Abstract

In November 2018, John Warrington, CEO of Cacao Oro de Nicaragua, was about to share a recommendation that would surely change the companyâs future. Over the last few weeks, John had engaged in analyzing the evolution of the company and the implications for its future. As a result, he felt the need to formulate a competitive strategy to guide the expansion in the next few years. He identified four market options: first, to focus on bulk cocoa, with commodity prices and high-volume transactions; second, to specialize in fine or flavor cocoa, with high price premiums and low-volume transactions; third, to focus on certified bulk cocoa, with small price premiums and high-volume transactions; and, finally, to develop a âmixedâ strategy with a combination of the three previous options. A few years earlier, plans were underway to develop 10 000 ha of cocoa in Nicaragua to become the worldâs largest cocoa producer. To start the venture, the first effort was to restore a 3000-ha farm in Rosita, a region on the Atlantic coast of Nicaragua, damaged by Hurricane Félix in 2008. In 2014, Cacao was born with restoration works to enable 2000 ha for cocoa cultivation. The first harvest in 2017 confirmed that the project was on the right track. And John thought that the time was ripe to reflect on the companyâs future strategy.

The Teaching Note to this article can be accessed at 10.6084/m9.figshare.23500566.

1. World Cocoa Production

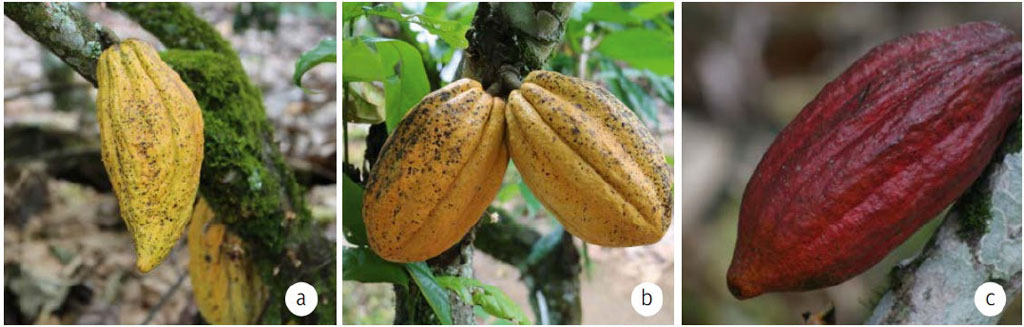

Traditional cocoa classification has only three basic types â Criollo, Forastero, and Trinitario â resulting in different varieties, hybrids, and clones planted worldwide (Figure 1) (see Appendix A).

Types of cacao: (a) Criollo, (b) Forastero, (c) Trinitario. Source: Arvelo et al. (2017).

Citation: International Food and Agribusiness Management Review 26, 5 (2023) ; 10.22434/ifamr-2022-0136r1

The global cocoa market has been characterized over time by its high variability. Nevertheless, cocoa ranks fourth in value traded among tropical crops, behind palm oil, rubber, and bananas. Also, cocoa ranks third in volume, after sugar and coffee, in the world market for agricultural commodities.

Cocoa beans fall into two broad market categories: bulk cocoa, accounting for 90â95% of worldwide production, obtained from the Forastero variety; and fine or flavor cocoa, accounting for 5â10% of global production, obtained from the Criollo and Trinitario varieties. Bulk is a term used in various circumstances, originally meaning cocoa shipped without bags. In the past, bulk cocoa had different names depending on the region. For example, it was known as common cocoa in Europe and as normal, basic, ordinary, or conventional cocoa in other regions. Similarly, the other category was named fine cocoa in Europe and flavor cocoa in the United States.

Cocoa production had grown steadily for 50 years, resulting in a fourfold increase of worldwide cocoa supply. As of 2011, however, an estimated 300 000 MT reduction in production was noted worldwide (Arvelo et al., 2017). This decline lasted until 2016, when production growth rebounded. As a result, cocoa prices declined sharply between September 2016 and February 2017, from $3000 to $1900 (Fountain & Huetz-Adams, 2018). The production growth was mainly linked to the expansion in the planted area in the previous years. This expansion hurt native forests. For example, more than 90% of the original western forests in Africa disappeared to make room for cocoa production.

At the same time, national policies to encourage cocoa production in Latin America and the Caribbean (LAC) also boosted production. In Central America, the land devoted to cocoa production grew by 13% from 2006 to 2014 (Figure 2). Although this figure was below the average world growth of 17%, it allowed countries such as Costa Rica, Nicaragua, Guatemala, and Belize to expand their growing cocoa frontier modestly.

Performance of area harvested in Central American Cocoa-Producing Countries â 2006 and 2013 (in ha). Source: taken from Arvelo et al. (2017) based on 2016 data from FAO (2021).

Citation: International Food and Agribusiness Management Review 26, 5 (2023) ; 10.22434/ifamr-2022-0136r1

Average cocoa bean production in main producing countries. Source: 2016 data from FAO (2021) and ICCO forecast, 2016. Note: 2006 to 2011 and 2012 to 2014.

Citation: International Food and Agribusiness Management Review 26, 5 (2023) ; 10.22434/ifamr-2022-0136r1

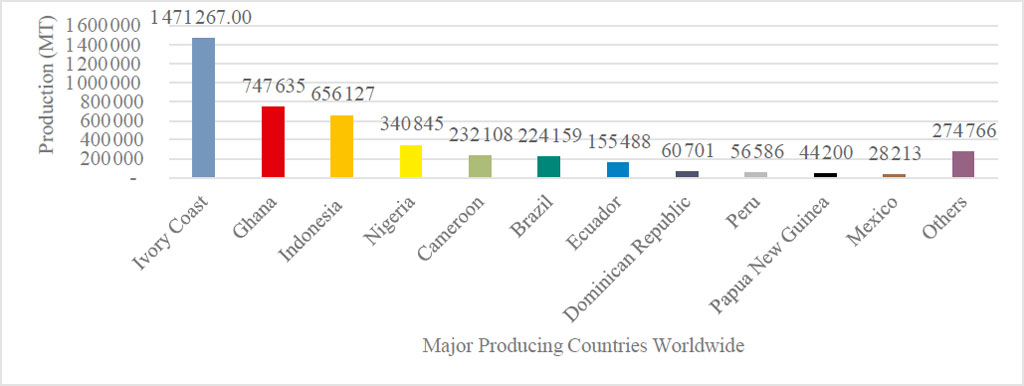

By 2017 world cocoa production exceeded 4 million MT of cocoa beans, with five countries (The Ivory Coast, Ghana, Indonesia, Nigeria, and Cameroon) leading the market with more than 84% of world production (Figure 3).

Africa accounted for 73% of world production and 64% of the worldâs area planted with cocoa. LAC contributed 17% of world production and 17% of the planted area, while Asia and Oceania contributed the remaining 10% of production with 19% of the planted area.

Cocoa cultivation in LAC countries over the last few years had spread remarkably in at least 23 countries, with yields of over 675 000 MT and around 1 700 000 ha planted in 2016. The largest producers included Brazil, Ecuador, Dominican Republic, Peru, Colombia, and Mexico, with more than 90% of the production and area planted on the continent (Arvelo et al., 2017).

Cocoa was estimated to be cultivated by more than 5.5 million producers worldwide, with plots between 0.2 and 0.5 ha. Between 80â90% of cocoa production came from small farmers, for whom cocoa was a significant source of income (Arvelo et al., 2017). Producers in Central America had cocoa plots of less than 2 ha. Average farms in Mexico were around 3 ha. In South America, on the other hand, the average cocoa plot was around 5 ha, except for Brazil, with average plots of around 11 ha (Figure 4).

Average area of cocoa production units in Latin American and Caribbean countries (ha). Source: Arvelo et al. (2017) based on 2016 data from FAO (2021).

Citation: International Food and Agribusiness Management Review 26, 5 (2023) ; 10.22434/ifamr-2022-0136r1

Despite extensive cocoa plantations worldwide, average productivity over the last few years had been around 438 kg/ha. Productivity for major African producers was 432 kg/ha. Asia and Oceania had an average of 505 kg/ha, while LAC had 408 kg/ha. According to SEPSA (2017), there were several causes for low productivity in LAC. The leading cause was the age of cocoa plantations, which in many cases were around 40 years old, which most of the time made them economically unproductive.

Research in Ecuador had made significant advances in genetics. The best-known case was clone CCN-51 (highly productive âbulkâ cocoa), and Nacional Arriba (the new INIAP clones), with production equal to or greater than those of clone CCN-51. Ecuador had also been outstanding in terms of assistance and technical advice to cocoa producers on good agricultural practices, integrated pest control, fertilization, and pruning, among others. All these factors helped Ecuador to increase its productivity considerably (SEPSA, 2017).

Limitations to productivity worldwide were hard to eradicate since most of the production was in the hands of small producers, who could improve almost only with support from governmental entities. However, a few large operations in LAC showed up to 3000 kg/ha yields. This productivity resulted from higher tree density, the use of higher-yield and disease-resistant varieties, better agricultural practices, and proper maintenance of trees, which small producers could not provide.

2. World cocoa trade

Between 1961 and 2014, the world demand for cocoa grew at a compound annual growth rate (CAGR) of 2.7% (Figure 5). This rate was expected to accelerate to 5.2% by 2020 and 7.3% by 2025. Historical growth in global aggregate demand was primarily a function of organic population and GDP growth. The demand had been accelerating in recent years because of the growth of the middle class in China, India, and Brazil. This middle class had enough income to purchase luxury goods, including chocolate confectionery, the main source of cocoa demand.

Apparent domestic cocoa consumption trend worldwide (2007â2015). Source: Arvelo et al. (2017) based on data from ICCO (2016).

Citation: International Food and Agribusiness Management Review 26, 5 (2023) ; 10.22434/ifamr-2022-0136r1

According to Ecuadorâs Ministry of Industries and Productivity, citing Mars and Barry Callebaut, two of the worldâs largest chocolate manufacturers, the gap between cocoa demand and production could grow to 1 million MT by 2020 and 2 million MT by 2030, reflecting the demand trend for cocoa and production concerns due to climate change, a soft focus on sustainability, and social issues in large producing countries.

Between 2007 and 2015 Europe was the largest consumer of cocoa by region, with 47% of the worldâs apparent domestic consumption, followed by the Americas with 32%, Asia and Oceania with 17%, and, finally, Africa with only 4%. Fifty-five percent of world cocoa consumption was concentrated in seven countries. The United States led the list with 20% of consumption, followed by Germany with 9%, France and the United Kingdom with 6% each, Brazil and Russia with 5% each, and Japan with 4% (see Figure 6).

Average Apparent Domestic Cocoa Consumption Of Main Consuming Countries Worldwide; 2007â2015 (MT). Source: Arvelo et al. (2017) based on data from ICCO (2016).

Citation: International Food and Agribusiness Management Review 26, 5 (2023) ; 10.22434/ifamr-2022-0136r1

Europe led the per capita consumption with 2.27 kg in 2015. Countries like Belgium, Switzerland, Germany, France, the United Kingdom, Slovenia, the Netherlands, Poland, and Italy more than doubled the world average of 0.64 kg. America ranked second in terms of per capita consumption with around 1.33 kg. Canada, the United States, Uruguay, Chile, Trinidad and Tobago, Brazil, and Bermuda were countries with levels above 1 kg/year.

World exports of cocoa as an ingredient, 2014â2018. Source: Ulloa Leitón (2019), based on data from FAOSTAT and Trademap.

Citation: International Food and Agribusiness Management Review 26, 5 (2023) ; 10.22434/ifamr-2022-0136r1

Cocoa exports, including cocoa beans, butter, paste, liquor, and powder, were worth $20 billion in 2018 (Figure 7). They had grown steadily at a CAGR of 1.5 from 2001 to 2016 (Arvelo et al., 2017). Cocoa beans accounted for approximately 46% of the export value, followed by cocoa butter with 27%.

Cocoa bean exports per country, 2014â2018 (MT 000s)

Citation: International Food and Agribusiness Management Review 26, 5 (2023) ; 10.22434/ifamr-2022-0136r1

Major cocoa exporters included the Ivory Coast, Ghana, Ecuador, the Netherlands, Cameroon, and Belgium (Table 1). In 2018, 44% of exports came from Africa, 32% from the European Union, 14% from Asia, and 9% from the Americas.

2.1 Bulk cocoa

Bulk cocoa dominated the industry and was traded primarily as a commodity in international exchanges: in New York and London. Fine or flavor cocoa was traded outside international exchanges in transactions negotiated directly between buyers and sellers. Due to cocoaâs unique place in the food value chain and its production characteristics, cocoa prices were largely uncorrelated with major cash crops and the spectrum of most other tropical crops.

The commercialization of bulk cocoa was relatively simple and transparent. Sellers were âprice takersâ according to the prevalent conditions in international exchanges. Buyers were usually large traders and leading chocolate manufacturers (e.g., Mondelez, Mars and Hershey, Nestle, Ferrero Group, and Barry Callebaut, among others) willing to purchase thousands of MT of the fungible commodity.

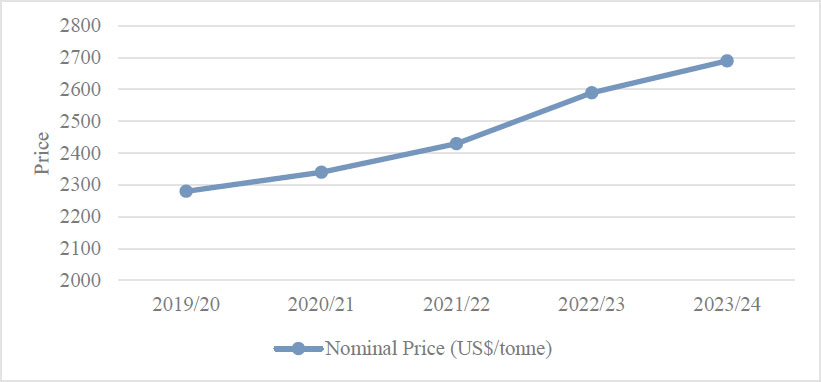

Prices of bulk cocoa averaged close to US$3000 per MT from 2010 to 2016. However, this changed in the 2016â17 season due to an excess supply in the market. The price fell below US$2000 for several months in 2017 and in 2018 was averaging US$2293 per MT (Figure 8). According to ICCO, despite increased supply, prices were expected to continue rising, albeit moderately, from 2019 on due to the continuous increase in demand (Figure 9).

Cocoa price per MT (2010â2018). Source: Authorâs elaboration based on ICCO data.

Citation: International Food and Agribusiness Management Review 26, 5 (2023) ; 10.22434/ifamr-2022-0136r1

Cocoa price projections in US$ per MT. Source: ICCO (2016) data.

Citation: International Food and Agribusiness Management Review 26, 5 (2023) ; 10.22434/ifamr-2022-0136r1

2.2 Fine or flavor cocoa

Fine or flavor cocoa, accounting for around 5â10% of demand, comes from cocoa beans with certain distinctive characteristics, appreciated for their aroma and flavor, which cannot be reproduced using bulk cocoa.

The main difference between fine cocoa and bulk cocoa is in its flavor, not in other characteristics. The flavor of the fine cocoa can include fruity, floral, herbaceous, woody, nutty, or caramel notes. Different varieties of fine cocoa offer idiosyncratic flavors. They are used mainly in the production of a limited number of relatively expensive, up-market chocolates, in which different types of cocoa beans are blended to obtain distinctive flavors and aromas.

There were no unified and clear criteria to determine the classification of fine or flavor cocoa. This made the commercialization of this input more difficult. Evidence indicated that, in addition to genetic components and post-harvest practices, factors such as climate and soil contributed to the difference in the flavor of cocoa beans (Arvelo et al., 2017). Over time, a combination of important criteria had been used. Genetic origin, morphological characteristics of the plants, chemical characteristics, and color of the beans, as well as the degree of fermentation, humidity, and acidity, were among these criteria. Likewise, the presence of undesirable flavors, insect infestation, and the percentage of internal mold and impurities were assessed (Pipitone, 2015).

This type of cocoa tended to produce lower yields than bulk cocoa. But, in many cases, the yield of fine or flavor cocoa was like that of bulk cocoa. For example, Ecuador, the largest producer of fine or flavor cocoa, reported a national yield of around 500 kg per ha in 2018.

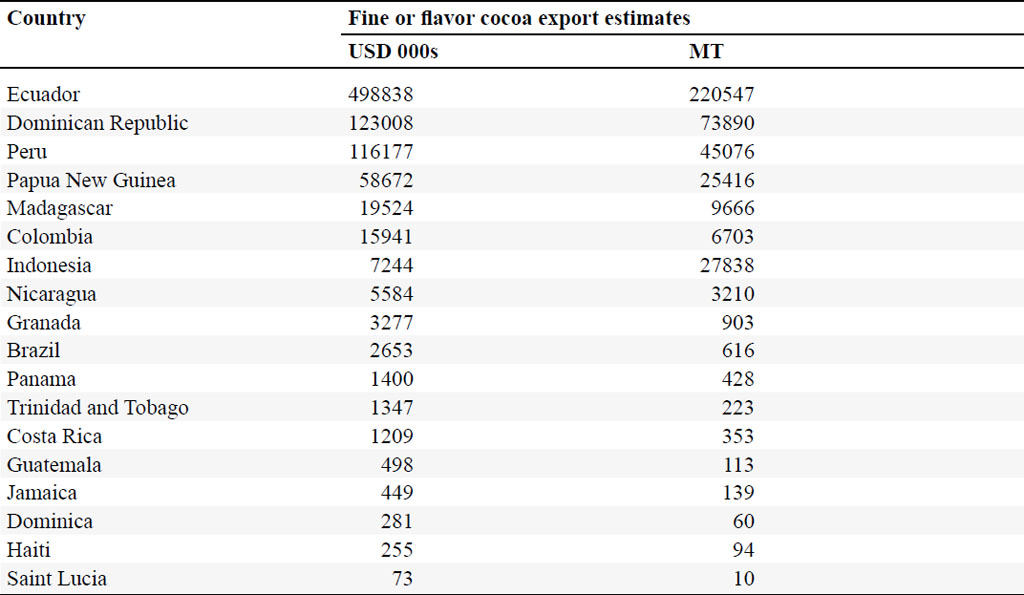

The fine or flavor cocoa market had grown steadily, at a 7â11% rate, since 2011, with estimated exports of more than 300 000 MT in 2017. However, the need for a reliable database in this market made it difficult to verify these numbers (Martin, 2017). Eighty percent of the total production of fine or flavor cocoa came from LAC countries (Pipitone, 2015). Ecuador was the leading exporter of fine or flavor cocoa, accounting for 56% of the global volume exported, followed by the Dominican Republic (19%) and Peru (12%) (see Table 2).

Main countries exporting fine or flavor cocoa, 2018.

Citation: International Food and Agribusiness Management Review 26, 5 (2023) ; 10.22434/ifamr-2022-0136r1

The global demand for up-market chocolate was on the rise. In Europe, the high-quality chocolate market was projected to grow at a CAGR of 8.7% between 2019 and 2024 (ProFound, 2020). The largest importers of fine or flavor cocoa consisted of Western European countries such as Belgium, France, Germany, Italy, Switzerland, and the United Kingdom, in addition to Japan. The United States, on the other hand, consumed mostly bulk cocoa.

Unlike bulk cocoa, fine or flavor cocoa was marketed in an independent, relatively small, and highly specialized market. The transactions were negotiated directly between buyers and producers. The formers were usually specialist agents of particular chocolate companies looking for specific flavors. The average transaction size was relatively small, from a few to 20 MT per contract (a shipping container usually carried 20 MT).

Prices of fine or flavor cocoa in exporting countries, 2010â2018 (USD/MT). Source: Ulloa Leitón (2019), based on ICCO, FAOSTAT, and Trademap data.

Citation: International Food and Agribusiness Management Review 26, 5 (2023) ; 10.22434/ifamr-2022-0136r1

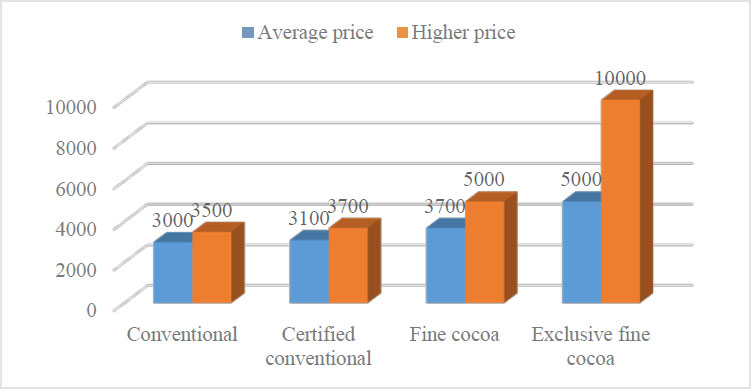

Fine or flavor cocoa normally commanded a price premium over bulk cocoa. Over the last few years, premiums in the Latin American markets for fine or flavor cocoa reached around US$1500 per MT (Figure 10). In 2015, while the price of bulk cocoa oscillated between US$3100 and US$3500, the price of fine or flavor cocoa varied between US$3500 and US$10 000 per MT (SEPSA, 2017). However, producers had to sell their fine or flavor cocoa as bulk input when they did not find buyers willing to pay a premium for their unique flavor. This could be frustrating considering that production was costlier, commercialization more difficult, and yields lower.

2.3 Certified Cocoa

Certified bulk cocoa was seen as part of sustainable, differentiated, and high-quality cocoa goods. The demand for certified bulk cocoa had grown significantly as a response from the chocolate industry to consumersâ growing interest in health issues, origin, and socially and environmentally responsible products.

The over-dependence of large chocolate manufacturers (e.g. Nestlé, Lindt and Hershey, among others) on African cocoa production was a latent threat to them due to three major problems in the region: climate change; social problems such as child labor and slavery; and a lack of orientation towards sustainability. For these reasons, these chocolatiers had set the goal to purchase their cocoa from 100% sustainable sources by 2020. Still, by 2017, none of them was sourcing more than 50% of their purchases from certified suppliers.

The three main certification standards in the industry used to be UTZ, Rainforest Alliance, and FairTrade. In January 2018, UTZ and the Rainforest Alliance merged, keeping the Rainforest Alliance label. All these standards made no difference in the type of cocoa grown (bulk or fine). They provided a differentiation alternative sought by manufacturers, with the following goals: social and organizational well-being; environmental sustainability; good agricultural practices favoring sustainability; and fair commercial practices (Gonzales, 2016).

According to ICCO, only about 15% of cocoa production was certified. However, projections indicated the segment would become 50% of the global demand by 2020. Exports of certified cocoa were estimated to have grown with a CAGR of 37% from 2003 to 2010 and were estimated to continue growing even faster. Latin American countries (Costa Rica, the Dominican Republic, Nicaragua, Peru, Ecuador, Brazil, among others) accounted for 48% of the global production of sustainable cocoa, followed by Africa (Ivory Coast, Ghana, Nigeria), and Asia (India, Indonesia, and Papua New Guinea).

The price of certified cocoa over the last three years exceeded the international price by an average of 4% to 20%. Thus, certified cocoa commanded a price premium between $100 and $1000 per MT. By 2016, certified cocoa prices were between $3100 and $3700 per MT, above those of bulk cocoa but below those of fine or flavor cocoa (see Figure 11). Prices were expected to continue rising due to the global trend for sustainable products.

Certified cocoa prices vs. prices of other segments (2016). Source: Arvelo et al. (2017).

Citation: International Food and Agribusiness Management Review 26, 5 (2023) ; 10.22434/ifamr-2022-0136r1

Most of the certifications did not guarantee a price higher than that of bulk cocoa. This was obtained through direct negotiations between producers and buyers. Thus, bargaining power played an essential role to obtain a good price premium. Small producers sometimes had to sell their certified cocoa beans at bulk prices. The FairTrade certification was the only major standard establishing a minimum price for cocoa ($2000 per MT) and a fixed premium of $200 per MT, offering some protection to small-scale cocoa farmers with weak bargaining power.

3. The Cocoa Industry in Nicaragua

The Nicaraguan government had paid more attention and supported the cocoa sector since 2010. It established a policy for industry development in 2012 and joined ICCO in 2013 to include the country in the list of countries exporting either exclusively or partially fine or flavor cocoa as of 2015.

Nicaraguaâs production volumes were only about 3% of Ecuadorâs, making it almost irrelevant in world cocoa markets. However, innovations in quality and flavor, as well as novel investments in four large-scale plantations in recent years, had placed Nicaragua on the map. As of 2014, Ritter Sport, Bean and Company, and Cacao Oro investments allowed Nicaragua to be seen as a country that would soon produce significant volumes and quality (Wiegel et al., 2020).

In 2018, Nicaragua harvested 11 620 ha, managed by around 11 000 small producers with estimated average yields of 597.2 kg/ha (FAO, 2021) and a production of 6940 MT (Figure 12).

Cocoa production and yield in Nicaragua (2015â2018). Source: Authors, based on FAOSTAT (2019) data.

Citation: International Food and Agribusiness Management Review 26, 5 (2023) ; 10.22434/ifamr-2022-0136r1

Cocoa production in Nicaragua took place in five agroecological regions:

Matagalpa-Jinotega

Región Autónoma de la Costa Caribe Norte (RACCN)

RÃo San Juan

Región Autónoma de la Costa Caribe Sur (RACCS)

Zelaya Central (Nueva Guinea, El Rama and Muelle de los Bueyes)

In these five regions, 98.2% of cocoa production took place, with the rest distributed in other departments, including Rivas, Granada, Boaco, and Chinandega.

The Autonomous Region of the North Caribbean Coast (RACCN) â the most important region among the five listed above â accounted for 38% of cocoa production, followed by Matagalpa-Jinotega with 31.54% (IICA, 2018). The municipalities with the highest production were Waslala, Rancho Grande, and Matiguas.

3.1 Value chain

Most Nicaraguan producers (around 6000) were organized into cooperatives, associations, and solidarity groups, although many producers preferred to remain independent. Producers usually owned smallholdings of 0.7â1.4 ha and grew cocoa under agroforestry systems, with cocoa associated with Musaceae species, fruit trees, and/or timber trees that helped cocoa with shade and families with food.

The producer organizations (around 50) bought cocoa beans in pulp (cocoa beans covered with mucilage, known as âbaba de cacaoâ in Spanish) from their members. They managed their own collection centers, their fermentation and drying infrastructure, and the export contracts with international buyers. A few of the main ones included CACAONICA, La Campesina, RÃos de Agua Viva, and COOPESIUNA, among others. NGOs cooperating with producer organizations also influenced the cocoa value chain.

Most of the cocoa grown in Nicaragua was of the Trinitarian type, with a Criollo genetic base, which gave the country the great potential to produce cocoa with a differentiated flavor and aroma (i.e. fine cocoa). Due to this, Nicaragua was recognized by ICCO as a 100% producer of fine cocoa in 2015. Nicaraguan cocoa trade consisted mainly of exports of cocoa beans, with around 4304 and 4013 MT exported in 2017 and 2018, respectively. Income obtained from said exports was $5.9 and $6.9 million respectively (Figure 13).

US$ Value of Nicaragua Cocoa Imports and Exports (2015â2018). Source: Authors, based on FAOSTAT data.

Citation: International Food and Agribusiness Management Review 26, 5 (2023) ; 10.22434/ifamr-2022-0136r1

Volume of Nicaraguan cocoa exported by destination country (in MT).

Citation: International Food and Agribusiness Management Review 26, 5 (2023) ; 10.22434/ifamr-2022-0136r1

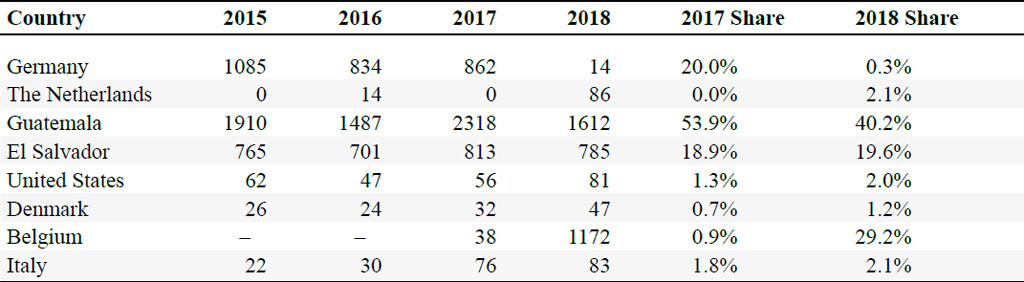

The main export destinations for Nicaraguan cocoa had been the neighboring countries of Guatemala and El Salvador, with 72.7% and 60% of total exports in 2017 and 2018 (Table 3). Other destinations included Germany, the Netherlands, Italy, the United States, Denmark, and Belgium. The latter was a destination with high potential that, in 2018, had grown rapidly to 29.2% of exports in terms of volume, becoming the destination with the highest value (US$3.4 million).

Cocoa exported to El Salvador or Guatemala was grown mainly by small producers. They only washed and dried the cocoa beans (known as âcacao rojoâ; these cocoa beans were washed, barely dried, but not fermented) and sold them to many informal intermediaries (known as âcoyotesâ). These intermediaries specialized in domestic commercialization and in exporting to neighboring countries. There was significant smuggling to these destinations. Most of the cocoa exported to El Salvador and Guatemala was underdeclared; that is, the real value of cocoa exports was much higher than reported and the real destination was unknown (industry participants thought that the main destination was Mexico). For that reason, even though large quantities of cocoa were exported to those countries, their monetary value was lower than that of cocoa exported to Germany or Belgium.

A second significant flow of cocoa was of the certified fermented type, exported to European countries by subsidiaries of international chocolate manufacturers (around 4) such as Ritter Sport, which owned farm operations or bought cocoa from producer organizations. These exporters produced or purchase large volumes of certified cocoa beans that had been washed, fermented, and dried under strict quality standards. Finally, fine or flavor cocoa was commercialized by both cooperatives and independent producers, who could sell it locally to a few specialized exporters such as Ingemann, or directly to fine chocolate manufacturers in Europe. This latter segment was receiving increasing attention, given the international recognition granted to the country in recent years.

Cocoa cultivation in Nicaragua certainly had significant potential to become a major source of income for producers and of development for rural communities. Despite this, some issues had to be resolved. A major weakness of cocoa programs was a discontinuity in the support for producers until they were linked to the market (Carrillo, 2019). Other limitations included producersâ limited crop management knowledge and low-investment capacity to create new plantations. Nicaragua had limited cocoa fermentation and drying infrastructure, which restricted the industry potential. Another issue was obtaining verifiable genetic material that would result in greater long-term productivity. The Instituto Nicaragüense de TecnologÃa Agropecuaria (INTA) was the leading supplier of this material in 2018.

Crop profitability had been a deterrent for the sector. Evidence suggested that cocoa growing was not profitable for the average producer. As a result, many cocoa growers prioritized other crops grown together with cocoa. The poor performance was mainly due to the lack of inputs, lack of experience with cultivation, poor agricultural practices, and the unwillingness of producers to specialize in this crop, opting for more common activities such as livestock.

The cocoa industry in Nicaragua was emergent, marketing cocoa beans mainly as a commodity, while transformation into intermediate or final products was just in the infant stages. However, the tradition of consuming cocoa and its by-products and increasing international recognition as an origin of high-quality cocoa contributed to energizing the national value chain.

By late 2018 Nicaragua was undergoing a sociopolitical crisis. Despite this, cocoa was one of the few crops with expected growth in 2019. The country was expected to produce about 7200 MT of cocoa on 11 100 ha, with productivity levels well above the world average, due to the increased yields from new plantations. As a result, export revenues were expected to reach US$9.3 million, US$2 million above those in 2018. Likewise, the leading exportersâ organization estimated that Nicaragua would produce 25 475 MT of cocoa and revenues of US$40.7 million by 2026 (APEN, 2019).

4. Cacao Oro de Nicaragua: the company

Cacao Oro de Nicaragua was founded in 2014 to produce cocoa on large-scale, sustainable plantations in Nicaragua and Peru. Since its onset, the company aimed to work with rural communities of the Atlantic of Nicaragua to grow cocoa as a profitable crop. In addition, it planned to expand to Peru to reach a total production area of about 10 000 ha. Finally, the company refocused its development efforts solely on Nicaragua to develop 10 000 ha of cocoa in the Autonomous Region of the North Caribbean Coast (Figure 14).

Map of Nicaragua and location of Cacao Oro. Source: Authors.

Citation: International Food and Agribusiness Management Review 26, 5 (2023) ; 10.22434/ifamr-2022-0136r1

From its start, Cacao Oro was a source of development for the region in an impoverished area in the northeastern region of Nicaragua. It was the leading employer in the area, with the positive impact of improving the lives of its workers and their families. In addition, it contributed to building bridges, roads, irrigation canals, and general infrastructure for the community and the company.

Cacao Oroâs top management team included John Warrington, Clément Ponçon, and Gifford (Giff) Laube. John, an investor who became the CEO, had studied the industry extensively and formulated the business plan for Cacao Oro. Clément, also an investor who became the Vice-President of Operations, had more than 45 years of experience in large-scale agricultural projects in Nicaragua and 18 other countries in Latin America. John and Clément led the efforts to raise enough capital from several investors to fund the venture. Giff, who became the Operations Manager, was responsible for selecting cocoa varieties, the technical nursery, field operations, and logistics.

The company had established strategic alliances with Exportadora Atlantic, an exporter of approximately half of Nicaraguaâs coffee production at that time, and Ecom Agroindustrial (parent company of Exportadora Atlantic), a global trader of agricultural commodities and logistics, with a presence in more than 40 countries.

The plantation was in a 3000-ha area that Hurricane Felix had damaged in 2008. The farm âLa Rositaâ was planted, reforested, and managed following sustainability criteria. The restoration of La Rosita resulted in 2000 ha of effective area for cocoa production. The business plan proposed that the farm would become the largest private cocoa plantation worldwide, with more than two million cocoa trees in 2000 ha, more than 200 000 broadleaf trees, and a 1.5-ha permanent-shade nursery able to produce 1.5 million plants per year. The plan was to reap the optimal economies of scale from a large plantation, implement best practices to boost productivity and invest in the best technology from farm to export to assure quality consistency throughout the process. The first harvest of several MT of cocoa occurred in 2017.

Cacao Oroâs farm was in the process of being certified under independent, internationally recognized sustainability standards, including UTZ and Rainforest Alliance. The operations followed an agroforestry model, including active reforestation of degraded lands with native species such as cedar, mahogany, and ânanciton.â More than 200 000 hardwood trees had been planted, interspersed with cocoa plants and other crops, which improved soil nutrition and helped care for flora and fauna in the region.

From the projectâs beginning, Cacao Oro had nineteen different cocoa varieties under study: CCN-51, known worldwide for its productivity but low quality, CATIE R-1, CATIE R-4, CATIE R-6, CC-137, ICS-39, PMCT-58, ICS-95, IMC-67, UF-296, UF-613, UF-667 and UF-668, which were international clones; and six Costa Rica Selecto varieties, categorized as fine or flavor cocoa. These varieties stood out for their organoleptic features, their resistance to disease, and their bean size, which was reflected in their weight (above 1 g).

With these varieties, Cacao Oroâs initial plan was to develop three different production areas: 600 ha for the CCN-51 variety, 700 ha for international clones, and 700 ha for the fine or flavor cocoa variety. The former had the highest yield per hectare, while the clone and fine or flavor cocoa areas had slightly lower productivity. Investment and production costs such as labor, harvesting, fertilization, pruning, pest management, and so on were almost the same for all areas. The only difference was post-harvest processing, during which the CCN-51 variety had to be handled separately due to its different drying and fermentation times.

Cacao Oro had invested in the infrastructure, technology, and equipment for a vertically integrated operation. As a result, it had a permanent-shade nursery, an industrial fermentation center, mechanical dryers, and automated classification and packaging equipment, with the capacity to process all the companyâs production, assuring product quality.

4.1 Competitive advantages

Production volume

Production volume was a significant difference and advantage of Cacao Oro. Nicaraguan and world cocoa production was dominated by small producers who could hardly provide large volumes of consistent quality to chocolatiers. As a result, Cacao Oro could distinguish itself from 99% of the worldâs producers.

High yield

This was a critical factor in profitability. Cacao Oroâs initial production confirmed yield estimates from 1500 to 2000 kg/ha, a figure that has yet to be achieved by Nicaraguan producers.

Availability of capital

Small producers need more capital to implement best practices, train staff, acquire adequate technology, etc. Cacao Oro enjoyed a significant degree of capitalization, resulting in high tree density, intensive maintenance and control, better cocoa varieties, and better technologies, vertical integration from farm to export, among other factors.

Low production costs

Cacao Oro projected production costs between $800 and $1000 per MT processed (i.e. produced, fermented, dried, and packaged). Considering historical market prices, Cacao Oro faced very low risks.

Vertical integration

Unlike Nicaraguan producers, Cacao Oroâs permanent-shade nursery and in-farm fermentation and drying capacity were designed to increase margins, control product quality, and eliminate the risks of dependence on local suppliers. Average-quality beans could produce high-quality chocolate if handled, fermented, and dried carefully. However, exceptional-quality beans could result in poor chocolate if not processed appropriately.

There were few large-scale cocoa producers with the experience, bargaining power, and resources that Cacao Oro was deploying. This gave the company a unique opportunity to become the largest producer in Nicaragua, Latin America, and, eventually, the world.

5. The Decision

In a decisive time for Cacao Oroâs future, John Warrington wondered about the best competitive strategy for the companyâs expansion. The investors were delighted with the ventureâs evolution in the last three years. However, they wanted to continue pursuing their vision of becoming the largest producer in the world. John identified four market options: first, to focus on bulk cocoa, with commodity prices and high-volume transactions; second, to specialize in fine or flavor cocoa, with high price premiums and low-volume transactions; third, to focus on certified bulk cocoa, with small price premiums and high-volume transactions; and, finally, to develop a âmixedâ strategy with a combination of the three previous options.

Cacao Oro could serve as a source of development for the Atlantic region of Nicaragua, as it had a clear focus on its social impact and production and processing capabilities. First, however, the firm was waiting for proper recommendations on a clear competitive strategy for the expansion in the next few years. In addition, John knew that each market option also involved a particular set of strategic choices to compete and win in each field. Thus, Johnâs recommendations had to define all these strategic choices in detail.

Bulk cocoa was a business relatively easy to develop but faced challenges related to price levels and instability according to supply fluctuations. Fine or flavor cocoa offered the highest prices but entailed challenges for large-scale operations, more significant transaction costs, lower yields, and high variation in buyersâ preferences. Certified bulk could take advantage of a rapidly increasing demand willing to pay small price premiums but faced the risk of âcommoditizationâ in the future. Moreover, a âmixedâ strategy would provide risk diversification and the capability to cater to different buyer segments but could complicate the operation significantly.

References

APEN, 2019. Cacao nicaragüense sortea crisis y apunta al crecimiento. Available online at https://apen.org.ni/cacao-nicaraguense-sortea-crisis-apunta-al-crecimiento/

Arvelo Sánchez, M.A., D. González León, T. Delgado López, S. Maroto Arce and P. Montoya RodrÃguez. 2017. Estado actual sobre la producción, el comercio y cultivo del cacao en América (No. IICA 633.743 E79). IICA, San José; Colegio de Postgraduados, México City; Fundación Colpos, México City.

Bejarano, M. 2019. Nicaragua vende menos cacao en 2018 y desaprovecha aumento de precio. Available online at https://www.elnuevodiario.com.ni/economia/483459-nicaragua-vende-menos-cacao-2018-desaprovecha-aume/

Carrillo, N. 2019. La Cadena de Valor del Cacao en América Latina y El Caribe: Diagnóstico de la Cadena de Valor del Cacao en Nicaragua. Available online at https://www.fontagro.org/new/uploads/adjuntos/Informe_CACAO_linea_base.pdf

Dirección de Estudios Económicos e Información Agraria de Perú. 2019. Repositorio Institucional MIDAGRI. Available online at https://repositorio.midagri.gob.pe/

FAO. 2021. Cultivos y productos de ganaderÃa. FAO-STAT. Available online at http://www.fao.org/faostat/es/#data/QCL

FAOSTAT.2019. Metadata. Available online at https://www.fao.org/faostat/es/#data

Fountain, A and F. Huetz-Adams. 2018. Barómetro del Cacao 2018. Available online at https://www.voicenetwork.eu/wp-content/uploads/2019/08/Cacao-Barometer2018_PMS_ESP_v2.pdf

Gonzáles, D. 2016. La calidad del cacao. IICA, San José.

ICCO. 2016. Forecast. Available online at https://www.icco.org/statistics/

IICA. 2018. IICA, culmina proceso de preparación del documento orientador para el financiamiento y gestión de inversiones en la cadena de cacao en Nicaragua. Available online at https://iica.int/pt/node/16508

Martin, C., 2019. Sizing the craft chocolate market. Fine Cacao and Chocolate Institute, Cambridge, MA.

Pipitone, L., 2015. Nuevas tendencias en el mercado internacional de cacao: oportunidades para el Peru como productor de fine or flavor cocoa (presentation). ICCO, Lima.

ProFound, 2020. The European market potential for specialty cocoa. Centre for the Promotion of Imports from developing countries (CBI), The Hague. Available online at https://www.cbi.eu/market-information/cocoa-cocoa-products/speciality-cocoa/market-potential

Ulloa Leitón, E. 2019. Caracterización de la comercialización internacional del cacao como ingrediente en las industrias cosméticas y alimentaria. Available online at http://sistemas.procomer.go.cr/DocsSEM/5A52A4C7-2FAF-4D5B-9940-9F36381AEC3B.pdf

Voore, V., S. Bermúdez and C. Larrea. 2019. Global Market Report: Cocoa. International Institute for Sustainable Development (IISD). Available online at https://www.iisd.org/system/files/publications/ssi-global-market-report-cocoa.pdf

Wiegel, J., M.D. Rio, J.F. Gutiérrez, L. Claros, D. Sánchez, L. Gómez, C. Gonzalez and B.A. Reyes. 2020. Sistemas de mercado de café y cacao en las Américas: oportunidades para apoyar la renovación y la rehabilitación. Centro Internacional de Agricultura Tropical (CIAT). Cali.

Appendix A A Historic Crop

Cocoa (Theobroma cacao) belongs to the genus Theobroma and the Malvaceae family, with more than 22 known species. Originally from South America, it was later domesticated in Middle America. Its scientific name comes from the Greek theos (god) and broma (food), a name that reflects its importance to Native Americans.

Cocoa requires adequate temperature, humidity, and rainfall to produce acceptable yields and to reduce its susceptibility to pests and diseases. Cocoa trees grow close to 30 feet tall in the wild but only seven to nine feet when planted for farming. The trees have straight, smooth trunks, with oval, bright red and green leaves, depending on age, and small yellowish flowers that turn into fruits. The fruit consists of an elongated berry containing around 20 to 40 seeds.

Cocoa pods were first used by the Mayans around 600 AD in Mexico for a drink served exclusively to warriors and nobles. The Mayans valued cocoa more than gold and, thus, used it for barter. Mayan mythology held that cocoa was a gift to humans from Kukulkan, the feathered serpent deity, and they honored the cocoa god with offerings and sacrifices. Aztecs, on the other hand, adapted the mythology and maintained that Quetzalcóatl descended from heaven to bring cocoa as a gift to humans. As a result, cocoa was used not only for currency but also for veneration.

Regardless of its origin, cocoaâs economic and cultural contribution to society cannot be denied. Currently, it is a significant crop in different regions around the world.

Corresponding author

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}