reviewed research, and gray literature:

AgEcon Search (https://ageconsearch.umn.edu/collections/)

CGSpace (CGIAR) (http://cgspace.cgiar.org)

Escuela Agrícola Panamericana - Zamorano’s Wilson Popenoe digital repository (https://bdigital.zamorano.edu/home)

Centro Agronómico Tropical de Investigación y Enseñanza - CATIE’s digital repository (https://repositorio.catie.ac.cr/)

Keywords and phrases used in the database searches.

Citation: International Food and Agribusiness Management Review 2026; 10.22434/ifamr.1303

Appendix B: Questionnaire used in the consultations (Spanish)

WP1: Cadenas de valor integradas globalmente, inclusivas, eficientes y ambientalmente sostenibles

Estudio exploratorio: cadena del café en Honduras y Guatemala v. 4/11/2022

Citation: International Food and Agribusiness Management Review 2026; 10.22434/ifamr.1303

LEER LA DECLARACIÓN DE CONSENTIMIENTO INFORMADO

Encuestador, responda: Doy fe de que he leído el consentimiento a la persona entrevistada y está de acuerdo en ser entrevistados y ha dado su consentimiento de manera verbal _____Sí _____No

Firma del encuestador (para dar fe que el consentimiento fue leído): _____________________

Información básica de la persona/organización

¿Hace cuánto y en qué roles ha estado usted involucrado en el sector café en Centroamérica?

La organización, ¿dónde opera o en qué regiones tiene actividades relacionadas con la comercialización del café? (Municipios, departamento, etc., separe zonas productivas de zonas de comercialización si éstas son diferentes)

Cuellos de botella

Ahora vamos a hablar un poco sobre cuellos de botella que Ud. logre identificar a lo largo de la cadena de valor:

¿Cuáles considera que son los tres (o cinco) principales cuellos de botella a lo largo de la cadena del café de Honduras? Por favor descríbalos, y de ser posible, separe por tipo de actor (si es que varían por tipo de actor).

¿Qué injerencia tiene usted/su organización sobre estos cuellos de botella?

¿Qué otros actores tienen injerencia sobre esos cuellos de botella?

Innovaciones implementadas o potenciales

Explicar al entrevistado:

La innovación es una idea amplia, por ejemplo: a) La innovación es producir un nuevo producto con tecnología existente b) La innovación es producir un producto existente con nueva tecnología/organización/proveedores c) La innovación es producir un producto existente en un nuevo lugar d) La innovación es vender productos existentes en nuevos lugares/ a nuevos consumidores e) cambiar para hacer más eficientes las relaciones de negocios o las relaciones entre actores de la cadena de valor

Para cada cuello de botella identificado en la sección anterior preguntar:

Para los cuellos de botella identificados en la sección anterior, ¿usted o su organización han implementado innovaciones? Cuénteme al respecto.

¿Qué resultados positivos obtuvo de la implementación de esta innovación?

¿Cuántos actores han implementado la innovación? ¿Unos pocos, algunos, muchos?

¿Qué dificultades tuvo en la implementación de esta innovación? Si tuviera la posibilidad, ¿Cómo los corregiría?

Para los cuellos de botella identificados en la sección anterior, ¿qué innovaciones ha visto implementadas por otros actores de la cadena de café?

¿Tiene alguna noción de qué tan efectiva fue esa innovación?

En caso de ser posible, ¿Usted/su organización implementaría esa innovación? ¿Por qué sí o por qué no?

-

Para los cuellos de botella identificados en la sección anterior, ¿qué innovaciones considera se pueden implementar, pero aún no han sido implementadas por ningún actor de la cadena?

¿Por qué no se ha promovido/adoptado a gran escala? ¿Qué se necesitaría para lograr esto?

¿Qué riesgos se pueden presentar para que los productores adopten nuevas innovaciones, o que las innovaciones se puedan implementar con éxito?

Temas de interés especial

¿Conoce o ha implementado innovaciones para incrementar la participación de mujeres y jóvenes en la cadena de valor de café de Centroamérica? Cuénteme sobre su objetivo e impacto.

¿Conoce o ha implementado innovaciones para mejorar la sostenibilidad ambiental de la cadena de valor de café de Centroamérica? Cuénteme sobre su objetivo e impacto.

¿Conoce o ha implementado innovaciones digitales1 dentro de la cadena de valor de café de Centroamérica? Cuénteme sobre su objetivo e impacto. ¿Cuáles son los factores que influencian que se puedan desarrollar estas innovaciones digitales?

Oportunidades de colaboración

Si esta iniciativa decidiera implementar alguna de las innovaciones que usted menciona, ¿usted/su organización estaría interesado en participar de esta iniciativa? ¿En qué calidad?

Finalmente, ¿qué otras organizaciones consideran estratégicas que debamos entrevistar acerca de estos temas? (favor proveer nombre, celular, email de contactos)

Corresponding author

Las innovaciones digitales son aquellos productos o servicios que recolectan, guardan, analizan y comparten información digitalmente. Pueden prestar diversos servicios, como asesoría técnica y extensión, actividades en el cultivo y postcosecha, servicios financieros, conexión con los mercados y gestión a lo largo de la cadena.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}