Abstract

Do low levels of social trust increase a population’s sense of insecurity and desire to get an insurance policy or alternatively make it turn to informal networks for safety nets? While generalized social trust is an important variable to explain insurance uptake, the existing literature offers conflicting accounts of its impact on a population’s insurance demand. By employing a mixed-methods research design that combines multivariate regression of large-N cross-country data with a qualitative case study of Azerbaijan, the study provides a systematic analytical measurement of the impact of social trust on the voluntary purchase of health insurance in 93 emerging markets. The article finds a statistically significant positive effect of generalized trust on voluntary health insurance purchases. The findings suggest that in countries with a low level of social trust, people favor informal safety nets rather than formal contracts with insurance firms.

1 Introduction

As any other business operating on market principles of demand and supply, the insurance industry assumes that a customer is a proactive instrumental utility maximizer. Hence, the industry’s business model presupposes that customers mostly procure insurance voluntarily,1 according to their individual cost-benefit calculations. However, data from Latin America (MAPFRE 2018), ASEAN (Schanz, Alms & Company 2018a), sub-Saharan Africa (Schanz, Alms & Company 2018b), South and East Asia (Willis Towers Watson 2018; Crawford 2018, 10), and MENA (Schanz, Alms & Company 2018c, 41) shows that the key drivers of insurance industry growth are mandatory insurance types (Crawford 2018, 10).

What socio-economic factors may possibly explain the skeptical attitudes of emerging market populations towards voluntary insurance products? A range of studies provide alternative explanations (see, Shi, et al 2015, Cole et al. 2011, Dragos 2011, Elango & Jones 2011). Among these factors, one variable – the impact of generalized social trust2 – seems puzzling. Generally, the literature acknowledges this variable as important in shaping insurance procurement preferences among the population (Shi et al 2015, Borisova 2017), as well as serving as a major factor influencing an individual’s insurance uptake (Pye 2005). On the other hand, there is a dearth of empirical studies of large-N cross-country data on the matter. Additionally, most emerging market studies focus on trust in insurance companies (as a predictor of voluntary insurance procurement) (World Bank 2011, Ernst &Young 2014, Borisova 2017, Prokopyeva 2015). Swiss Re argues that in emerging markets “affordability is a major demand-side barrier, but … even subsidies do not lead to improved take-up of insurance … because of lack of trust in the industry” (Swiss Re 2017, 1). However, the impact of a broader concept – i.e. social trust – is not equally well scrutinized.

This gap in research incapacitates both governments’ and insurance industry actors’ ability to account for a major factor shaping demand for insurance products. A population’s generalized trust is fundamental for retaining insurance users and increasing social safety and well-being in emerging markets. Without understanding a population’s reaction to insurance uptake as a function of social trust, we are unlikely to grasp the increasing penetration of insurance schemes in the developing world. Hence, both the regulatory authorities and insurance companies have to work actively to understand the potential impacts of social trust on the population’s insurance demand.

Consequently, this article provides a systematic analytical measurement of the impact of social trust on the insurance uptake of emerging market populations. Building on existing literature on insurance demand, and by employing data on 93 emerging markets, I argue that the level of generalized trust in society is a potent factor positively associated with a population’s preferences for voluntary health insurance procurement. Along with corroborating the importance of personal (freedom to affect one’s life), industry-specific (insurance penetration, Soviet legacy), and socio-economic factors (urbanization, education, GDP per capita), the research also finds that the levels of corruption perception, the shadow economy, natural resource dependence, and insurance industry concentration are not statistically significant in predicting the level of population’s voluntary health insurance purchase in emerging markets.

This article makes several contributions to the scholarship on trust and insurance policy. This is the first systematic empirical assessment of the impact of the social trust environment on the level of voluntary insurance purchases encompassing 93 emerging markets, hence providing the most comprehensive analysis, given existing data. On the other hand, it contributes to the academic literature on the effects of generalized social trust in the developing world context. There are also research implications for the rule of law (corruption, the shadow economy), and resource-dependence literature. Second, unlike similar studies of population attitudes and practices of insurance procurement, this study complements quantitative cross-country statistical analysis with qualitative data from a focus group discussion with actual insurance users in one of the emerging economies. Additionally, while social trust is a structural-environmental factor, government policies can mediate its impact on voluntary insurance purchase. Hence, the article contributes to public policies regulating the insurance industry, by highlighting specific mechanisms through which generalized social trust translates into a consumer’s specific perception, and then a decision to react to an insurance product.

I start by outlining alternative theories explaining the impact of different variables on voluntary insurance purchase. The following section discusses the research hypothesis. Then I move to the methods section, including variables and data. The next section outlines the results of the quantitative analysis. Subsequently, I discuss qualitative analysis findings and place them into a broader social context. The final section concludes by discussing research implications.

2 Theories Explaining Population Insurance Purchase

Before the examination of major explanations shaping the variation of a population’s insurance demand, we conceptualize generalized trust. “Generalized trust” refers to trust in other members of society. It may be distinguished from the particularized trust, which corresponds to trust in the family, neighbors, or close friends. Generalized trust is measured by the percentage of a country’s population who affirmatively answer the statement “Most people can be trusted”. In the context of insurance purchases, individuals with higher levels of generalized trust are more likely to believe that insurance companies and other actors involved in the insurance industry will act in good faith and fulfill their obligations. People with high levels of generalized trust tend to believe that others will act in a trustworthy manner, even if they have no personal relationship with them. This is different from particularized trust, which is based on personal relationships and experiences with specific individuals or groups. Generalized trust is based on a more abstract belief in the overall honesty and reliability of others in society.

The effect of generalized trust on insurance purchases is complex and can vary. On the one hand, individuals with higher levels of generalized trust may be more likely to purchase insurance because they believe that insurance providers will act in good faith and provide fair compensation in the event of a loss. On the other hand, individuals with higher levels of generalized trust may also be less likely to purchase insurance because they believe that other members of society will be willing to help them in the event of a loss, reducing their need for insurance.

Economic and sociological literature provides several major explanations for the variation of a population’s insurance demand. The first set of explanations underlines the importance of modernization, with concomitant rising levels of urbanization, education, income, and other personal determinants on insurance demand (Dragos 2014, Alhassan and Biekpe 2016). According to Zelizer (1978), a dominant mode of collective attitudes toward human life, specifically the sacralization of human body, death, and life, historically prevented an active penetration of life insurance among Americans. Since the human body and death were sacral concepts, selling and purchasing them, and assigning a monetary value to them in a life insurance policy was deemed blasphemous. However, with modernization that led to urbanization after the American Civil War, the situation changed. Urbanization meant that orphans and widows could not rely anymore on the assistance of their extended family, but depended solely on the wage of a male breadwinner. Hence, in the case of the latter’s death in an urban setting, families and society, in general, had little choice but to accept life insurance as a religiously meritorious act of “active beneficence” which guarantees deceased policy-holders an easy afterlife (Zelizer 1978, 605). Thus, modernization (with concomitant urbanization) gradually led to a change in religious attitudes and superstitions related to life insurance purchase.

Shi et al (2015), Hess, Leuenberger, and Scherrer (1996) argue for a positive association between the amount of per capita income, as well as perseverance and thrift (Park & Lemaire 2011), and the level of insurance penetration.3 As a result, some researchers believe that growing economic welfare will gradually increase the rates of insurance penetration in emerging markets (Faulkner 2002). This perspective generally argues that increasing incomes make insurance affordable and more attractive. Education (Kjosevski 2012) is tightly connected with both urbanization and rising GDP (Dragos 2014, Alhassan and Biekpe 2016) in determining insurance demand. Linked to the broader ‘modernization’ paradigm, these factors boost a social taste for the instrumental application of a utilitarian rational choice, hence leading to a higher probability of insurance purchase.

Among other factors, an emerging economy’s rentier state environment can negatively affect insurance culture by undermining economic effectiveness (Mahdavy 1970, Ross 2012), and accountability. In such societies, insurance companies and individuals living off natural rent, subsidies, or state handouts do not have market incentives to embrace an effective customer-oriented approach. Individuals rely on the government to mitigate the negative repercussions of risks, otherwise transferred on insurance companies. Such a rentier social environment leads economic actors to treat insurance premiums as a ready resource for expropriation and consumption, rather than financial capital growth based on the instrumental application of a probability theory.

Among other modernization-related factors shaping a country’s ‘insurance culture’ is the levels of fatalism or freedom to affect one’s life choices (Black and Skipper 2000) related to fatalism dominant in a given society. Yusuf, Gbadamosi, and Hamadu (2009, 37) argue that “reliance on life insurance results from a distrust of God’s protecting care.” Hence a social setting with a lower level of fatalism is predicted to increase motivation for purchasing insurance voluntarily.

A second group of explanations points to the importance of industry-specific dynamics on a population’s insurance demand. Insurance penetration and insurance density are two major measures of a given insurance market’s development level (Swiss Re 2017, Ernst &Young 2014). Higher insurance market development leads to greater versatility and quality of services, hence driving the population into the insurance market. Monopolization or concentration levels of the insurance industry belong to these explanations (Pye 2005, 208; Aliyeva 2011, 9). Lower concentration usually leads to higher market competition, which in turn translates into greater care for customer feedback, lower prices, higher quality, and a greater range of insurance products. Consequently, a higher concentration has the opposite effect, including weak insurer outreach to customers for feedback (Naujoks et al 2016), and the resulting limited population awareness about specifics of insurance policies and terms (Borisova 2017). For instance, while during the communist period in Central and Eastern Europe (CEE) and the former Soviet Union, the state was the sole provider of insurance, this legacy was carried over to the post-communist period in such countries as Russia, Kazakhstan, Belarus, where the markets are dominated by state-owned insurance corporations (Rosgosstrakh, EIC, and Belgosstrakh respectively).4

Other industry-specific variables are economic growth and investment climate. Hence economic crises are predicted to have a negative association with the level of insurance pervasiveness in a given country (Park, Borde, Choi 2002). High rates of inflation make it both difficult (Greene 1954) and unprofitable (Ahlgrim & D’Arcy 2012) for insurers to invest in and have satisfactory profit margins on the market. Since insurance serves (along with banking and capital markets) as a major pillar of any financial system, it is very sensitive to the health of banks (Chen, et al 2014). Without flexible and broad investment opportunities offered by banking and capital markets, insurers face obstacles to capitalize on their funds.

The third strand of theories focuses on informality (with the effect of social capital), and the rule of law (including corruption, and the shadow economy) as defining factors of population insurance demand. Trust and generally social capital are mentioned as important factors of insurance demand (Shi et al 2015, Camargo and Gonçalves 2014, Jowett 2002). Informality and the shadow economy (Polese et al 2014, Mobarak and Rosenzweig 2012) shape ‘insurance culture’ and social welfare in a given society (RNSF 2017). The presence of a considerable shadow economy not only opens up opportunities to neglect formal demands and norms of insurance legislation (Williams & Nadin 2012) but also undermines trust in formal contractual relations – people do not treat insurance contracts and obligations as being backed by an effective enforcement mechanism. Hence, it is not surprising that ‘predictability’ is singled out as one of the three most important factors affecting insurance culture (Hofstede 1995).

An important factor, related to informality, is the rule of law in a given society. According to the range of studies, law enforcement heavily affects the dynamics of medical insurance (Jain, et al 2014), life insurance penetration and density (Kjosevski 2012), as well as the overall insurance industry (Koblensky 2017). Hofstede (1995) points to social solidarity as an important value affecting insurance culture. Distrust in formal laws and high corruption diminish citizen trust in insurance contract terms. If, for instance, an agent asks a kickback for releasing customer insurance claim payment, then the customer is likely to rely on personal savings and/or her personal network to deal with the next emergency instead of seeking formal insurance coverage. However, Kjosevski (2012) notes that although the rule of law is important for life insurance demand, the control of corruption is not a significant predictor of it.

3 Hypothesis: the Effect of Generalized Social Trust

While extant literature postulates a significant effect of generalized social trust on a population’s insurance uptake, including health insurance, there is no consensus on the direction of its effect. Indeed, a higher generalized trust may affect a population’s insurance purchase both positively and negatively. Some research (Murgai, et al 2002) postulates that social trust is negatively associated with population insurance uptake – i.e., the lower social trust, the higher the probability of insurance purchase; and vice versa, a higher social trust leads to a greater reliance on informal (kinship and neighborhood) rather than formal (like insurance) channels to cope with possible emergencies. As an actor finds itself in an environment with low generalized trust, it strives to shield itself from vicissitudes by relying on formal means of securing insurance, because informal channels are untrustworthy.

On the contrary, higher generalized trust increases the probability of informal insurance schemes. For instance, agricultural communities pooling resources together in insurance schemes to shield from possible negative weather effects should weigh the positive returns of such insurance against the backdrop of “transaction costs of monitoring behavior, enforcing participation, and coordinating transfers” (Murgai, et al 2002, 246). In this situation, higher generalized trust decreases risks of transaction costs, and thus ensures the maximization of the positive yield of the insurance scheme. As a result, higher generalized trust leads to a higher probability of entering into informal insurance setups.

Other research, on the contrary, postulates a positive relationship between social trust and formal insurance uptake. This strand of research argues that a higher social trust leads to a greater probability of insurance purchase, thanks to several factors. First, a higher social trust environment increases the chances that actors will replicate the decisions of other agents who have already purchased insurance. Cai et al (2015) show that trust “networks do effectively transfer information about the functions and benefits of insurance” (p. 82) leading to higher insurance take-up rates. Thus, trust contributes to social learning and experience exchange which in turn leads to higher formal insurance adoption.

Second, a higher social trust increases the chance of collective absorption of “aggregate shocks that affect a whole community” (Dercon 2015, 132–3). Since some members of the community are more exposed to basic risk than others, social trust increases the probability that other individuals will “commit to offer mutual protection to each other against such idiosyncratic shocks” (Dercon 2015, 133). This in turn increases the willingness of the agents to procure insurance. As a result, greater social trust leads to a greater willingness to share knowledge and risks, thereby contributing to a higher insurance adoption.

Indeed, does an individual’s worry about their social surroundings lead to a higher preoccupation with personal insurance? Or is it significant trust in a social environment that makes people in emerging markets trust their resources to long-term insurance schemes?

While the literature is inconclusive, I test the following hypothesis of the effect of generalized social trust:

Hypothesis: Higher generalized social trust in a given society increases the probability of its population’s voluntary health insurance uptake.

4 Methodology

To test the proposed hypothesis, I use a mixed-methods research design. I start with multivariable OLS regression of cross-country large-N data compiled from open sources. Then I specify the model and proceed to measure the direction and impact of generalized social trust on population health insurance purchases in 93 countries. I follow up with the discussion of qualitative data drawn from three focus group discussions held in Azerbaijan.

4.1 Quantitative Method

4.1.1 Variables and Model Specification

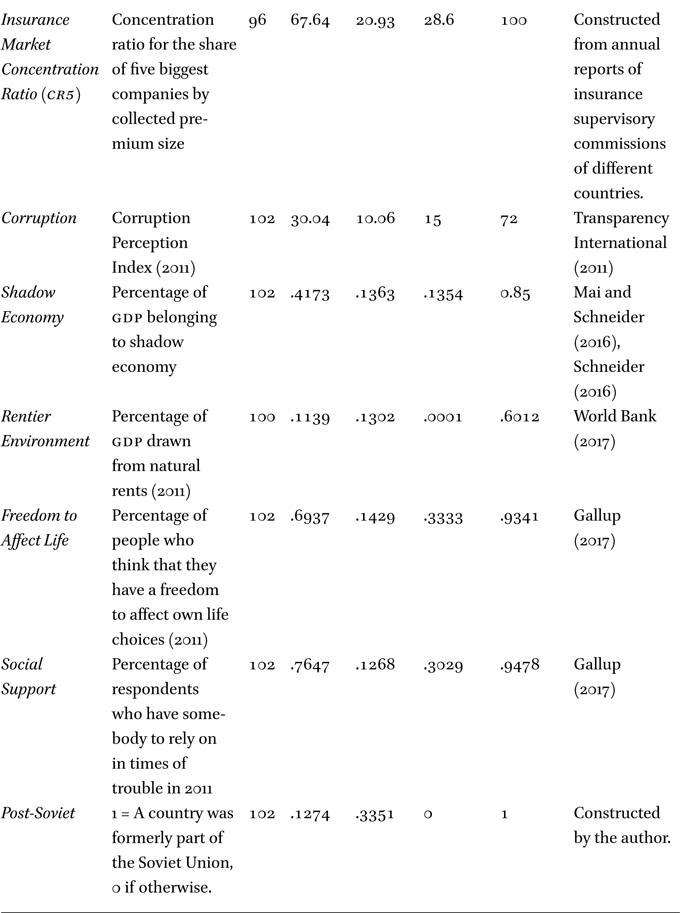

Table 1 reflects descriptive statistics of the quantitative analysis variables. In terms of the outcome variable, no significant cross-country surveys measure voluntary insurance purchases per se. Insurance regulators of different countries publish annual insurance market reports on the share of voluntary vs. mandatory insurance premiums. However, “voluntary” insurance segments in these reports provide an incomplete picture of population insurance demand. For instance, these reports put different private and public employers’ procurement of insurance for their staff into the voluntary insurance segment, while in reality the population/employees do not purchase this insurance out of personal volition. To overcome this imprecision, I use as an outcome variable “personal purchase of health insurance” – a measurement of the World Bank’s (WB) Global Financial Inclusion survey (2011). While the measurement pertains only to the purchase of health insurance (on top of national health insurance), it is the only available valid indicator of a voluntary insurance procurement. Hence, the dependent variable is Personal Purchase of Health Insurance measured as a percentage of country respondents who had personally purchased health insurance from a total sample of respondents in each country. Since the variable data is available only for 2011, the measures for all other variables are also provided for the year 2011. Consequently, the dataset is a cross-sectional one. The independent variable is Generalized Social Trust measured as a percentage of country respondents agreeing with the statement that “Most people can be trusted” in 2010–2011 by Gallup World Poll.

To account for the effect of modernization-related variables, I include into the statistical model Urbanization (measured as a percentage of urban people in a country’s total population) (World Bank 2017), Education (calculated as the latest available number of new entrants in the last grade of lower secondary education, divided by the population at the entrance age for the last grade of lower secondary education) (UNESCO 2017), and GDP per capita (based on purchasing power parity in constant 2011 international dollars) (World Bank 2017). Rentier Environment in a country is measured by the percentage of GDP drawn from total natural rents, defined as “the sum of oil rents, natural gas rents, coal rents (hard and soft), mineral rents, and forest rents” (World Bank 2017). Freedom to Affect Life (or anti-fatalism) in a given social context is drawn from the Gallup World Poll and measures the percentage of people who think that they have the freedom to affect their life choices (Helliwell, Layard, and Sachs 2018).

Second, industry-specific variables are accounted for in the following way: the level of monopolism in insurance is operationalized by Industry Concentration ratio, measured as the ratio of the combined market shares of the five biggest firms to the whole market size of a given country (CR5). The variable was constructed based on the following sources: 1. relevant figures published by national agencies regulating the insurance industry; 2. international business reports (including the reports of Africa Re (2019), and Atlas Magazine (2016)). Insurance Penetration is a variable denoting the maturity of a country’s domestic insurance sector and is measured as the ratio of underwritten insurance premiums to a country’s GDP. The variable was constructed based on the following sources: 1. relevant figures published by national agencies regulating the insurance industry; 2. International business reports (including the reports of MAPFRE (2015), OECD (2020), PwC (2018), Africa Re (2020), and AIG (2013)).

Since post-Soviet countries have a communist legacy of pure market monopolism, I also include a dummy variable for the Post-Soviet region (variable = 1 if a country is a post-Soviet state, 0 = otherwise). Economic growth is a dynamic process that assumes economic efficiency over a multi-year horizon. Therefore, I measure the variable with Growth rate, the rate of GDP growth for 2011. Third, to account for informality-related variables, I use Corruption (drawn from Transparency International’s Corruption Perception Index (CPI)), and Shadow Economy (measured as the percentage of the shadow economy in the volume of a country’s GDP), both variables reflecting the situation in the year 2011. To provide an additional check for the pressure of the social environment on population insurance demand, I use Social Support denoting the presence of someone on whom a respondent can rely in case of an emergency (Gallup 2017).

4.1.2 Model Specification

Pearson correlation coefficients of independent variables show only one salient correlation (> 0.60) (Table 2): per capita GDP is saliently correlated with Urbanization (0.71), as is suggested by modernization theories (Kendall, Linden, and Murray 2007, 11). Collinearity diagnostics show no significant Variance Inflation Factors (VIF) values (Table 3). To further check for endogeneity, I perform the Wu-Hausman estimate and also calculate the Durbin score. First, using the 2SLS instrumental variables approach, we develop the test instrument. In the next stage, we use the instrument to obtain the Wu-Hausman estimate and Durbin score (Table 4). The significance of test statistics in the case Wu-Hausman and Durbin estimates is a sign of the presence of endogeneity. Since both of the statistics in our results are insignificant (p > 0.05), we can conclude that our model is not likely to have endogeneity.

Consequently, the equation for the model is the following:

Yi =

β o +β 1 Generalized Trust i +β 2 Urbanization i +β 3 Education i +β 4 GDP i +β 5 Growth rate i +β 6 Corruption i +β 7 Rentier Environment i +β 8 Freedom to Affect Life i +β 9 Insurance Penetration i +β 10 Concentration Ratio i +β 11 Social Support i +β 12 Post-Soviet i + ɛ i

4.2 Qualitative Method

I complement the large-N statistical analysis with a qualitative case study. While the quantitative analysis of cross-country data treats countries as cases (see Table 9), the qualitative study provides perspective on ordinary individuals’ attitudes to and practices of insurance procurement. For my qualitative study, I draw on the results of three focus group discussions (FGD) held in Azerbaijan5 – an emerging market with the characteristics of all our independent variables, including significant resource wealth, informality (Sadigov 2014), increasing per capita income and urbanization levels, shadow economy, social support – especially the role of familism, and post-Soviet legacy. FGD as a method was chosen to identify major inter-subjective group narratives (Roller and Lavrakas 2015), which cannot be grasped in individual qualitative interviews.

One focus group discussion was held with each of the following target groups: 1. current clients of the biggest local insurance company; 2. current clients of other insurance companies; 3. people who are potentially interested in purchasing insurance, but are not clients of any insurance companies yet. Each focus group consisted of 8 people, which is an optimal size for this method (Krueger & Casey 2014, 67). Hence, there were a total of 24 respondents divided into three FGD s. The selection of participants for each FGD was based on random sampling interviews of 250 people in different regions of Azerbaijan. From those who agreed to participate in the study, I selected 24 people based on their age, income, education, gender, and place of residence to reflect the statistical distribution of the entire Azerbaijani population, and hence ensure the representation of meaningful factors affecting insurance purchase among the FGD participants. The discussion questions touched on the following topics: 1. comprehension of insurance; 2. awareness about local companies and products on the insurance market; 3. usage of insurance services; 4. satisfaction with insurance services and the level of customer loyalty to existing companies; 5. perception of insurance salespeople; 6. perception of the biggest local insurance company; 7. perception of the local insurance market.

Endogeneity test results (Wu-Hausman test and Durbin score)

Citation: Caucasus Survey 12, 2 (2024) ; 10.30965/23761202-bja10028

5 Quantitative Analysis Results

The results of regression analysis (Table 5 and Figure 1 and Figure 2) support the research expectations, thus lending support to the research Hypothesis. Generalized social trust is a significant predictor of population health insurance demand. It is positively correlated with the outcome variable, meaning that a 1 percent increase in the share of generalized trust in a society increases a given population’s voluntary health insurance purchase by approximately 19.1 percent. Among control variables, modernization (Urbanization, Education, GDP), and insurance industry-related (Insurance Penetration, Post-Soviet) factors are statistically significant predictors of voluntary insurance purchase. The research model correctly predicts the direction of association between the dependent, the independent, and the control variables, except for Urbanization. The latter is negatively associated with voluntary health insurance purchase in emerging markets. One possible explanation of the result may be that in the recent period non-urban insurance policies like agriculture/crop insurance are one the dominant segments driving the local insurance industry in many emerging markets (Crawford 2018).

Predictors of insurance demand in selected emerging markets

Citation: Caucasus Survey 12, 2 (2024) ; 10.30965/23761202-bja10028

Association between generalized social trust and voluntary insurance uptake rates

Citation: Caucasus Survey 12, 2 (2024) ; 10.30965/23761202-bja10028

Average marginal effects for the regression model

Citation: Caucasus Survey 12, 2 (2024) ; 10.30965/23761202-bja10028

Insignificant predictors of health insurance demand in emerging markets are informality and rule of law factors (Shadow Economy, Corruption), some socioeconomic (Rentier Environment), industry-specific (market Concentration Ratio), and individual (Social Support, Freedom to affect life) determinants. Rentier Environment in the research dataset included rent from all types of natural resources. The variable’s weak effect on insurance demand may be because it does not localize the effect of various natural resources. While some resources may have a dramatically higher effect on economic dynamics (including the insurance industry) than others (Ross 2012), the measurement of their separate effects might be a productive avenue for further research. Insignificance of Market Concentration may be due to the fact that insurance markets in developing countries are dominated by international corporations (AXA, SONAR, Allianz in Africa; Allianz, Prudential, Manulife, AXA in South-East Asia; Zurich and Metlife in South America). Spanning markets and regions, these industry giants compete globally, thus ensuring tight quality control to ensure high customer satisfaction. Consequently, a high market concentration spearheaded by the mix of internationally active players and purely domestic companies (especially in MENA and Latin America) may not necessarily negatively affect the population’s voluntary purchase of health insurance, while the high market concentration in some regions (like the post-Soviet one) leads to the monopolization by local companies which do not compete in international markets beyond their respective countries. In the latter case, a high market concentration should lead to the decreasing quality of service, as is discussed in-depth later, in the qualitative research section.

The random effect of the rule of law (shadow economy, corruption) on voluntary health insurance purchase can possibly be due to the fact that corruption in some cases may potentially increase the rates of economic development, savings, and market activity (Aidt 2003, Huntington 1968). Corruption in emerging markets with deficiencies in governance may enable market actors to buy their way through bureaucratic red tape (Rose-Ackermann 1999). As a result, corruption may not have a consistently uniform effect on economic dynamics (including the insurance industry). The random effect of Social Support on voluntary health insurance uptake may be due to significant cultural differences among countries (Hofstede 1991, Banfield 1958).

6 Qualitative Analysis

6.1 Background: the Insurance Industry in Azerbaijan

The latest industry statistics show that the Azerbaijani insurance sector, although profitable, is characterized by a very weak penetration and density by average international standards. While in 2010 the insurance sector accounted for 2% of GDP, in 2017 insurance accounted for only 0.79% of GDP. This is not drastically different from 2016 when the insurance penetration rate stood at 0.81%. On average, insurance payments in Azerbaijan are 15 times lower than average payments internationally (Aliyeva 2011, 4). Hence, the insurance business is relatively less mature in Azerbaijan than in other countries. The concentration ratio as the share of the top five insurance market companies (CR5) in Azerbaijan equals 76.8% (FMSA 2018a), which is higher than the international average of 67.64% (Swiss Re 2017).

More importantly, voluntary insurance uptake levels among Azerbaijani citizens are low. The existing socio-economic structure incentivizes them to turn to insurance to avoid state punishment for the lack of compulsory coverage (like in the case of car insurance). The measure of the research’s dependent variable for Azerbaijan is 1.2% of the respondents who voluntarily purchased health insurance. The result closely replicates other studies (World Bank 2005), which put the national level of health insurance coverage at 1% of the population. According to FMSA (2018d) data endowment insurance stands out as the dominant one. According to an insurance expert, Anar Sadikhov, endowment insurance cannot be viewed as a valid part of a voluntary insurance portfolio in Azerbaijan, because from the early-2010s this type of insurance was actively used by employees to evade compulsory state pension payments. According to local legislation, an employee had a choice to transfer part of his/her pension payments to an endowment insurance account, from which s/he could start earning additional interest rates (like in bank deposits). As a result, an increasing number of eligible employees started to use endowment insurance as a scheme to save on compulsory pension payments while getting additional interest income (author’s interview with Anar Sadikhov in January 2018). To put it differently, endowment insurance is perceived by employees as a source of rentier earnings, rather than a rational instrument for managing risks.

Hence, the insurance industry in Azerbaijan is dominated by an incentive structure that leads to a weak voluntary population uptake: people pay for insurance when it is compulsory by law to have it. In the majority of cases then, purchasing insurance is either an instrument to increase financial yield or an act of avoiding legal punishment for breaking compulsory insurance requirements, rather than the result of rational-instrumental calculation by placing the burden of risks on insurance products. As our FGDs show, for “insurance” in a latter sense Azerbaijanis mostly prefer to rely on informal connections, borrowing resources from family and friends while under duress.

6.2 Focus Group Discussion Findings

FGD results are used to shed light on incentives that the existing state-level socio-economic environment provides for individuals when they are faced with a need for insurance. The main thread of the discussions during the FGD s consisted of numerous stories about insurance companies’ ‘unjust’, ‘selfish’, and ‘predatory’ decisions in insurance cases. This is supported by many reports in which people lament insurance company ‘fraud’ in Azerbaijan (Karimzada 2018). Consequently, the majority of the focus group participants had low trust in the local insurance industry. Participant reasoning was the following: insurance companies and their clients have opposing interests. When an insurance case is approved, the insurance provider bears the costs, and thus earns less. On the other hand, if an insurance company succeeds in lowering the number and volume of payments to clients, the company earns more. As a result, potential and current insurance clients among my focus group respondents demonstrated almost no trust in insurance companies. The respondents argued that the companies would use every opportunity to dodge valid insurance cases. Or when unable to avoid payments, insurance companies will do everything in their power to pay less than is required to cover client damage. For instance, one of my FGD participants argued that she faced a situation when a local medical insurance company changed her doctor’s original prescription for cheaper drugs that did not treat her health problem effectively. Thus, the respondent perception of the insurance sphere is that of a zero-sum game, in which insurance companies have all the leverage and ambition to cheat their clients of valid payments. Therefore, FGD participants argued that to successfully get claims from insurance companies, one needs to have informal acquaintances (tapş) (Sayfutdinova 2018) in a given insurance company – otherwise it is almost impossible to get fair treatment.

As a counterpoise, the respondents argued that a higher emphasis on ethics, and the dominance of morality both on a societal level and individually is the only factor that can potentially keep insurance companies from breaching their formal contractual obligations toward their clients. Ethics and morality were seen by the FGD participants as the only mechanisms that guarantee the concurrence between officially declared norms (rules, laws) and their actual enforcement. The respondents defined morality as a glue that holds society together when other formal and some informal mechanisms are disintegrating under monetary relations. Neither better legislation, nor better enforcement of existing laws was viewed as a viable solution to address the perceived fundamental disparity of interests between insurance companies and their clients. Respondents reasoned that if laws are enforced and followed inadequately in other social spheres in Azerbaijan, then they will not be followed also in the insurance business, dominated by companies with a high capacity to hijack public interest. Only better/higher ethics and conscience of insurance providers can force insurance agents to respect contracts. Generally, a social environment dominated by ethics narratives and concomitant ceremonial formalism (as opposed to instrumental rationality) has been shown to define choices of the Azerbaijani and generally post-Soviet citizens in agriculture (Wegren 2005), attitudes toward legality and enforcement of contracts (Ledeneva 2006), education and research (Libman & Zweynert 2014), and other spheres (Zavisca and Gerber 2016). Hence, personal ethics becomes a counterpoise to the pervading lack of trust among post-Soviet actors striving for collective action (Yakovlev, Freinkman, Ershova 2017). Preference for ethical (rather than technocratic) solutions to socioeconomic problems is corroborated by other empirical data on the Azerbaijani population. The survey of the Azerbaijani Citizens’ KAP toward bribe offers (2015) (Sadigov 2017) showed that the respondents saw the root cause of many social problems in Azerbaijan (corruption, high divorce rates, early marriages) in the weak stature of ethics in society.

As a result of this ethics-dominated perception, the FGD participants did not define the insurance sphere as a business, based on mutual benefits, in which companies have to earn money by providing services. Instead, the field of insurance was viewed by the respondents as a service akin to state welfare, or first medical aid, in which a suffering citizen can never shoulder responsibility for causing insurance damage – because of being a victim in an insurance situation. For instance, if a client of an insurance company causes a car accident, in which she suffers physical injuries or her car gets damaged, then, according to the majority of the FGD respondents, she should not be liable for any insurance costs, even though formally (i.e., according to her insurance contract) she is guilty of creating the insurance situation. For the FGD respondents, being a victim of an insurance situation is already enough of a burden, which relinquishes the clients of any liabilities before insurance companies and other people involved in the case, even though the formal contract between the client and the company may stipulate client liability for causing the accident. Participants in all three FGD s agreed that the relations between insurance companies and their clients should be based on the scale of resulting damages for a specific accident and not on uniform contracts because the final resulting damage for the clients widely varies from one situation to another. Thus, the dominant collective narrative of FGD participants is the localization of standardized global rules, i.e., changing the scope of applicability and the meaning of universal laws according to specific circumstances.

According to the FGD respondents, if insurance companies demand liability from their clients under duress, then these insurance companies act immorally, display egoism, and hence are surely trying their best to defraud their clients. At the same time, the respondents involved in the focus groups confessed that they never read insurance contracts because of ‘laziness’ (6 FGD participants out of a total of 24 participants), and a ‘lack of interest in details’ (12 out of 24 FGD participants). They rather passively sign these contracts. The respondents assigned an insurance company the role of a ‘parent’ whose main mission is to care for the ‘safety’ of its often irresponsible ‘children’ – i.e., its clients. Consequently, the respondents demonstrate a dominant social narrative of clear-cut passivity, and reactive attitudes toward responsibilities, which was noted in Azerbaijani insurance customers in other studies too (Ibrahimli 2016).

As a result, when insurance companies do not fit this population-devised idealized image and require their clients to take responsibilities outlined in formal contracts, this reality leads to very negative feedback from local insurance consumers. The FGD participants agreed that insurance company insistence on formal contractual relations as very cold, detached and inhumane attitude that does not consider the peculiarities of various insurance situations and local circumstances which can take place in life. As one participant noted, the ‘most important quality of an insurance agent is compassion, understanding that a client’s distress is not an object of [insurance claim] negotiations’.

All these developments show a social environment inconducive to trust in insurance companies. A shared sentiment among the FGD participants was that it is more advisable and safer to rely on old and trusted informal social safety nets, turning to financial and health-related assistance to their kin, friends, and neighbors to mitigate the consequences of emergencies. In most cases, current and potential clients among the FGD participants did not know basic information about insurance products and business, its logic, assumptions, and inner workings. This finding is corroborated by other researchers. According to Ibrahimli, the level of insurance knowledge in Azerbaijan is so low that people treat their insurance policy as a formal document (on par with a driver’s license or vehicle registration document) to be presented to police during an accident: ‘the majority of people … are not even aware that they could get paid based on insurance policy’ (Ibrahimli (2017). Low population awareness also substantially decreases the rates of voluntary insurance purchase.

6.3 Putting FGD Findings in the Social Context of Azerbaijan

What society-wide processes can shed light on the FGD findings? The dominance of informality and the rentier nature of the local economy in the wake of the oil boom are potent society-wide factors that may potentially shape insurance practices and their perception by individuals in Azerbaijan.

Azerbaijani society historically has been dominated by the traditional ethos of neopatrimonialism and nepotism (Ramazanova 2011; Sadigov 2018). The dominance of informality and internationally low level of interpersonal trust (Sadigov 2017) leads to population distrust for any formal institutions, including contractual relations. On the one hand, insurance clients in Azerbaijan project their patrimonial image of society on insurance companies and see them as parents of a big family of clients. This means that formal client-firm communication based on formal contracts is seen as out of place. Communicating with insurance companies through the lens of informality, insurance clients try to go beyond their formal contracts.

It is not coincidental that some FGD participants argued that opening insurance cases and receiving insurance payments are bound only on personal acquaintances and protection in insurance companies. In this case, the majority of clients may not think of formal insurance contracts as something important at all. In such a volatile social context where formal rules are not respected and are weakly enforced, economic actors are predictably wary of investing money with insurance companies that offer in exchange “just a piece of contract paper which can easily be reneged upon” (male, 29 years-old, FGD-3 participant).

A considerable improvement in living standards in Azerbaijan led to the exacerbation of interpersonal distrust, nepotism, and conflict. Since 20056 Azerbaijan experienced an oil boom. The ensuing dramatic rise in per capita incomes led to the rentier economic development model, in which government spending relies heavily on oil windfalls. The Azerbaijani population’s economic activity replicates this rentier model. Roughly between 7–10% of the economically active population in Azerbaijan lives off a rentier income (SSCAR 2018).

In such a rentier context, when both state and population depend on natural and monetary rents, without active production of added value based on the instrumental application of scientific methods, insurance based on a business model of probabilistic monetary efficiency may not be easily accepted. Living off natural rents, the population may project the same type of business model to insurance companies. In this type of thinking, insurance payments of clients are an ‘easy prey’ source of money that people feed companies for further ‘consumption’. In this mindset, an insurance company does not have an obligation to provide any service. In line with this, one of the dominant views among the FGD participants of the study was that the insurance business did not add any economic value – these companies just feed off client payments akin to ‘donations’, while doing their best to shield themselves off from their clients’ claim payments.

7 Conclusion

This article offered a comprehensive analysis of the determinants of voluntary health insurance purchase in emerging markets. Addressing the dearth of empirical measurements of voluntary insurance purchase by emerging market populations, this article provides a systematic analytical measurement of the impact of social trust on voluntary health insurance uptake in emerging markets. Combining regression analysis and qualitative FGD data in a mixed-methods research design, this article argues that generalized social trust is positively associated with voluntary insurance purchases among emerging market populations. Qualitative data contributes to large-N statistical analysis by showing how the dominance of informality, and a rentier economic environment leads to the rejection of formal insurance in an insurance market with a high concentration and weak competition.

This article has several theoretical implications. First, by establishing a positive association between generalized trust and insurance demand, this article’s findings contribute to the debates in insurance research. My findings support a broader claim that significant trust in a social environment in emerging markets creates incentives to invest their resources in long-term insurance schemes. Thus, less trust in society pushes people to integrate more with family and friends in bonding social structures, and hence rely on informal safety nets, rather than formal insurance contracts with companies.

Second, the research finding of the insignificant effect of the rentier environment on population insurance demand contributes to resource-dependence literature, by implicitly showing that oil and gas rents may have a more dramatic effect on the development of markets and economies in comparison to the dependence on other natural rents. Third, the finding that the rule of law (Shadow Economy, Corruption) has a statistically insignificant effect on voluntary health insurance purchase corroborates studies with a similar outcome (Kjosevski 2012). More broadly, the finding contributes to the academic debates on whether corruption raises or decreases market efficiency (Meon and Weill 2010). Concurring with broader literature, the finding may suggest that the effect of corruption and shadow economy on population choices (including insurance procurement) is mediated by an intermediate mechanism. As suggested by relevant literature (Bardhan 1997, Rose-Ackerman 1999), most likely corruption aids market operation in countries with weak bureaucratic efficiency.

Several suggestions for future research can be proposed in turn. First, subsequent studies can expand this article’s scope, by collecting and researching data on all emerging market populations’ voluntary purchase of insurance products in general. Second, future studies are well advised to pursue further some unexpected results of the research. The random effect of rule of law (corruption and shadow economy), the role of resource rents, the effect of insurance market competition on potential and actual customer satisfaction, and the impact of social support on insurance procurement are all important research problems in their own right. Third, methodologically, future research can use small-N studies comparing developments in various countries to provide further a nuanced picture of the causal impact of generalized trust on emerging market populations’ insurance perception, demand, and actual uptake. The combination of a large-N study with a single-case analysis by this research should be viewed as an initial step, while future research can expand available research cases. This might help the insurance industry, as more recent and comprehensive data on incentives for voluntary insurance purchase by population in emerging markets becomes available.

Disclosure Statement

No conflict of interest was reported by the author.

Appendix: FGD Participant Information

The list of the participants for the Focus Group Discussion One

Citation: Caucasus Survey 12, 2 (2024) ; 10.30965/23761202-bja10028

The list of the participants for the Focus Group Discussion Two

Citation: Caucasus Survey 12, 2 (2024) ; 10.30965/23761202-bja10028

The list of the participants for the Focus Group Discussion Three

Citation: Caucasus Survey 12, 2 (2024) ; 10.30965/23761202-bja10028

List of countries included in the study

Citation: Caucasus Survey 12, 2 (2024) ; 10.30965/23761202-bja10028

References

Aidt, T.S. 2003. “Economic analysis of corruption: a survey.” The Economic Journal, 113, 491: 632–652.

Africa Re. 2019. Insurance market concentration. https://www.africa-re.com/dashboards. [Accessed 19 September 2020].

Africa Re. 2020. Insurance penetration. https://www.africa-re.com [Accessed 18 Sep-tember 2020].

Ahlgrim, K.C., & D’Arcy, S.P. 2012. The effect of deflation or high inflation on the insurance industry. Casualty Actuarial Society, Canadian Institute of Actuaries and Society of Actuaries.

Atlas magazine. 2016. Top 5 insurance companies per turnover in each country. https://www.atlas-mag.net [Accessed 10 September 2020].

AIG. 2013. MENA Insurance Markets. http://www.meinsurancereview.com/Portals/1057/PDF/MENA_Ins_Mkts-Mini_Guide2013.pdf [Accessed 21 January 2021].

Alhassan, A.L., & Biekpe, N. 2016. “Determinants of life insurance consumption in Africa.” Research in International Business and Finance 37: 17–27.

Aliyeva, L. 2011. Azərbaycanda siğorta sistemi. [Insurance system in Azerbaijan.] In Azerbaijani. Baku: Qanun.

Banfield, Edward. 1958. The Moral Basis of a Backward Society. Glencoe: The Free Press.

Black, K., & Skipper, H.D. 2000. Life and health insurance. Upper Saddle River, New Jersey: Prentice Hall.

Borisova, N. 2017. “Condition and prospects of developing life insurance market in Uzbekistan.” In Russian. Mirovaya Ekonomika 4, 94: https://cyberleninka.ru/article/v/sostoyanie-i-perspektivy-razvitiya-rynka-strahovaniya-zhizni-v-uzbekistane [Accessed 13 December 2020].

Cai, J., De Janvry, A., & Sadoulet, E. 2015. “Social networks and the decision to insure.” American Economic Journal: Applied Economics, 7, 2: 81–108.

Camargo, A. and Gonçalves, L. 2014. Encouraging access to insurance in Peru. Lima: Access to Insurance Initiative. https://a2ii.org/sites/default/files/reports/2014_11_21_country_diagnostic_peru.pdf [accessed January 5, 2021].

Chen, H., Cummins, J.D., Viswanathan, K.S. and Weiss, M.A. 2014. “Systemic risk and the interconnectedness between banks and insurers.” The Journal of Risk and Insurance 81, 3: 623–652.

Cole, S., Sampson, T., & Zia, B. 2011. “Prices or knowledge?” The Journal of Finance, 66, 6: 1933–1967.

Crawford, Shaun. 2018. “Global insurance trends analysis 2018”. Ernst &Young. https://www.ey.com/Publication/vwLUAssets/ey-global-insurance-trends-analysis-2018/$File/ey-global-insurance-trends-analysis-2018.pdf [Accessed 12 October 2020].

Dercon, S., Hill, R.V., Clarke, D., Outes-Leon, I., & Taffesse, A.S. 2014. “Offering rainfall insurance to informal insurance groups.” Journal of Development Economics, 106: 132–143.

Dragos, S.L. 2014. “Life and non-life insurance demand.” Economic research-Ekonomska istraživanja 27, 1: 169–180.

Elango, B., & Jones, J. 2011. “Drivers of insurance demand in emerging markets.” Journal of Service Science Research, 3, 2: 185–204.

Ernst &Young. 2014. Global Consumer Insurance Survey. https://www.ey.com/Publication/vwLUAssets/EY-the-EY-global-consumer-insurance-survey-2014/$FILE/EY-the-EY-global-consumer-insurance-survey-2014.pdf [Accessed 15 December 2020].

Faulkner, J. 2002. “Culture and corruption-the development of insurance in post -communist countries.” Insurance Research and Practice 17, 2: 16–22.

FMSA (Financial Markets Supervisory Authority). 2018a. Premiums Written and Claims Paid in 2018. https://www.fimsa.az/assets/upload/files/January-December%202018.xlsx. [Accessed 12 October 2020].

FMSA. 2018b. Premiums Written and Claims Paid in 2017 (by insurance types). https://www.fimsa.az/assets/upload/files/Yanvar_dekabr_sinifler_2017(3).xlsx. [Accessed 19 September 2020].

FMSA. 2018c. Premiums Written and Claims Paid in January–December 2017 (by insurance companies). https://www.fimsa.az/assets/upload/files/Yanvar_dekabr_%C5%9Firk%C9%99tl%C9%99r_2017.xlsx. [Accessed 12 September 2022].

FMSA. 2018d. Insurance market by Classes. https://www.fimsa.az/en/By%20Classes.

Gallup. 2017. Gallup World Poll. https://www.gallup.com/services/177797/country-data-set-details.aspx [Accessed 19 September 2022].

Greene, M.R. 1954. “Life insurance buying in inflation.” Journal of the American Association of University Teachers of Insurance 21, 1: 99–113.

Helliwell, J., Layard, R., and Sachs, J. 2018. World Happiness Report 2018. New York: Sustainable Development Solutions Network.

Hess, T., Leuenberger, L., & Scherrer, A. 1996. “The insurance industry in Eastern Europe: Recovery has begun.” Sigma 8. Zurich: Swiss Re.

Hofstede, G. 1991. “Empirical models of cultural differences.” In N. Bleichrodt & P.J.D. Drenth, eds., Contemporary issues in cross-cultural psychology, 4–20. Lisse: Swets & Zeitlinger Publishers.

Hofstede, Geert. 1995. “Insurance as a product of national values.” The Geneva Papers on Risk and Insurance-Issues and Practice, 20, 4: 423–429.

Huntington, Samuel P. 1968. Political Order in Changing Societies. New Haven, CT: Yale University Press.

Jain, A., Nundy, S., & Abbasi, K. 2014. Corruption: medicine’s dirty open secret. BMJ. http://pbtindia.com/wp-content/uploads/2014/06/BMJ-Healthcare-Corruption-June-26-2014.pdf [Accessed 19 September 2020].

Jowett, M.R. 2002. “Voluntary health insurance in Vietnam.” Unpublished Ph.D. dissertation, University of York.

Ibrahimli, U. 2016. “Challenges of the Post-Soviet insurance market.” https://www.linkedin.com/pulse/challenges-post-soviet-insurance-market-u%C4%9Fur-i%CC%87brahimli/ [Accessed 12 December 2020].

Ibrahimli, U. 2017. “Postsovet ölkələrində sığortanın inkişaf problemləri” [Problems of insurance development in post-Soviet states]. http://banker.az/postsovet-olk%C9%99l%C9%99rind%C9%99-sigortanin-inkisaf-probleml%C9%99ri [Accessed 12 February 2021].

Karimzada, D. 2018. “Insurance companies’ fraud.” In Azerbaijani. Minval. http://minval.info/sigorta-sirk-tl-rinin-firildaqlari-surucul-r-bogaza-yigilib/35598. [Accessed 12 December 2020].

Kendall, Diana, Linden, R., and Murray, J. 2007. Sociology in our times. 4th Canadian ed. Toronto, Ontario, Canada: Thomson Nelson.

Kjosevski, J. 2012. “The determinants of life insurance demand in Central and Southeastern Europe.” International Journal of Economics and Finance 4, 3: 237–247.

Koblensky, W. 2017. “How big a problem are corruption and bribes in insurance?” Insurance Business, 17 March, https://www.insurancebusinessmag.com/us/news/breaking-news/how-big-a-problem-are-corruption-and-bribes-in-insurance-63054.aspx [Accessed 14 September 2020].

Krueger, R.A., and Casey, M.A. 2014. Focus groups: A practical guide for applied research. Los Angeles: Sage.

Ledeneva, A.V. 2006. How Russia really works: The informal practices that shaped post-Soviet politics and business. Ithaca: Cornell University Press.

Libman, A. and Zweynert, J. 2014. “Ceremonial science.” Economic Systems 38, 3: 360–378.

Mahdavy, H. 1970. “The Patterns and Problems of Economic Development in a Rentier Stare: The Case of Iran.” In M.A. Cook, ed., Studies in Economic History of the Middle East, 428–467. London: Oxford University Press.

Mai, H., and Schneider, F. 2016. “Size and development of the shadow economies of 157 worldwide countries: Updated and new measures from 1999 to 2013.” Journal of Global Economics 4, 3: 1–15.

Mazzuca, S.L. 2013. “Lessons from Latin America: The rise of rentier populism.” Journal of Democracy 24, 2: 108–122.

MAPFRE. 2015. Latin American Insurance Market. https://www.fundacionmapfre.org/documentacion/publico/i18n/catalogo_imagenes/grupo.cmd?path=1091144 [Accessed 10 September 2020].

Méon, P.G., & Weill, L. 2010. “Is corruption an efficient grease?” World Development 38, 3: 244–259.

Mobarak, A.M., and M.R. Rosenzweig. 2012. Selling formal insurance to the informally insured. Economic Growth Center Discussion Paper (1007). https://www.econstor.eu/bitstream/10419/59144/1/715687328.pdf [Accessed 19 September 2020].

Murgai, R., Winters, P., Sadoulet, E., & De Janvry, A. 2002. “Localized and incomplete mutual insurance.” Journal of Development Economics 67, 2: 245–274.

Naujoks, Henrik, Camille Goossens, Gunther Schwarz, Harshveer Singh, Andrew Schwedel and David Whelan. 2017. Customer Behavior and Loyalty in Insurance. Report, Bain and Company, 14 September. https://www.bain.com/insights/customer-behavior-loyalty-in-insurance-global-2017/ [Accessed 19 September 2020].

OECD. 2020. Insurance indicators: Penetration. https://stats.oecd.org/Index.aspx?QueryId=25444 [Accessed 29 September 2020].

Okruhlik, G. 1999. “Rentier wealth, unruly law, and the rise of opposition: the political economy of oil states.” Comparative Politics, 31, 4: 295–315.

Park, H., Borde, S.F., & Choi, Y. 2002. “Determinants of insurance pervasiveness: a cross-national analysis.” International Business Review 11, 1: 79–96.

Park, S., & Lemaire, J. 2011. “Culture matters: Long-term orientation and the demand for life insurance.” Asia-Pacific Journal of Risk and Insurance 5, 2: 1–21.

Polese, A., Morris, J., Kovács, B., & Harboe, I. 2014. “‘Welfare states’ and social policies in Eastern Europe and the former USSR: where informality fits in?” Journal of Contemporary European Studies, 22, 2: 184–198.

Prokopyeva, E. 2015. “Life insurance in Russia: features of regional development.” Ekonomika regiona. In Russian. https://cyberleninka.ru/article/n/life-insurance-in-russia-features-of-regional-development [Accessed 21 September 2020].

PwC 2018. “Ready and Willing.” https://www.pwc.co.za/en/assets/pdf/south-african-insurance-2018.pdf [Accessed 23 September 2020].

Pye, R.B. 2005. “The evolution of financial services in transition economies: An overview of the insurance sector.” Post-communist Economies 17, 2: 205–223.

Ramazanova, A. 2011. Trust towards Public School Teachers, Quality of Education and Human Capital in Azerbaijan. Research paper, Khazar University; https://core.ac.uk/download/pdf/161801937.pdf [Accessed January 23, 2021].

Rose-Ackermann, Susan. 1999. Corruption and Government. Cambridge: Cambridge University Press.

RNSF. 2017. Extending coverage: Social protection and the informal economy. Experiences and ideas from researchers and practitioners. Research, Network and Support Facility, ARS Progetti, Rome; Lattanzio Advisory, Milan; and AGRER, Brussels.

Ross, M. 2012. The oil curse. Princeton, NJ: Princeton University Press.

Roller, M.R., & Lavrakas, P.J. 2015. Applied qualitative research design. New York: The Guilford Press.

Sadigov, T. 2014. “Corruption and social responsibility: bribe offers among small entrepreneurs in Azerbaijan.” East European Politics 30, 1: 34–53.

Sadigov, T. 2017. “Localization, formalism, and passivity: symbols shaping bribe offers in Azerbaijan.” Journal of Civil Society 13, 4: 406–425.

Sadigov, T. 2018. “A Clash of Cultures: How Rural Out Migrants Adapt to Urban Life in Baku.” Caucasus Analytical Digest (CAD), 101, 11–14.

Sayfutdinova, L. 2018. “Tapş.” In Ledeneva, A. ed. The Global Encyclopaedia of Informality. Vol.1, 80–84. London: LUC.

Schanz, Alms & Company. 2018a. ASEAN Insurance Pulse 2018. https://pulse.schanz-alms.com/files/media/files/db31b38b9be35551b807792b0d16b84a/Pulse_Asean18_Web2.pdf [Accessed 29 September 2020].

Schanz, Dr. Alms & Company. 2018b. Africa Insurance Barometer 2018. https://pulse.schanz-alms.com/files/media/files/aac2d1e0123a5b5f5df7008326f20a3a/Africa_Insurance_Barometer_WEB_E.pdf [Accessed 30 September 2020].

Schanz, Dr. Alms & Company. 2018c. MENA Insurance Pulse 2018. https://pulse.schanz-alms.com/files/media/files/04bc7e703829af737e746bb0a805626f/MENA_Insurance_Pulse_2018.pdf [Accessed 10 September 2020].

Schneider, F. 2016. “Out of the shadows: Measuring informal economic activity.” In B. Riley, & T. Miller, eds., 2016 Index of Economic Freedom, 35–49. The Heritage Foundation. www.heritage.org/international-economies/report/2016-index-economic-freedom-yet-more-evidence-free-trades-benefits. [Accessed 11 January 2021].

Shi, X., Wang, H.J., & Xing, C. 2015. “The role of life insurance in an emerging economy.” Journal of Banking & Finance 50: 19–33.

SSCAR. 2018. Labor Resources (dynamics). https://www.stat.gov.az/source/labour/en/001_5en.xls [Accessed 19 September 2020].

Swiss Re. 2017. “Insurance: adding value to development in emerging markets.” Sigma, 4. https://www.swissre.com/dam/jcr:0c654530-302f-4442-b01e-585d11ea3beb/sigma4_2017_en.pdf [Accessed 19 September 2020].

Swiss Re. 2018. “World insurance in 2017.” Sigma, 3. https://www.swissre.com/dam/jcr:a160725c-d746-4140-961b-ea0d206e9574/sigma3_2018_en.pdf [Accessed 10 September 2020].

Transparency International. 2011. Corruption Perception Index. https://www.transparency.org/cpi2011 [Accessed 12 September 2020].

Transparency International. 2018. Corruption Perception Index. https://www.transparency.org/cpi2018 [Accessed 1 September 2020].

UNESCO. 2017. Lower secondary completion rate. Paris: UNESCO Institute for Statistics.

Wegren, S.K. 2005. “Russian agriculture during Putin’s first term and beyond.” Eurasian geography and economics 46, 3: 224–244.

Williams, C.C. & Sara Nadin. 2012. Tackling informal entrepreneurs. In Mai Thi Thanh Thai and Ekaterina Turkina, eds., Entrepreneurship in the Informal Economy: Models, Approaches and Prospects for Economic Development, 161–176. New York: Routledge.

Willis Towers Watson. Asia Insurance Market Report 2018. https://www.willistowerswatson.com/-/media/WTW/PDF/Insights/2018/02/asia-insurance-market-report-2018.pdf [Accessed 2 September 2020].

World Bank. 2005. Azerbaijan Health Sector Review Notes. Washington, DC: World Bank.

World Bank. 2011. Global Financial Inclusion survey. Washington, DC: World Bank; https://datacatalog.worldbank.org/dataset/global-financial-inclusion-global-findex-database.

World Bank. 2017. World Development Indicators. Washington, DC: World Bank.

World Values Survey. 2014. WVS Database. http://www.worldvaluessurvey.org/WVSDocumentationWV6.jsp [Accessed 19 September 2020].

Yakovlev, A., Freinkman, L.M. and Ershova, N.V. 2017. “The evolution of the collective forms of interaction between foreign business and government in Russia.” Journal of Institutional Studies 9, 4: 16–36.

Yusuf, T.O., Gbadamosi, A., & Hamadu, D. 2009. “Attitudes of Nigerians towards insurance services: an empirical study.” African Journal of Accounting, Economics, Finance and Banking Research 4, 4: 34–46.

Zavisca, J.R. and Gerber, T.P. 2016. “The socioeconomic, demographic, and political effects of housing in comparative perspective.” Annual Review of Sociology 42: 347–367.

Zelizer, V.A. 1978. “Human values and the market: The case of life insurance and death in 19th-century America.” American journal of sociology 84, 3: 591–610.

Voluntary means here a type of insurance products which are not mandatory according to relevant national legislation.

“Generalized trust” is defined in this study as trust in other members of society. It may be distinguished from particularized trust, which corresponds to trust in the family, neighbors, or close friends.

Insurance penetration is the share (in %) of a country’s GDP that constitutes the premium income of insurance industry (or the amount of premium income divided by the volume of GDP).

Post-communist CEE countries demonstrate considerably less insurance market concentration than post-Soviet states (Kjosevski 2012).

FGD s were held in Baku (Azerbaijan) in December 2017 by the author of the article. The profile of each FGD participant is provided in the Appendix (Tables 6, 7, and 8).

The year when first oil revenues from 1994 oil contracts started to flow into the state budget.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}