1

mdbs are supranational institutions typically established and owned by states.1 Some mdbs have entities other than states as members; the European Bank for Reconstruction and Development (ebrd), for instance, comprises the European Investment Bank (eib) as a shareholder.2 While they differ in terms of membership, purpose and geographical scope, mdbs are united in their function of lending money to sovereign or non-sovereign borrowers to promote social and economic goals and achieve a variety of development goals based on the particular mdb’s mandate and mission.3

The states that establish an mdb, along with states who become members of the mdb after its formation, also own the mdb as shareholders. At the time of establishment, typically there is an injection of initial capital in proportion to the organization’s ownership structure. This capital injection allows the organization to begin its operations, such as acquiring a headquarters and hiring initial staff. After this point, the member states’ financial contributions stop and the usual way an mdb funds its ongoing operations is through the issuance of bonds on the international debt capital markets, where mdbs raise the large quantities of funds needed to finance their loans. In this way, as this article underscores, mdbs play an important role not only through their financings, but also via their engagement in the international debt capital markets.

Until recently, such bonds issued by mdbs were not linked to specific types of projects that the mdb was financing under its mandate and mission. The proceeds of a bond issue would typically be included in an mdb’s ordinary resources and be used to finance such mdb lending activities in general. Beyond this, however, mdbs’ bond frameworks did not provide for bond proceeds to apply differently based on any eligibility criteria related to the type or theme of a project.

However, in a major departure from established practice, starting in 2007 two of the largest mdbs – the eib and the International Bank for Reconstruction

This chapter is written in light of these rapid developments in the labelled bond concept, which deserve to be better explored and understood in the literature.6 Furthermore, in the broader society and even among some practitioners in the field, there is a need for further awareness of and discussion about the various types of labelled bonds, their taxonomy and their related legal and policy considerations. Similarly, greater attention should be given to the role labelled bonds can play in responding to – and recovering from – the covid-19 pandemic, as well as to mitigate climate change risks in the longer term.

Against this backdrop, this chapter will provide a brief history of the development of green bonds. Following this, the focus will turn to the rapid evolution and expansion of the labelled bond concept, including, most recently, sustainability-linked bonds. As a case study, covid-19 Response Bonds provide a timely and relevant illustration of the emerging types of thematic bonds and their attendant legal issues. The chapter will then look at the latest developments related to, and the future of, the labelled bond concept. Finally, a call for further innovation and growth in themed bonds, and the critical role of mdbs in this connection, will accompany other concluding thoughts.

2

This section provides a summary of the background to the emergence of green bonds in the context of mdbs, starting with traditional bond issuance, key developments, and ongoing diversification of the green bond issuer base.

mdbs have a long experience in financing their lending activities by borrowing money from international debt capital markets by issuing bonds. Distilling these to their essence, bonds are commoditized debt instruments representing, in substance, a promise from the issuer to repay the principal of the bond to the holder at maturity in addition to, if applicable, a periodic coupon over the life of the bond. The World Bank, for instance, has issued bonds since 1947 to finance its development projects.7 These bonds issued by mdbs were historically not linked to specific or thematic project types.

However, in 2007 and 2008, two watershed events occurred that paved a new way for mdbs to raise money on the debt capital markets. In 2007, eib issued a “Climate Awareness Bond”. The issue of this bond marked a turning point as proceeds were for the first time “ring-fenced” in a specific portfolio.8 Shortly thereafter, in 2008, the World Bank issued its first green bond in response to market demand and involving a diverse range of stakeholders. The proceeds of this particular bond would be applied exclusively to eligible environmental projects and impact reporting was included as a key element of the process. An interdisciplinary research body, the Centre for International Climate and Environmental Research (cicero), was closely involved in the green bond’s development and provided the first research-based evaluation of the green bond investment framework to evaluate its environmental robustness (known as a second opinion).9 Setting aside their tailored use of proceeds wording and any corresponding additional disclosure, green bonds otherwise closely follow the issuance process used for classic unlabelled bonds (including in respect of

Initially, only mdbs issued green bonds, and the volumes were small. Volumes have since increased remarkably, as shown in Graph 10.1 below. Growth in volume has gone hand in hand with a diversification of the issuer type.11 Presently, in addition to mdbs, green bonds are also issued by commercial banks, corporates, sovereigns and a number of government agencies. A notable agency example is Fannie Mae, which in 2020 was the largest issuer of green bonds by volume with total a total issuance of usd 13 billion.12

Growth in issuance of green bonds 2007 – Nov. 2020

source: crédit agricole cib sustainable banking (as of 20 november 2020){kind=link}

Despite this growth in volume and diversification, the overall green bond market represented less than 1% of the total bond market in 2019 and was

3 Beyond Green: Evolution and Expansion of the Bond Concept

Following the initial green bond issuances in the late 2000s, green bond design underwent a rapid evolution to cover even more targeted themes than “just” green. An illustrative example is the Nordic Investment Bank’s (nib) inaugural Nordic–Baltic ”Blue Bond” for water management and protection. This Nordic–Baltic ”Blue Bond” was issued in February 2019 and was the first blue bond listed on Nasdaq’s Nordic Sustainable Debt Market. For context, nib has been issuing green bonds since 2011, for a total of almost eur 5 billion, financing over 90 projects. Given nib has an explicit environmental mandate and that it had been assessing the environmental impact of projects for a long time prior, issuing green (and other themed) bonds was a logical (and easy) step for nib. The same can be said, mutatis mutandis, for a number of mdbs.

The Nordic–Baltic “Blue Bond” was issued under nib’s Environmental Bond (neb) Framework. This Framework has a “Dark Green” second opinion from cicero, which is the highest possible grade.14 The neb framework allows neb bonds to finance projects from several of nib’s seven eligible project categories, or to just focus on one type, which was the case for the Nordic–Baltic “Blue Bond”. The proceeds of the Nordic–Baltic “Blue Bond” were designated for eligible projects in the fields of wastewater treatment and water pollution prevention. More specifically, eligible projects under the Nordic–Baltic “Blue Bond” included those with the aim of (i) reducing discharges into water (mainly phosphorus, nitrogen, organic matter, heavy metals, plastics and pharmaceuticals); (ii) supporting pollution prevention and the development of climate change resilient infrastructure; and (iii) minimizing groundwater extraction and contamination, and improving the replenishment of aquifers, extending protected areas, and strengthening the protection and restoration of water and marine ecosystems, and biodiversity (such as wetlands, rivers and lakes, coastal areas and open sea zones).15

The first Nordic–Baltic “Blue Bond” issued by nib is one among an increasing number of bonds whose proceeds are ring-fenced to fund specified categories of eligible projects. Presently, four main categories of labelled bonds can be observed in the market. First, Green Bonds, the proceeds of which, as described above, are used to finance eligible environmental projects. Second, Social Bonds are loans used to finance, as the name implies, eligible social projects. An example is the African Development Bank’s Social Bond, the proceeds of which are used to finance projects including rural electrification, last mile connectivity for rural communities, sustainable water supply and sanitation delivery, as well as other categories of projects with positive social impact and outcomes.17 The third type of labelled bonds are “Sustainability Bonds”, the proceeds of which are used to finance a combination of eligible green and social projects. An example is “Sustainable Development Bonds” issued by the World Bank, investing in which supports the World Bank Group’s twin goals of ending extreme poverty and promoting shared prosperity, as well as supporting the Sustainable Development Goals and positive social and environmental outcomes in countries.18 And fourth, Sustainability-linked Bonds, the financial and/or structural characteristics of which vary depending on whether the issuer achieves predefined sustainability or other environmental, social or governance (esg) objectives. This type of labelled bond is still in the nascent phase of development, with the first issue taking place in late 2019 by the

Labelled bonds are regulated like any other fixed-income securities. Additionally, a number of industry bodies have designed frameworks governing best practices regarding labelled bonds, namely the International Capital Market Association (icma’s) Green Bond Principles, Social Bond Principles, Sustainability Bond Guidelines and Sustainability-Linked Bond Principles (slbp). icma is a highly regarded non-governmental entity in the capital markets that sets industry best practices and could be regarded as exercising a quasi-regulatory function. These icma Principles are voluntary guidelines developed in collaboration with market players (issuers, investors, arranging banks, etc.) and, while they carry weight, are not formally binding legal standards.

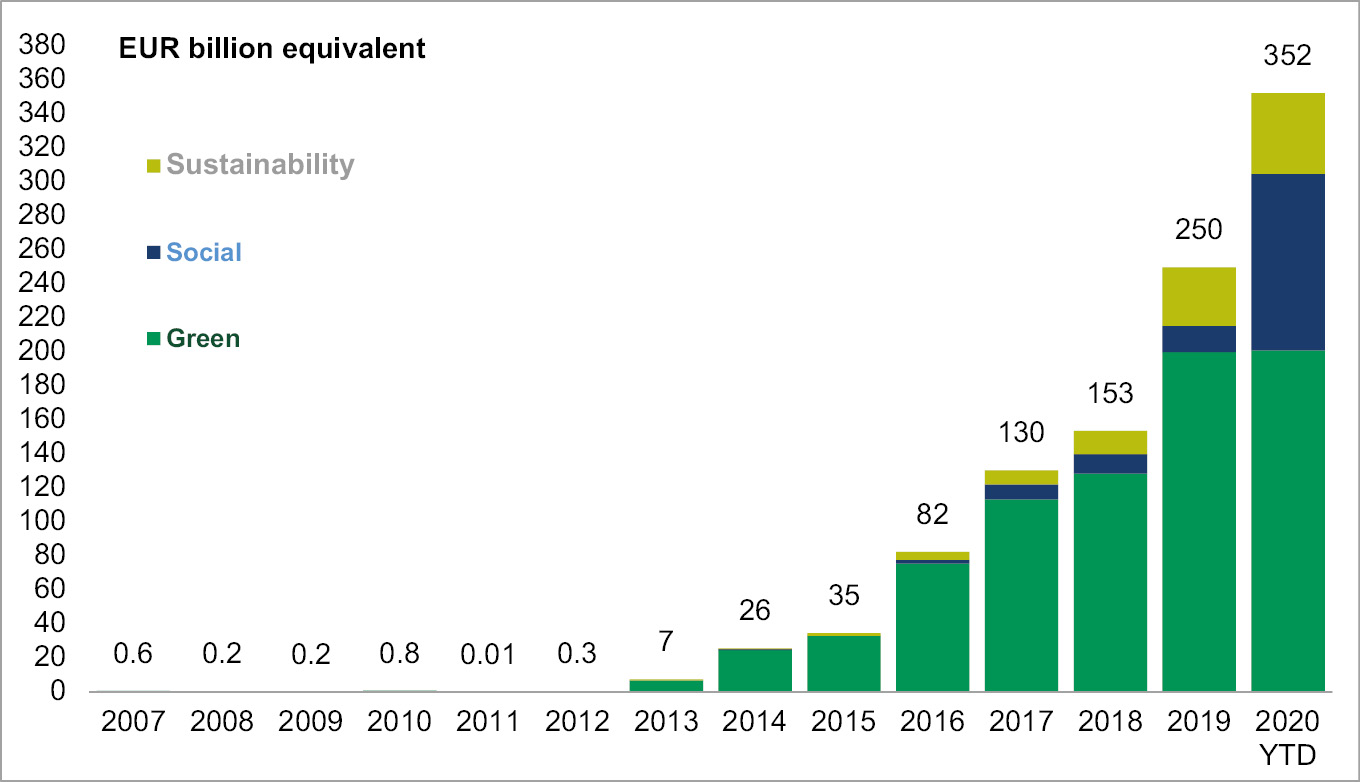

As with green bonds, other new types of labelled bonds have experienced rapid expansion in terms of volumes and diversity of issuers. As the graph below (Graph 10.2) illustrates, the labelled bond market has grown from eur 7 billion in 2013 to a projected eur 352 billion in 2020. Green bonds still constitute the bulk of outstanding labelled bonds; however, social and to a lesser extent, sustainability bond volumes have increased rapidly, particularly over the last couple of years.

Volume and type of labelled bonds issued 2007 – Nov. 2020

Note: Excluding sustainability-linked bonds.

source: crédit agricole cib sustainable banking (as of 20 november 2020); excludes sustainable development bonds which are not icma compliant; percentages in graph refer to bonds in eur (ex-gov){kind=link}

As a proportion of total bonds issued, as of late 2020, green, social, sustainability, and sustainability-linked bonds – issued by mdbs and other market players – represented almost 14% of bonds issued in eur. By way of contrast, in 2013, the same amount stood at just 0.4%.20

4

To illustrate the rise of labelled bonds beyond the most well-known green bond type (in addition to the above-mentioned blue bond), the global tragedy of the coronavirus pandemic – still ongoing at the time this chapter was written – provides a timely, if not sobering, opportunity for a case study in the form of covid-19 Response Bonds.

covid-19 first emerged in early 2020 and subsequently spread around the world resulting in 116 million confirmed cases and 2.5 million deaths as of early March 2021.21 The effects of the covid-19 pandemic go beyond its impact on global health, with profound social and economic consequences and suffering businesses, leading to, among others, increased unemployment and underemployment. In this particular context, regular bond issuers – including states and government agencies, and international and supranational organizations, as well as corporates – needed additional resources to effectively react to the

mdbs were at the forefront of issuing this new type of bond. In particular, some mdbs used their existing social bond frameworks to issue bonds in relation to covid-19. For example, the Council of Europe Development Bank (ceb) responded to the covid-19 crisis by quickly leveraging off its existing Social Inclusion Bond framework in order to support its member countries, whilst being in line with existing initiatives, to launch a eur 1 billion seven-year covid-19 Social Inclusion Bond on 2 April 2020. Later the same year, a usd 500 million three-year Global covid-19 Response Social Inclusion Bond followed.22

In contrast, other mdbs created new bond frameworks in response to the pandemic. For example, nib issued its first Response Bond in March 2020 (for eur 1 billion) in response to a call from its Governors to take decisive action in response to the covid-19 pandemic. This Response Bond financed eligible projects that aimed at alleviating the social and economic consequences caused by the covid-19 pandemic in nib’s member countries in the Nordic-Baltic region. nib has no explicit “social mandate”, but social aspects are captured under its “productivity” mandate which are reflected in the purpose of the Bank and its constituent documents. In addition, nib’s defined purpose implies that it can also play a stabilizing role during economic crises.

To issue these bonds, nib created a brand new “Response Bond Framework” under which two transactions (as at 15 October 2021) have been taken. This Response Bond Framework includes a description of, among other matters, the eligible project selection process, the use and management of proceeds from the sale of such bonds, and the corresponding reporting.23 The bonds issued under nib’s Response Bond Framework are intended to fund eligible response loans extended by the Bank, with such bonds otherwise following all financial, risk and liquidity policies and guidance under which nib normally issues debt.24 Market demand was strong: the eur 1 billion issue, for example,

An early question that arose when covid-19 Response Bonds began to be issued to finance the response to the covid-19 pandemic was the categorization of these bonds. In this respect, covid-19 Response Bonds are best apprehended of as a new type altogether of social bond. As alluded to earlier, social bonds finance projects aimed at either a specified social issue or which seek to achieve a desired social outcome. A cursory review of covid-19 Response Bonds, including those issued by nib, shows that covid-19 Response Bonds are typically designed to address the health, social or economic consequences of the coronavirus.

From the perspective of icma, debt capital market issuers can indeed issue a Social Bond related to covid-19 even if they have not previously issued a Social Bond. But when doing so, the body has underscored the importance of addressing the four key components of icma’s Social Bond Principles.25 Those four components relate to the use of proceeds, project evaluation and selection, proceeds management and reporting. Proceeds must go exclusively towards addressing or mitigating social issues wholly or partially emanating from the coronavirus outbreak.26 There is, however, no list published by icma regarding these social issues. Having said that, in the early stages of the pandemic, the International Finance Corporation noted for illustrative and guidance purposes some industry-specific case studies of use of proceeds. For example, in the mdb sphere, use of proceeds could finance loans to small businesses affected by the adverse economic effects of the pandemic. Another example, for corporate issuers in the pharmaceutical industry this time, would be use of proceeds covering financing covid-19 testing, vaccine or medication research and development. In the manufacturing industry, use of proceeds could target the manufacturing or modification of machines to produce safety equipment and hygiene supplies.27

While covid-19-related bonds issued by mdbs as Social Bonds should follow the Social Bond Principles, a departure from those principles may be justified by the nature of the circumstances. When doing so, the reasons for, and the fact of, non-adherence to the Social Bond Principles must be articulated clearly. For example, nib specifically mentions in its Response Bond Framework that: “[T]he framework has not obtained a Second Party Opinion. Despite playing an important role in societies’ response to the crisis, the framework should not be considered compliant with the Social Bond Principles”.29

This was a conscious choice given the urgency and severity of the situation, and because nib was not fully certain that it could adhere in total to the Social Bond Principles. Therefore, it was a more short-term solution rather than nib’s normal long-term view and proper assessment of projects upfront before financing.

nib’s experience in using covid-19 Response Bonds illustrates the tensions associated with balancing a “need for speed” with adequate commitment regarding the use of proceeds, project evaluation and selection, proceed management and reporting elements of social bonds. “Green washing” has been cited as a common problem in respect of green bond issues. This refers to the phenomenon where bonds labelled as “green” have in fact little positive environmental impact and may actually harm the environment instead.30 Similarly, there is a risk that social bonds issued in response to the pandemic may involve “social washing”. It goes without saying that this is to be avoided at all costs when mdbs issue response bonds, and that transparency and accountability is vital for the credibility and viability of social bonds and labelled bonds in general.

To conclude, the usual considerations concerning transparency relating to management of proceeds, monitoring requirements, mechanisms to track funds, impact measurement, third-party assessments, and other reporting elements should be respected in the context of covid-19 Response Bonds, the issuance of which follows the Social Bond Principles. For those Response

Therefore, in the absence of strong governance, there are increased risks for not only the integrity of individual covid-19 bond issues but also the broader market when departing from the Social Bond Principles in the interests of speed. This emphasizes the more fundamental need for mdbs to operate with sound banking principles and the highest standards of good governance.

5 Latest Development and Future Prospects for Labelled Bonds

This section discusses some of the emerging trends and developments in the sphere of labelled bonds, as well as some possible future trajectories.

First, as demonstrated by the rapid growth in green bond volumes and diversification in the issuer and investor bases, it is likely that labelled bonds will play an increasingly important role in mobilizing financing needs. This is not only in response to the covid-19 pandemic, but also in the longer-term, in response to the impact of climate change.

Much has been written about human-induced global warming and how this affects the climate system.32 This has been increasingly recognized in the financial sector. A watershed moment in this respect was the speech given by the then Governor of the Bank of England and Chairman of the Financial Stability Board, Mark Carney, in 2015. In his speech, titled “Tragedy on the Horizon”, Carney observed that: “With better information as a foundation, we can build a virtuous circle of better understanding of tomorrow’s risks, better pricing for investors, better decisions by policymakers, and a smoother transition to a lower-carbon economy. By managing what gets measured, we can break the Tragedy of the Horizon”.33

For many reasons, including increasing government, public and investor awareness of climate change, green bonds are likely to continue to be issued in increasing volumes by an increasingly diversified issuer base. This is a

In addition, a second meaningful development to look out for relates to the rise of esg considerations and the important role played by investor activism in that regard. As the World Bank’s first green bond showed, investor demand has from early on driven the development of labelled bonds. Strong investor demand is appealing to market newcomers who take full advantage of it. For instance, in October 2020, the European Commission’s first social bond (eur 17 billion issued) was 13 times oversubscribed.34 This insatiable investor demand reflects the increased efforts of the global community towards addressing the impacts of climate change and the increased appeal of financings for investments providing esg benefits. Hence it is not only states, supranational organizations and mdbs, but also institutional investors – including large asset managers – that are increasingly incorporating esg-related considerations into their investment decisions and channelling growth in sustainable financing.

esg has emerged as a core concept in defining sustainability, and there are now a wide range of industry-supported sustainability initiatives that link esg with financing. These include the Global Impact Investing Network,35 the Equator Principles36 and the Principles of Responsible Investment.37 In relation to bonds specifically, icma has noted that Sustainability-Linked Bonds aim at furthering the key role that debt markets can play in funding and encouraging issuers that contribute to sustainability from an esg perspective.38 Hopefully, the enhanced focus on esg considerations will further drive investor preference toward sustainable financing and impact investing, including labelled

A third major trend that is expected to continue is the role taken by mdbs in the development of the labelled bond concept and the stimulation of the labelled bond market. In this respect, it is important to note that mdbs are not only issuers, but also investors, including in labelled bonds. For example, nib has allocated eur 500 million in liquid assets for investments in green bonds, social bonds, sustainability bonds and sustainability-linked bonds issued by companies or municipalities in nib’s member countries. These investments are used to finance environmentally sustainable projects that can contribute to mitigating climate change and achieve positive social outcomes in the Nordic-Baltic region. This, in turn, contributes to nib fulfilling its mandate.39

In addition, researchers have argued that mdbs can be seen as “norm entrepreneurs” in light of their role as a – perhaps the – key catalyst in the development of sustainable banking norms and practices.40 This “entrepreneurial spirit” can be observed clearly in the role that mdbs have played in the development of the labelled bond concept. Indeed, the Addis Ababa Action Agenda encouraged mdbs to play their role by developing financial instruments – including green bonds, and by extension labelled bonds more generally – to direct the resources of long-term investors towards sustainable development.41 The various ways in which mdbs are in fact achieving this goal has been explained above.

Furthermore, the measuring, tracking and reporting on the impact of bonds is now established market practice even where there is no legal obligation to do so. One striking example of thought leadership in this respect is the World Bank Sustainable Development Bonds and Green Bonds Impact Report (earlier the “Green Bond Impact Report”) which includes dedicated chapters for sustainable development bonds and green bonds and presents results highlights, issuance, commitment and allocation figures.42 The Report is widely respected by the industry – as well as other mdbs – as a useful reference point and benchmark for impact reporting standards. This shows that mdbs are

The fourth development we wish to highlight regarding the future of labelled bonds is the emergence of Sustainability-Linked Bonds. A key development in this regard is the publication by icma of its Sustainability-Linked Bond Principles. In a nutshell, the idea behind this type of labelled bonds is that their financial performance should be a function of whether the issuer succeeds in achieving predefined sustainability/esg objectives.43 This type of bond is “forward looking”, and is a performance-based instrument where an issuer commits explicitly to future improvements in sustainability outcome(s) within a set timeline. Sustainability-linked bonds represent a fascinating development from a legal perspective, perhaps foreshadowing a shift in focus away from use of proceeds to an analysis of the performance and/or impact of a business or other relevant entity.

One key legal question concerns the consequences of an issuer not achieving the predefined goals in terms of bond performance and default. If an issuer does not achieve its targets, the bond will specify the consequences. As the Sustainability-Linked Bond Principles provide: “The cornerstone of a slb is that the bond’s financial and/or structural characteristics can vary depending on whether the selected kpi(s) reach (or not) the predefined spt(s), i.e. the slb will need to include a financial and/or structural impact involving trigger event(s)”.44

The usual main consequence is a higher interest rate and hence higher coupon yield. In situations where the bond’s targets cannot be satisfactorily observed, the Sustainability-Linked Bond Principles note that fallback mechanisms should be included.45 Potential exceptional or extreme events – such as drastic changes in the regulatory environment that could substantially impact the calculation of the kpi – should also be explained in the bond documentation.46 Otherwise, generally speaking, there are no other adverse contractual consequences – for example, breach of covenant – for the issuer not achieving the bond’s goals. This similarly holds for event of default; to the author’s best knowledge, no mdb issue has ever used the concept of “esg default”.

Sustainability-linked bond issuance remains novel and niche but is likely to grow. In late 2020, the European Central Bank (ecb) decided that sustainability-linked bonds would be eligible as collateral for Eurosystem credit operations, and also for Eurosystem outright purchases for monetary policy purposes.47 In making this decision, sustainability-linked bonds were given legitimacy as a discrete form of instrument and, more broadly, signaled clearly to the market the EU’s strong and growing support for sustainable finance. mdbs, given their mandates and expertise, are uniquely placed to finance environmentally sustainable projects funded by sustainability-linked bonds. In this respect, the role of mdbs in moving forward innovation and regulation remains central and should be encouraged. For example, from 2021 onwards, nib is one of the coordinators of the Working Group on Sustainability-Linked Bonds.

A fifth future prospect relates to the significance of major European Union regulatory initiatives. The EU’s “Green Deal” of December 2019 underlined the need for long-term signals to direct financial flows to green investments. The Taxonomy Regulation, which entered into force on 12 July 2020, represented a significant development as it establishes a common set of criteria for determining whether an economic activity qualifies as environmentally sustainable.48 The Taxonomy Regulation establishes six environmental objectives, including climate change mitigation and climate change adaptation.49

The Taxonomy is still in its infancy and its legal consequences for labelled bond issuance continue to evolve quickly. Taking green bonds as an example, the EU Commission has announced the establishment of a voluntary EU Green Bond Standard open to all issuers of green bonds, including to mdbs. A core requirement of the proposed framework will be Taxonomy-alignment—that is, funds raised by the bond should be allocated fully to projects that are aligned with the EU Taxonomy. The other key elements are transparency on how the bond proceeds are allocated, external review to ensure compliance with the Taxonomy Regulation, Taxonomy-alignment of the funded projects and supervision by the European Securities Markets Authority of reviewers.51

In light of the Taxonomy and related laws, it can be expected that mdbs issuing green bonds (and other relevant bonds) in the EU will address Taxonomy-alignment in their bond issuances. The eib’s initiatives in this respect provide an illustrative case study. In late 2020, the eib’s Board of Directors approved the Climate Bank Roadmap 2021–2025 outlining the eib’s goals for climate finance that support the European Green Deal.52 The Climate Bank Roadmap provides that the eib aims to align its tracking methodology for green finance with the EU Taxonomy and reflect the alignment to capital markets through an extension of the eligibility criteria for Climate Awareness Bonds and Sustainability Awareness Bonds.53 The Roadmap also aims to align those bonds over time with the proposed EU Green Bond Standard, and the

6 Conclusion

There are a variety of labelled bonds that have quickly emerged on the debt capital markets. Labelled bonds have a critical and possibly under-appreciated role to play in financing a sustainable response to, and recovery from, the pandemic, as well as a transition to a lower-carbon future. mdbs have and will play a central role in driving the innovation, growth and diversification of labelled bonds. Green and other labelled bonds are important tools to finance responses to climate change risks, which remain the greatest risks in the longer run. When the pandemic ends, the international community must be prepared to re-build and mdbs have a key role to play in financing the recovery, and further on the horizon, in financing long-term responses – including major infrastructure projects – to climate change. mdbs have and will continue to play a key role in international debt capital markets by contributing to guiding regulatory developments and in setting high standards for other (labelled) bond issuers.

General Counsel and Head of Legal, Nordic Investment Bank, heikki.cantell@nib.int.

In this article, “multilateral development bank” is given a broad meaning and includes international financial institutions (ifis), such as the Nordic Investment Bank, and other related multilateral entities engaged in cross-border project financing. Some mdbs, such as the European Investment Bank, can arguably be considered to be both an investment bank and a global development bank.

European Bank for Reconstruction and Development ‘ebrd Shareholders and Board of Governors’, <

For an overview of the main global, regional, and sub-regional mdbs, see Delikanli, Dimitrov and Agolli 2018.

The terms “themed”, “thematic” and “labelled” are synonymous. For the purposes of simplicity and consistency, in this article, “labelled” bonds will be used.

As Maltais and Nykvist note: “Despite significant growth there has to date been very little academic research on green bonds”: Maltais and Nykvist 2020, 2.

World Bank, ‘10 Years of Green Bonds: Creating the Blueprint for Sustainability Across Capital Markets’,<

European Investment Bank. ‘Climate Awareness Bonds’, <

World Bank, ‘10 Years of Green Bonds: Creating the Blueprint for Sustainability Across Capital Markets’,<

Ibid, pp. 2–3.

Climate Bonds Initiative, ‘Record $269.5bn green issuance for 2020: Late surge sees pandemic year pip 2019 total by $3bn’, <

cicero’s ‘Shades of Green’ methodology provides information on how well a green bond aligns with a low-carbon resilient future. The two other lower grades are Light Green and Medium Green. For more, see cicero. ‘Shades of Green: Green Bonds’, <

Nordic Investment Bank 2020, ‘nib sek 1.5 billion 5-Year Nordic-Baltic Blue Bond’, <

Environmental Finance 2020, ‘Award for innovation – use of proceeds (green bond) – Nordic Investment Bank’, <

African Development Bank 2017, ‘Social Bond Framework’, <

World Bank, ‘ibrd Funding Program’, <

World Business Council for Sustainable Development 2021, ‘Enel successfully places a triple-tranche 3.25 billion euro sustainability-linked bond in the eurobond market, the largest sustainability-linked transaction ever priced’, <

Crédit Agricole cib Sustainable Banking (As of 20 November 2020); excludes Sustainable Development Bonds which are not icma compliant; percentages in graph refer to bonds in eur (ex-gov).

bbc, Covid map: Coronavirus cases, deaths, vaccinations by country, <

ceb 2020, ‘ceb issues second covid-19 Social Inclusion Bond’, <

nib 2020, ‘nib Response Bond Framework’, <

Ibid, at p.3.

icma, ‘Q&A for Social Bonds related to Covid-19’, <

Ibid.

ifc 2020, Social bonds: Illustrative use-of-proceeds case studies: Coronavirus, <

See e.g. Sustainalytics 2020, ‘Responding to covid-19 through Social Bonds’, <

nib 2020, ‘nib Response Bond Framework’, <

See e.g. Berensmann et al. 2018.

See e.g International Panel on Climate Change (ipcc), Chapter 3, <

European Commission 2020, ‘eur 17 billion EU sure social bond listed on LuxSE’, <

The Global Impact Investing Network, ‘compass: The Methodology for Comparing and Assessing Impact’, <

The Equator Principles 2020, <

The Principles of Responsible Investment, ‘About the pri’, <

International Capital Markets Association 2020, ‘Sustainability-Linked Bond Principles’, <

Nordic Investment Bank, ‘Investments in labelled bonds’, <

Mendez and Houghton 2020, 12; 972.

United Nations Inter-agency Task Force on Financing for Development, ‘Multilateral developmentbanks’,<

World Bank, ‘World Bank Impact Report: Sustainable Development Bonds and Green Bonds’, <

As defined in icma in the Sustainability-Linked Bond Principles: Voluntary Process Guidelines2020,<

Ibid.

Ibid.

European Central Bank 2020, ‘ecb to accept sustainability-linked bonds as collateral’, <

Regulation (EU) 2020/852 of the European Parliament and of the Council of 18 June 2020 on the establishment of a framework to facilitate sustainable investment, and amending Regulation (EU) 2019/2088.

The four other objectives are: Sustainable use and protection of water and marine resources; the transition to a circular economy; pollution prevention and control; and the protection and restoration of biodiversity and ecosystems: European Commission, ‘EU taxonomy for sustainable activities’, <

See European Commission, ‘Platform on sustainable finance’, <

European Commission, ‘European green bond standard’, <

eib, ‘The eib Group Climate Bank Roadmap 2021–2025’, <

eib, ‘Climate Awareness Bonds’, <

Ibid.

References

Environmental Finance 2020, ‘Award for innovation – use of proceeds (green bond) – Nordic Investment Bank ’, <https://www.environmental-finance.com/content/awards/green-social-and-sustainability-bond-awards-2020/winners/award-for-innovation-use-of-proceeds-(green-bond)-nordic-investment-bank.html>,accessed21 October 2021.

The Equator Principles, (July 2020), <https://equator-principles.com/wp-content/uploads/2021/02/The-Equator-Principles-July-2020.pdf>, accessed 21 October 2021.

International Finance Corporation (ifc), Social bonds: Illustrative use-of-proceeds case studies: Coronavirus, (March 2020), <https://www.ifc.org/wps/wcm/connect/3d1ccd21-ad12-4468-b03d-251cd6421bc5/SB-COVID-Case-Study-Final-30Mar2020-310320.pdf?MOD=AJPERES&CVID=n4RsBEk>, accessed 21 October 2021.

Ketterer J A, Andrade G, Netto M, and Haro M I, Transforming the Green Bond Market. Inter-American Development Bank, (2019), <https://publications.iadb.org/publications/english/document/Transforming_Green_Bond_Markets_Using_Financial_Innovation_and_Technology_to_Expand_Green_Bond_Issuance_in_Latin_America_and_the_Caribbean_en.pdf>, accessed 21 October 2021.