Abstract

Frequent and long-lasting extreme climate events can impact business-related natural capital, severely affecting production and resulting in losses for agricultural firms. Physical climate effects are material dependencies for agricultural businesses and may severely affect their performance and compromise their survival. This studyâs aim is to analyze the comprehensive effect of climate change factors on agricultural firm bankruptcies in a European geographical area that is especially susceptible to climate change. Employing a panel of 15 036 agricultural firms, we analyze the effects of adverse climatic conditions in the firmâs headquarters area using logit regressions, an instrumental variable ordinary least squares model, and the gradient-boosting ensemble method. We find that bankruptcy is conditioned upon extreme weather events, indicating that climate changeâs physical impacts on firm resources already materially affect the agricultural sectorâs resilience and survival. Specifically, abnormally high temperatures, precipitation, and the incidence of fires are significant factors that contribute to bankruptcy or insolvency. Furthermore, a âfire weatherâ index comprising high temperatures, drought, and wind, combined with fire occurrence, intensifies the bankruptcy risk of agricultural businesses.

1. Introduction

The temperature and precipitation trends analysis shows that climate change is visible worldwide, and its effects are expected to intensify in the coming years (Coronese et al., 2019; Grillakis, 2019; Romilly, 2007; Teuling, 2018). European financial institutions (EIB, 2021; EIOPA, 2022) and research studies (Forino and von Meding, 2021; Gasbarro et al., 2017; Hsiang et al., 2017; Linnenluecke et al., 2013; Winn et al., 2011) recognize that physical climate change risks require adaptation by institutions, businesses, and society to reduce vulnerability, moderate damage, and alleviate adverse effects. In the European context, the IPCC (2021) report shows that Mediterranean countries are experiencing more extensive and longer agricultural and ecological droughts combined with floods from extreme rainfall. In addition to droughts and floods, a broad study performed by the EIOPA (2022) among European insurers identifies wildfires as one of the most dangerous and potentially disruptive risks in southern Europe from a current and forward-looking perspective. As wildfires are prevalent in rural areas, this study shows that most property and assets destroyed by wildfires belong to firms and agricultural businesses. Our study focuses on this Mediterranean area, mostly within southern Europe.

Climate change is the origin of critical changes in the natural capital used in agriculture, constituting strong dependencies. The resulting changes in consumptive natural capital range from the desiccation of the soil surface and freshwater, as well as damage/destruction of raw materials (grain and other harvests, trees) (Natural Capital Coalition, 2016b), to the deterioration or destruction of property, plant, and equipment (Monasterolo, 2020). The consequences of climate change dependency on the agricultural business are the increase in operational costs to access alternative freshwater and raw materials, loss of revenue from crops, reparation costs, and rebuilding investments, and even compromising the firmâs resilience and survival in the most severe cases (Natural Capital Coalition, 2016b).

The main objective of this study is to analyze the comprehensive effect of climate change factors on firm bankruptcy for agriculture, a sector of particular concern in the European Mediterranean area, a geographical zone especially susceptible to climate change. Specifically, our study aims to measure how anomalies in maximum temperatures and precipitation as well as fires affect agricultural firmsâ next-year bankruptcy risk. We focus on agricultural firms in France, Italy, Spain, and Portugal from 2016 to 2019, using logit regression as the main methodology for our empirical testing.

To date, a limited number of studies have integrated environmental risk into credit risk management performed by financial firms (Coulson, 2009; Labatt and White, 2002; Mengze and Wei, 2015; UNEP FI, 2007; Weber, 2012, 2005; Weber et al., 2008, 2010; White, 1996). Specifically, studies focusing on the effect of physical risks associated with climate change on credit are still incipient and more limited in number. Calabrese et al. (2023) investigate the impact of extreme weather events, such as heavy rains and tropical cyclones, on mortgage default and prepayment probabilities. Ouazad and Kahn (2021) examine how tropical cyclones affect lendersâ behaviour in the mortgage market. And Berger et al. (2023) document that US bank holding companies suffer more operational losses during extreme storms, being business disruption and damage of physical assets relevant drivers of these losses. However, previous studies addressing physical climate risk in credit risk management have devoted very little or no attention to wildfires.

To fill this void, this study analyzes individual climate factors, such as excess rainfall and periods of abnormally high temperatures; we find that these factors negatively influence firm health. This result is consistent with the very limited previous findings (Griffin et al., 2019; Nguyen et al., 2023) and the dependency of agricultural resources and resilience on climate conditions. Furthermore, this study explores an element of climate change that has not been previously analyzed as an inductor of financial health deterioration. To this end, we investigate wildfire effects on the agricultural business, which requires the joint impact of several climate factors: drought, high temperatures, and wind as the main inductors. According to our results, bankruptcy risk significantly increases for firms in areas affected by extremely high temperatures and rainfall, and also for firms in the area of influence of wildfires. The combination of these three climatic factors (drought, high temperatures, and wind) aggravates the negative effect of wildfires on firmsâ financial health. These results highlight the importance of studying geographical areas with specific climatic conditions and risks, suggesting that the influence of climatic factors is not straightforward. In the European Mediterranean area, mostly placed in southern Europe, excess rainfall causes floods, a negative factor for agricultural production; however, scarce rainfall is the main inducer of droughts and a relevant climatic factor for wildfire risk.

This study contributes to the existing literature in several ways. First, it extends the emerging stream of research on the relationship between the physical effects of climate change and bankruptcy risk by establishing how this relationship affects the agricultural sector in the European Mediterranean area. Second, to the best of our knowledge, this is the first empirical study to analyze the effects of wildfires and their accentuated impacts in the presence of specific climatic conditions that climate change aggravates. Finally, our work links theoretical frameworks at two levels: at the agricultural firm level, the resource-based and resilience theories explain where and how firmsâ financial health is affected by physical climate risks. However, their application cannot quantify these risks individually. At the agricultural stakeholder level, the credit risk management theory incorporates financial environmental risks, including physical effects derived from climate change. It quantifies the risk for the concerned industries in broad geographical areas where these physical climate risks are endemic. The financial risk to agricultural businesses derived from climate change has implications for policymakers, regulators, investors, companies, and civil society (Caldecott, 2017; IRENA, 2017). In the case of financial firms, both creditors and insurers (Natural Capital Coalition, 2016c) are concerned about the deterioration of natural capital, which reduces income and increases costs, thus hampering the firmsâ capacity to repay credit and deteriorating their capital investment, which results in collateral abatement (ESRB, 2016).

2. Theoretical framework

The theory of financial environmental risk is a complex framework comprising three blocks (Gutiérrez-López et al., 2022): the transition costs to low-carbon production (LCP), which can be considered of systemic relevance in the European setting (Cahen-Fourot et al., 2019), firmsâ danger of being unsustainable once a low-carbon economy is reached (Caldecott and Dericks, 2018), and the already experienced or potential climate-induced physical damage to firmsâ capital (Romilly, 2007), which is the object of this study.

The physical impacts of climate-related risks are classified by European financial institutions (EIB, 2021; EIOPA, 2022) as acute risks (extreme weather events) and chronic risks (gradual global warming) and are expected to become the most prominent environmental hazards. Primary production sectors such as agriculture are strongly affected by their high dependence on natural capital (Ascui and Cojoianu, 2019).

To analyze the impact of physical risks from climate change on agricultural sector firms, this study establishes a necessary connection between the standpoints of firmsâ and their stakeholders.â From the firmsâ perspective, two theoretical approaches play a role in explaining how firmsâ financial health is affected: the resource-based theory and the resilience theory. The resource-based theory states that a firm obtains a competitive advantage by exploiting its productive resources when imitation is challenging and generates valuable capabilities (Barney and Clark, 2007; Berrone et al., 2013). Therefore, according to this theory, the direct effect on agricultural firmsâ resources negatively impacts firm performance. Physical climate risks can damage or destroy productive resources (natural capital, a firmâs physical assets, and even human capital health) (Monasterolo, 2020) to such a significant extent that a firmâs survival can be compromised. Hence, we resort to resilience theory to complete the proposed theoretical framework. In this theory, resilience is defined as the capacity shown by an organization or a system to face disruptions and persist after negative shocks (Annarelli and Nonino, 2016).

Concerning the firmâs resilience, business adaptation to the physical effects of extreme weather events has been mostly reactive due to their inability1 to predict changes and variability in climate at their locality, as well as expected impacts on their resources and activities and translation into costs and benefits (Berkhout, 2012; Winn et al., 2011). Adaptation is also conditioned by a firmâs sense-making and learning processes related to climate change (Gasbarro and Pinkse, 2015; Zhang, 2022), with culture, institutions, information, and financial restrictions being as much of a determinant as costs and benefits.

Recent studies (Clement and Rivera, 2017; Linnenluecke et al., 2012; Winn et al., 2011) have expanded resilience theory to consider extreme weather events. Thus, firms advance from adaptation to transformative change to cope with adaptation limits as extreme weather events become more frequent and intense due to climate change. The adaptation process should allow the firm to recover and return to its original operational regime; however, when adaptation limits are surpassed, two other trajectories emerge: a new operational regime or cease of operations (Clement and Rivera, 2017).

From the stakeholdersâ perspective, this study builds on the theoretical exploration made by Ascui and Cojoianu (2019) of how natural capital credit risk assessment may be articulated in agricultural lending.

Evaluating physical climate risk has become increasingly critical for financial institutions, with significant implications for their operations and financial performance (EIB, 2021; EIOPA, 2022). Financial firmsâ resilience depends on how they measure the effect of the physical climate risk on the valuation of assets and clientsâ credit risk profiles. Therefore, regulators worldwide are increasingly focusing on climate risk, and financial institutions may be required to disclose their climate risk exposure and incorporate climate risk into their risk management processes. For instance, in February 2024, the European Central Bank (ECB) published its final revised guide to internal models. This updated version recommends the inclusion of material climate-related and environmental risks in banksâ models. Non-compliance can result in regulatory penalties and reputational damage (Fabris, 2020).

This study addresses the need to incorporate physical climate risks into assessment methods to serve financial institutionsâ credit management (Georgopoulou et al., 2015). Specifically, we integrate climate risks into the credit risk assessment for agricultural businesses in the four largest countries of the European Mediterranean area, a geographical area susceptible to climate change.

In line with Ascui and Cojoianu (2019), we adopt a lenderâs perspective when considering climate-derived physical risk. The reason alluded to by resilience theory is the low chance of recurrence for a particular community and certain firms; hence, the low chance of recurrence is a reason for firms to only adopt reactive occasional measures (McKnight and Linnenluecke, 2019; Zhang, 2022). In contrast, lenders offer credit to wider geographical areas (normally countrywide), and are very likely to be affected by some adverse effects of physical climate risk if the lenderâs area of influence is endemically affected by climate risks, as countries in the Mediterranean area and southern Europe are in the period under analysis.

3. Research hypotheses

Since specific by-industry attributes may be critical to a successful and effective response to the physical impacts of climate change (Linnenluecke et al., 2013), we focus on the effects of climate change on agricultural business. Let us consider operational disruptions requiring agricultural production adjustments for achieving business resilience. In the primary sectors, acute risks, such as extreme temperatures, droughts, and floods, cause issues in accessing water for irrigation, a negative effect on crop growth, loss of grain and other harvests (raw materials), degradation of fertile soil, and deterioration of livestock health and welfare, resulting in higher mortality rates, lower productivity, and deterioration of immobilized productive capital (property, plant and equipment) (Ascui and Cojoianu, 2019; Grillakis, 2019; Monasterolo, 2020). Therefore, according to the Natural Capital Protocol, climatic factors are classified as dependencies on the agricultural sector (Natural Capital Coalition, 2016b).

Heat, lack of air humidity, derived desiccation of the soil surface, and strong winds work to intensify and extend a specific disaster type, wildfires (Sutanto et al., 2020). Fires can incinerate crops, devastate irrigation systems, and damage infrastructure, resulting in substantial losses for farmers and the agricultural sector. Another repercussion of agricultural fires is the degradation of fertile soil (Monasterolo, 2020). Fires can induce soil erosion and diminish its nutrient content, rendering it less adaptable for crop cultivation.

Consequently, the compound extreme event of wildfires must be regarded as a determinant of potential future losses and bankruptcy, critical factors in the climate resilience of agricultural firms.

The question of interest is how to integrate these dependencies into credit risk management or the recently developed environmental credit risk management (ECRM) (UNEP FI, 2007). The risk assessment process comprises the following stages: identification, analysis, categorization, mitigation, and monitoring. To advance the stages of identification and analysis, we propose specific quantitative variables referring to extreme conditions of temperature, precipitation, and wind, as well as wildfires, to measure the physical climate change risk with damaging effects on agricultural resources. We hypothesize that they have a material effect on firmsâ next-year bankruptcy probability, which is obtained through logistic regression. Thus, when climatic factors (anomalies in maximum temperatures and precipitation, fires, and fire weather conditions) have a positive effect, the value of the dependent variable increases. The dependent variable ranges between 0 and 1, indicating a firmâs probability of bankruptcy from 0% to 100%.

H1. Physical climate change factors exert a material effect on firmsâ bankruptcy risk

H1a. Anomalies in maximum temperatures exert a material positive effect on firmsâ bankruptcy risk

H1b. Anomalies in maximum precipitations exert a material positive effect on firmsâ bankruptcy risk

H1c. More frequent fires exert a material positive effect on firmsâ bankruptcy risk

H1d. Fire weather conditions exert a material positive effect on firmsâ bankruptcy risk

4. Research design

The proposed model aims to uncover the crucial financial and climatic risk factors determining a companyâs bankruptcy or insolvency within the following 12 months. The studyâs objective is to pinpoint the drivers of company distress, considering not only individual financial ratios but also climate-related variables, particularly those concerning physical risks.

The choice of companies, countries, and years analyzed is meticulously considered. This study primarily targets companies operating in the agricultural sector, including crop and livestock production, where the effects of climate change are particularly pronounced. Agricultural businesses are susceptible to temperature, precipitation, and other climatic fluctuations because they are highly dependent on natural capital (Ascui and Cojoianu, 2019).

4.1. Sample and data description

The present studyâs financial data are sourced from the ORBIS dataset provided by Bureau van Dijk (BvD). Agricultural firms in Portugal, Spain, Italy, and France2 with available financial data from 2016 to 2018 have been extracted. These selection criteria ensure the use of the most recent available financial data until 2019 for any firm under consideration. The selection of these countries is informed by an IPCC (2021) report, which highlights that Mediterranean countries are experiencing more extensive and prolonged agricultural and ecological droughts juxtaposed with floods resulting from extreme rainfall. Consequently, these countries encounter pronounced extreme weather events and wildfires within the timeframe of this study.

The years selected for this analysis are particularly significant, as they represent economically stable periods in Europe from a macroeconomic perspective. This choice mitigates the influence of bankruptcy that may arise from a more significant economic downturn. For example, although data from 2020 and 2021 may technically be incorporated, these years are predominantly overshadowed by the global implications of the COVID-19 pandemic. As such, discerning whether a firmâs bankruptcy arises due to the pandemic, inherent financial vulnerabilities, or specific factors such as climate-induced risks may become fuzzier.

Furthermore, the years selected for this study strive to strike a balance between historical depth and representativeness and validity of the data. Given the recent surge in global temperatures and escalation of extreme weather events, it is paramount to consider contemporary climatic influences on businesses. Factoring data from distant years may jeopardize the studyâs conclusions, as the economic characteristics of firms during those periods may differ substantially from those of more recent years.

The sample comprises 15 036 companies from four countries. At 41.22% of the total, the highest proportion is from Italy, followed by Spain (38.77%), Portugal (11.34%), and France (8.67%). These firms are categorized as either âdistressedâ or âhealthy.â A company is deemed a âfailedâ if its financial statements for the year are accessible and one of the following statuses is observed within the next 12 months: rescue plan, insolvency proceedings, payment suspension, dissolved, or bankruptcy. This selection criterion ensures the use of the most recent available financial data until 2019 for any firm under consideration. Italy ranks first in terms of bankrupt firms, at 59.15%, followed by Spain (18.60%) and France (16.46%). Portugal has the lowest proportion of distressed firms at 5.79%. Notably, this approach mirrors the strategies employed by financial institutions in their efforts to predict default. Such strategies allow them a margin of manoeuvrability to pre-empt potential bankruptcy or non-payment issues. This approach also aligns with the Basel IV regulations emphasizing banking stability. Based on this criterion, 458 firms are considered to have failed.

Financial information has been extracted from Orbis. The selected accounting-based variables are profitability, long-term debt, short-term liabilities, liquidity, tangibility, size, and activity. Return on assets (ROA) is calculated as the ratio of net income to total assets. Long-term debt (LONG_DEBT) is expressed as the ratio of long-term financial debt to total assets. Short-term liabilities (SHORT_LIAB) are calculated as the ratio of short-term liabilities to total assets. Liquidity (LIQ) represents the ratio of current assets to current liabilities. Tangibility (TANG) is the ratio of fixed assets to total assets. Size (SIZE) is computed as the logarithm of total assets, and the activity variable (ACTIVITY) is calculated as sales growth with respect to the previous year.

Climatic data are sourced from the European Climate Assessment and Dataset Project (ECA&P). The ECA&P aggregates observations from an extensive network of stations across Europe and the Mediterranean region. It boasts records from over 2500 sites detailing daily precipitation patterns and over 1300 sites documenting daily minimum and maximum temperatures. This dataset is one of the most reliable public repositories for daily European weather data. This study also integrates historical data on European wildfires. Wildfire information is derived using Fire Event Delineation for Python (FIREDpy) open-source software. FIREDpy autonomously fetches and refines fire-related data for designated areas and captures metrics, such as the number of fires, expansion of the burned area, duration, and other pertinent parameters. It is worth mentioning that although financial information of explanatory variables is limited to the years 2016 to 2018, climate-related metrics consider data from the last 10 years; therefore, the period covered is quite extensive.

The maximum temperature and precipitations anomalies (MAX_TEMP and PRECIPI respectively) represent the difference between the highest temperature/precipitations recorded in a given year in the location of the company and the average of the maximum temperature/precipitations over the preceding decade. FIRES measures the number of fires in the last 5 years within a 100 km radius of the firmâs location. In addition, a Climate Index is calculated by extracting the first principal component of the three most influential variables in the initiation and propagation of fires (CLIMATE_INDEX). The maximum temperature, drought, and wind (IPPC, 2021; McKnight and Linnenluecke, 2019; Turco et al., 2014) are used. Drought is assigned a value of one if the mean rainfall value for April, May, June, July, August, and September is below the first tercile of the average annual rainfall, and zero otherwise. The wind is calculated as the anomaly in the mean wind speed observed in the last 5 years compared to the historically available data.

Linking climate variables to individual companies is considerably more challenging, especially compared with the more straightforward process of assigning financial metrics. This difficulty is primarily due to the need to accurately identify the operational locations of these companies. For larger corporations, gathering detailed information on their main production sites and key assets may not always be feasible. In addition, the available data may not always be reliable. The current study focuses on small to medium-sized enterprises (SMEs) in response to this issue. The location of an SMEâs headquarters is often easy to find and usually provides a good indication of its primary asset location, as supported by Griffin et al. (2019). This concept is based on the view that smaller companies tend to operate in specific areas. When adding climatic factors for each company, considering the companyâs distance from relevant data sources, such as weather stations, is essential. For example, if a company is close to several weather stations that record temperature data, the readings from the nearest station are assigned to that company.

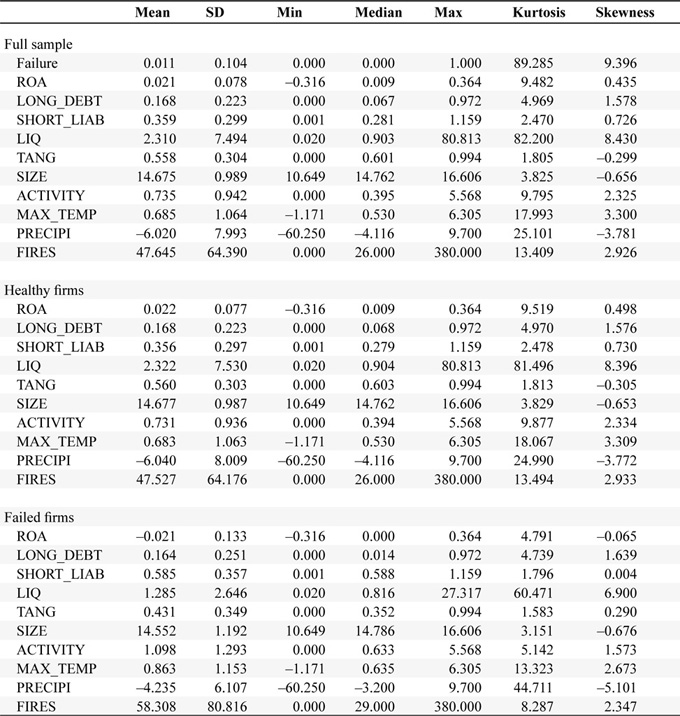

Table 1 presents the summary statistics of the variables included in the model for the full sample, healthy firms and failed firms. Panel A reports that, on average, the overall failure rate is 1.1%, ROA is 2.12%, and leverage shows a high rate of short-term liabilities (35.87%) in contrast to long-term financial debt (16.78%). Comparing Panels B and C, failed firms show negative ROA and lower liquidity and tangibility. The higher proportion of short-term liabilities is consistent with this faster way of obtaining funds when a decrease in profitability limits the available liquidity. The variable descriptive statistics include average, minimum, median, and maximum values, as well as standard deviation, kurtosis, and skewness.

Descriptive statistics.

Citation: International Food and Agribusiness Management Review 28, 1 (2025) ; 10.22434/ifamr1170

Figure 1 reports the mean values of the climate factors used by the firmâs category of financial health. In all cases, failed firms are located in areas that suffered severe climate conditions, indicating a negative effect of these extreme climate events (rainfall anomalies, anomalies in maximum temperatures, and the number of fires around the firm) on the firmâs financial health.

Climate variables by firmâs financial health. The definitions of the variables are given in Table A1 in the Appendix.

Citation: International Food and Agribusiness Management Review 28, 1 (2025) ; 10.22434/ifamr1170

4.2. Models

In the proposed model, the dependent variable is a dummy variable that equals one if the company is considered failed, and zero otherwise. This model incorporates the financial and climate-related variables previously described as explanatory factors. The seven selected financial information variables have been extensively employed in the literature as proxies for a firmâs financial health (Atif and Ali, 2021; Charalambakis and Garrett 2019; Crutzen and Van Caillie, 2010; Du Jardin, 2010; Tian et al., 2015). Thus, the baseline model (1) explains the firmâs probability of bankruptcy in a certain year based on several explanatory variables that capture different relevant aspects of the prior yearâs business performance and resilience.

Regarding climate risk, there is a well-documented rise in extreme weather events globally, which have had notably devastating effects in temperate zones and significant economic repercussions on agriculture (Coronese et al., 2019). In our selected countries â France, Italy, Portugal and Spain â the intensification of temperatures above the global average, along with substantial variability and a general decrease in precipitation levels, presents an important challenge to the sustainability of agricultural activities (IPCC, 2021). Indeed, the escalating trend in temperatures and the increasing frequency of severe droughts across Europe are expected to continue, directly threatening the viability of agricultural activities (Sutanto et al., 2020; Teuling, 2018). The situation is aggravated during the summer months by an elevated risk of wildfires, driven by a confluence of extreme heat, drought, desiccation of the soil, and strong winds. These conditions pose imminent threats to crop health, soil fertility, and overall agricultural productivity (Lavalle et al., 2009). Therefore, the baseline model is extended to test the hypotheses posed. Model (2) adds climatic risk (CRP), proxied by three alternative variables (IPCC, 2021, Natural Capital Coalition, 2016a,b): anomalies in maximum temperatures (MAX_TEMP), anomalies in maximum precipitation (PRECIPI), and number of fires (FIRES) to test the general hypothesis (H1) and specific hypotheses H1a, H1b, and H1c. Model (3) simultaneously considers these three proxies of climatic risk to test the three sub-hypotheses more in depth.

Finally, as heat, lack of air humidity, derived desiccation of the soil surface, and strong winds work to intensify and extend wildfires (Sutanto et al., 2020), we incorporate fire weather3 through our constructed climate index. Model (4) includes the joint effect of fires and the occurrence of fire weather to test hypothesis H1d and the moderating effect of climate conditions on initiating and propagating fires.

Citation: International Food and Agribusiness Management Review 28, 1 (2025) ; 10.22434/ifamr1170

A correlation analysis was conducted for the variables included in the model to obtain a first assessment of their possible linear association; the proposed models are estimated using logit regressions for the panel data. Since Ohlsonâs (1980) ground-breaking work, which introduced logistic regression as a powerful tool for predicting corporate failure, this method has remained a cornerstone in bankruptcy prediction research. Logistic regression is widely used due to its ability to directly estimate probabilities, handle multiple financial predictors, and provide easily interpretable coefficients (Barboza et al., 2017). The robustness of logistic regression to non-normal distributions, which are common in financial data, further justifies its use in our study (Sun et al., 2014). Additionally, Liang et al. (2016) highlighted the methodâs flexibility by effectively combining financial ratios with corporate governance indicators, improving predictive power and providing insights into the importance of non-financial factors in bankruptcy prediction.

To validate our logit regression models, we employed several key statistical tests, including the Wald test to assess the significance of individual coefficients. The Lagrange multiplier (LM) was applied to check for potential model specification errors by testing the null hypothesis that additional parameters are unnecessary. The receiver operating characteristic (ROC) curve along with the area under the curve (AUC) was used to measure the modelâs ability to correctly classify bankruptcy cases. Additionally, we employed the likelihood ratio (LR) test to compare the goodness-of-fit between models with different sets of predictors, ensuring that the included variables effectively improve the models. These methods are standard in the literature for validating logit models (e.g., Filipe et al. 2016; Greene, 2017; Long and Freese, 2001).

In addition, in the robustness section we applied the instrumental variable ordinary least squares model, boosting ensemble method, and cross-validation technique to support our results.

5. Results and discussion

5.1. Empirical results

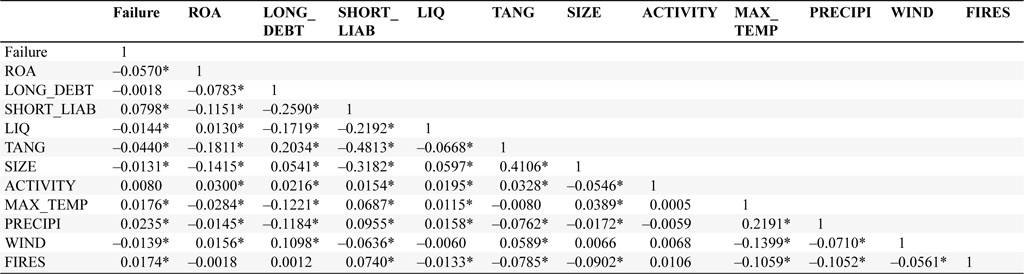

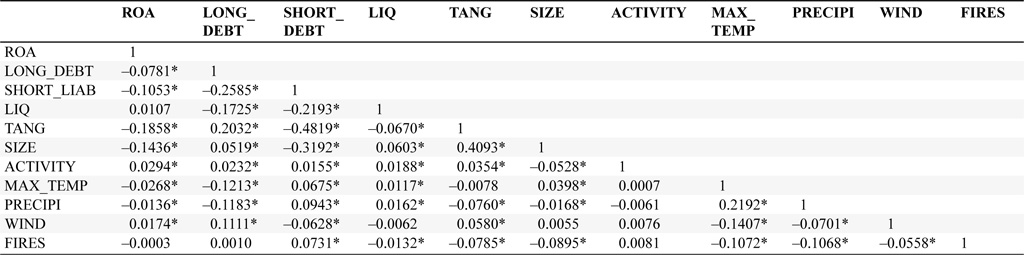

The results of a preliminary correlation analysis considering the full sample, healthy firms and failed firms are provided in Tables A2âA4 in the Appendix.5 All four extreme climatic events show a significant correlation with failure (in the full sample), and the positive signs for temperature, precipitation, and fire support the results shown in Figure 1. The negative correlations between extreme precipitation and fire with tangibility and size are consistent with the deterioration/destruction of firm resources.

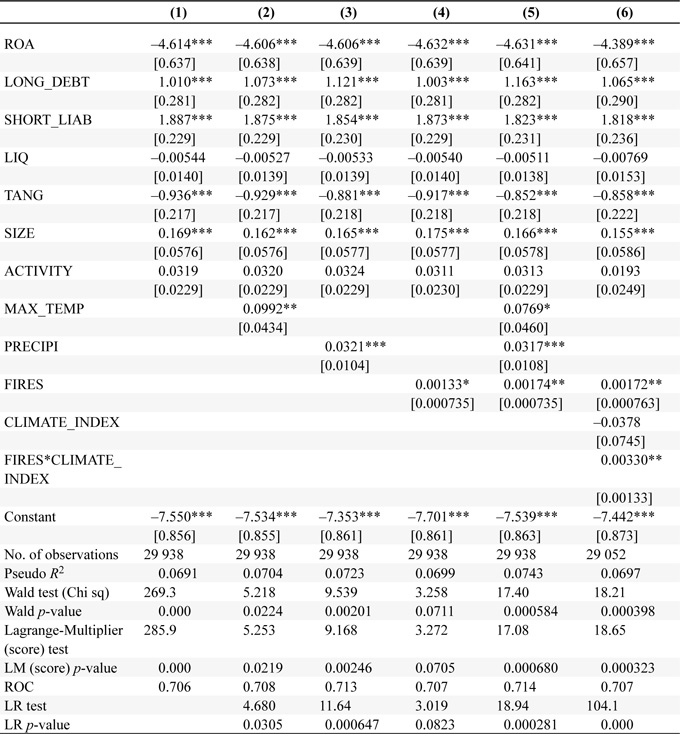

Table 2 presents the results of the logit regressions used to derive the probability of agricultural firm bankruptcy or insolvency based on firm-specific financial variables and geography-specific climate risk factors. The first column shows the results for the baseline model, which only includes well-known financial inductors with effects on firm bankruptcy that have been contrasted in the literature. The next five columns show the results after adding climate risk factors. Extremely high temperatures are added in column 2, extreme precipitation in column 3 and fires in column 4; all four positively and significantly affect the probability of firm bankruptcy. These results align with the damage/destruction of relevant resources from extreme climate events (resource-based theory) and with scarce previous findings on the adverse effects of high temperatures and fire danger on European agriculture (Lavalle et al., 2009).

The effects of climate change on business failure.

Citation: International Food and Agribusiness Management Review 28, 1 (2025) ; 10.22434/ifamr1170

Our results for extreme rainfall are also consistent with those of Calabrese et al. (2023) for heavy rainfall events. Column 5 shows that all three factors maintain their significant effects when jointly incorporated into the model. In column 6, we test the encouraging effect of a âfire weatherâ index to the simple existence of fires close to firms, confirming the relevant role of weather conditions on the incidence of this catastrophe (whether ignited naturally or human-induced), the amplifying effect of combining several climatic factors (IPCC, 2021; Sutanto et al., 2020), and the importance of including wildfires (or just fires) as climate-related physical risks in the aggravating process derived from climate change in the Mediterranean and southern Europe (Lavalle et al., 2009).

5.2. Robustness analyses

To address reverse causality, in Table 3, we present the results obtained by estimating an instrumental variable ordinary least squares (OLS) model that resembles the conventional use of two-step least squares (2SLS). The first four columns show similar results, supporting the validity of our conclusions. However, in this approach, we also consider instrumental variables to study the effect of the number of fires on business failure (column 5). Specifically, we select anomalies in the maximum temperature, anomalies in the mean wind speed, and a proxy of droughts as instruments. The results indicate that if the number of fires is explained by climate variables that act as fire inductors, the positive effect of fires on business failures is stronger.6

The effects of climate change on business failure: two-step least squares.

Citation: International Food and Agribusiness Management Review 28, 1 (2025) ; 10.22434/ifamr1170

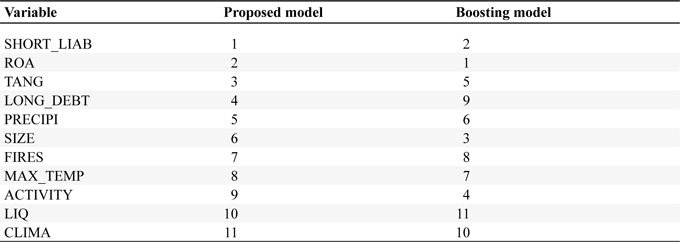

Finally, as a robustness test, we check the rank ordering and importance of the variables derived from our model by comparing them with the well-established gradient-boosting ensemble method (Freund and Schapire, 1996). In machine learning, utilizing an ensemble of distinct classifiers has demonstrated enhanced overall model accuracy. Boosting is a technique that initially acquires a base classifier from an original dataset, modifies the training dataset distribution based on the performance of the base classifier, and subsequently trains the next base classifier using an altered sample distribution. This method allocates weights to each training set, which can be employed to create a collection of bootstrap samples from the initial data.

Boosting is selected as a benchmark because several studies in the bankruptcy literature use ensemble strategies, including boosting, and have corroborated their advantages (Kim and Upneja, 2014; Sun et al., 2014; Wang et al., 2012). Furthermore, boosting can give more importance to features that contribute more to the classification task and are less prone to overfitting than a single and more complex classifier. The importance of the variables in a model is measured as the loss in the modelâs accuracy if a variable is removed from the model, keeping the remaining variables constant. Table 4 lists the importance of the variables used in the boosting ensemble model.

The effects of climate change on business failure: boosting model.

Citation: International Food and Agribusiness Management Review 28, 1 (2025) ; 10.22434/ifamr1170

Overall, the logit/probit and boosting models show relatively similar patterns in ranking variables. Although differences are observed in the specific rankings of individual items, the overall structure and importance assigned to financial and climatic factors are generally consistent between the two methodologies. Only two variables rank differently: long-term debt and activity. These results suggest that both model types capture similar aspects of the underlying data, and their differences can be attributed to the unique characteristics of each method.

Finally, we apply cross-validation (by simulating multiple analyses), which enhances the robustness of our conclusions and provides a more accurate estimate of the modelâs performance across different contexts (Breiman, 1996). This method allows us to test the modelâs stability across various data partitions, ensuring that the results are not influenced by a single dataset split. In non-tabulated results, we check how cross-validation reinforces our initial findings regarding the significance of climate events, making the modelâs predictions reliable and generalizable across diverse contexts and regions.

6. Conclusions

Climate change is the origin of critical effects on natural capital, a significant part of the agricultural production process that constitutes a strong dependency on this sector. In the European Mediterranean area, mostly located in southern Europe, extreme conditions of climatic factors, such as high temperature, heavy rainfall, or lack of it, result in compound extreme events such as droughts and floods. In addition, high temperatures, in combination with lack of air humidity, the derived desiccation of soil surface, and strong wind, are called âfire weatherâ as inductors of fire seriousness. The direct destruction of goods and productive tangible assets, together with the deterioration of natural capital (soil erosion and difficult access to fresh water), severely affects strategic resources for the agricultural business (resource-based theory), producing immediate losses, increased costs, and reduced income. The indirect effects come from the reduced market values of non-damaged assets (reducing collateral value in credit contracts), higher insurance premiums, reduced gross domestic product, and higher rates of unemployment in the damaged area near the agricultural firm, as other firms and citizens (potential clients) also suffer losses in physical capital and significant expenses due to climate disasters.

The risks mentioned above are often underestimated. First, the growing progression of physical climate risks under climate change makes backward-looking data a poor and optimistic proxy for real risk. Second, the low recurrence rate of climatic disasters in the same specific zones induces occasional reactive measures instead of incremental adaptation (resilience theory). However, this should not be the case for financial firms, such as banks or insurance companies, since their area of influence is considerably wider, extending to many firms and clients across one or even several countries, implying that financial firms in areas where climatic disasters become endemic (chronic risk) will suffer their economic consequences.

Given the considerations above, this study adopts a lenderâs perspective to consider climate-derived physical risk and estimate the probability of bankruptcy of agricultural firms in four European Mediterranean countries during 2016â2018. We do not address 2020 and 2021, as the adverse effects of the COVID-19 pandemic may bias them. Considering their geographical proximity to the firmâs headquarters, we assign extreme climatic events to firms, as SMEsâ assets are expected to be concentrated close to and around the head office. For a sample of 15 036 firms, including 458 officially declared bankruptcy or insolvency, our results show that abnormally high temperatures, precipitation, and the incidence of fires are significant factors contributing to bankruptcy or insolvency. Furthermore, a âfire weatherâ index comprising a combination of high temperatures, drought, and wind, in combination with fire occurrence, shows an intensifying effect on the bankruptcy risk of agricultural businesses.

7. Implications and extension of our study

Our results demonstrate that underestimated physical climate risks are material and have a measurable effect on agricultural firmsâ bankruptcy and/or insolvency. The main implications for managers, investors, creditors, insurers, and policymakers emanate from the need to include time and geography as relevant factors in the climate change transition (Nyberg et al., 2022). Both financial systems and public administrations are final contributors of funds to help societies and productive agents cope with the effects of climate physical disasters, thus playing a critical role in climate change adaptation (Dennis, 2022; Forino and Von Meding, 2021) but also suffering economic consequences in their accounts, compromising the financial system and the states financial stability (Klusak et al., 2021) in the most dramatic cases. In line with the UNEP FI (2002) recommendations, coordinated policies are urgently required in key climate-related zones, and our study suggests concerns for the European Mediterranean area with respect to the agricultural sector.

Financial firms, mainly banks and insurance companies, can obtain an additional tool to quantify the incidence of physical climate-derived disasters in agricultural businesses; hence, they can derive probabilities and price the potential impacts of physical climate risks on firmsâ performance, with substantial influence on their loans and insurance terms. Knowledge of industry-wide incidence can help design institutional policies to prompt firms to develop attributes for adapting production to climate physical impacts (Linnenluecke et al., 2013), and climate change adaptation is a relevant contribution to community resilience (McKnight and Linnenluecke, 2019)

Future extensions of this work can incorporate expectations for specific geographical areas regarding the evolution of climatic factors triggering physical climate disasters according to scientific medium- and long-term estimations.

Acknowledgement

This study was upported by Grant PID2021-124950OB-I00 funded by MCIN/AEI/ 10.13039/501100011033 and by ERDF A way of making Europe.

References

Annarelli, A. and F. Nonino. 2016. Strategic and operational management of organizational resilience: Current state of research and future directions. Omega 62: 1â18. https://doi.org/10.1016/j.omega.2015.08.004

Ascui, F. and T.F. Cojoianu. 2019. Implementing natural capital credit risk assessment in agricultural lending. Business Strategy and the Environment 28: 1234â1249. https://doi.org/10.1002/bse.2313

Atif, M. and S. Ali. 2021. Environmental, social and governance disclosure and default risk. Business Strategy and the Environment 30(8): 3937â3959. https://doi.org/10.1002/bse.2850

Barney, J.B. and D.N. Clark. 2007. Resource-based theory: Creating and sustaining competitive advantage. Oxford University Press, Oxford.

Berger, A., F. Curti, N. Lazaryan, A. Mihov and R. Roman. 2023. Climate risks in the U.S. banking sector: Evidence from operational losses and extreme storms. Federal Reserve Bank Philadelphia Research Paper 23-31. Federal Reserve Bank, Philadelphia, PA.

Berkhout, F. 2012. Adaptation to climate change by organizations. WIREâs Climate Change, 3(1): 91â106. https://doi.org/10.1002/wcc.154

Berrone, P., A. Fosfuri, and L. Gelabert. 2013. Necessity as the mother of âgreenâ inventions: Institutional pressures and environmental innovations. Strategic Management Journal 34 (8): 891â909. https://doi.org/10.1002/smj.2041

Breiman, L. 1996. Bagging predictors. Machine Learning 24(2): 123-140.

Cahen-Fourot, L., E. Campiglio, E. Dawkins, A. Godin and E. Kemp-Benedict. 2019. Capital stranding cascades: The impact of decarbonisation on productive asset utilisation. WU Institute for Ecological Economics Working Paper Series, 18/2019. WU Institute for Ecological Economics, Vienna.

Calabrese, R., T. Dombrowski, A. Mandel, R.K. Pace and L. Zanin. 2023. Impacts of extreme weather events on mortgage risks and their evolution under climate change: A case study on Florida. SSRN Working Papers: 1â47. https://ssrn.com/abstract=3929927

Caldecott, B. 2017. Introduction to special issue: Stranded assets and the environment. Journal of Sustainable Finance and Investment 7(1): 1â13. https://doi.org/10.1080/20430795.2016.1266748

Caldecott, B. and G. Dericks. 2018. Empirical calibration of climate policy using corporate solvency: A case study of the UKâs carbon price support. Climate Policy 18(6): 766â780. https://doi.org/10.1080/14693062.2017.1382318

Charalambakis, E.C., and I. Garrett. 2019. On corporate financial distress prediction: What can we learn from private firms in a developing economy? Evidence from Greece. Review of Quantitative Finance and Accounting 52: 467â491. https://doi.org/10.1007/s11156-018-0716-7

Clement, V., and J. Rivera. 2017. From adaptation to transformation: An extended research agenda for organizational resilience to adversity in the natural environment. Organization and Environment 30(4): 346â365. https://doi.org/10.1177/1086026616658333

Coronese, M., F. Lamperti, K. Keller, F. Chiaromonte and A. Roventini. 2019. Evidence for sharp increase in the economic damages of extreme natural disasters. Proceedings of the National Academy of Sciences of the United States of America 116(43): 21450â21455. https://doi.org/10.1073/pnas.1907826116

Coulson, A.B. 2009. How should banks govern the environment? Challenging the construction of action versus veto. Business Strategy and the Environment 18(3): 149â161. https://doi.org/10.1002/bse.584

Crutzen, N., and D. Van Caillie. 2010. Towards a taxonomy of explanatory failure patterns for small firms: A quantitative research analysis. Review of Business and Economic Literature 55(4): 438â463.

Dennis, B. 2022. Climate change and financial policy: A literature review. FEDS Working Paper 2022-48. http://dx.doi.org/10.17016/FEDS.2022.048

Du Jardin, P. 2010. Predicting bankruptcy using neural networks and other classification methods: The influence of variable selection techniques on model accuracy. Neurocomputing 73(11â12): 2047â2060. https://doi.org/10.1016/j.neucom.2009.11.034

EIB. 2021. Assessing climate change risks at the country level: The EIB scoring model. EIB Working Paper 2021/03, May, 1-21. EIB, Luxembourg.

EIOPA. 2022. European insurersâ exposure to physical climate change risk: Potential implications for non-life business. EIOPA Report 22/278, May, 1-59. EIOPA, Frankfurt am Main.

ESRB. 2016. Too late, too sudden: Transition to a low-carbon economy and systemic risk. Report of the Advisory Scientific Committee 6, European Systemic Risk Board, Frankfurt am Main.

European Central Bank. 2024. ECB guide to internal models. ECB Banking Supervision Series. https://doi.org/10.2866/286363

Fabris, N. 2020. Financial stability and climate change. Journal of Central Banking Theory and Practice 9(3): 27â43. https://doi.org/10.2478/jcbtp-2020-0034

Filipe, S.F., T. Grammatikos, and D. Michala. 2016. Forecasting distress in European SME portfolios. Journal of Banking and Finance 64: 112â135. https://doi.org/10.1016/j.jbankfin.2015.12.007

Forino, G. and J. Von Meding. 2021. Climate change adaptation across businesses in Australia: interpretations, implementations, and interactions. Environment, Development and Sustainability 23: 18540â18555. https://doi.org/10.1007/s10668-021-01468-z

Freund, Y. and R.E. Schapire. 1996. Experiments with a new boosting algorithm. In Machine learning: Proceedings of the Thirteenth International Conference. Morgan Kaufman, San Francisco, CA, pp. 148â156.

Gasbarro, F., F. Iraldo, and T. Daddi, 2017. The drivers of multinational enterprisesâ climate change strategies: A quantitative study on climate-related risks and opportunities. Journal of Cleaner Production 160: 8â26. https://doi.org/10.1016/j.jclepro.2017.03.018

Gasbarro, F. and J. Pinkse. 2015. Corporate adaptation behavior to deal with climate change: The influence of firm-specific interpretations of physical climate impacts. Corporate Social Responsibility and Environmental Management 23(3): 179â192. https://doi.org/10.1002/csr.1374

Georgopoulou, E., S. Mirasgedis, Y. Sarafidis, V. Hontou, N. Gakis, D. Lalas, F. Xenoyianni, N. Kakavoulis, D. Dimopoulos and V. ZavrasPiraeus. 2015. A methodological framework and tool for assessing the climate change related risks in the banking sector. Journal of Environmental Planning and Management 58(5): 874â897. https://doi.org/10.1080/09640568.2014.899489

Greene, W. 2017. Econometric analysis, 8th edn. Pearson, New York, NY.

Griffin, P., D. Lont, and M. Lubberink. 2019. Extreme high surface temperature events and equity-related physical climate risk. Weather and Climate Extremes 26. https://doi.org/10.1016/j.wace.2019.100220

Grillakis, M.G. 2019. Increase in severe and extreme soil moisture droughts for Europe under climate change. Science of The Total Environment 660: 1245â1255. https://doi.org/10.1016/j.scitotenv.2019.01.001

Gutiérrez-López, C., P. Castro, and M.T. Tascón. 2022. How can firmsâ transition to a low-carbon economy affect the distance to default? Research in International Business and Finance 62: 1â14. https://doi.org/10.1016/j.ribaf.2022.101722

Hsiang, S., R. Kopp, A. Jina, J. Rising, M. Delgado, et al. 2017. Estimating economic damage from climate change in the United States. Science 356(6345), 1362â1369. https://doi.org/10.1126/science.aal4369

IPCC. 2021. Climate change 2021 - the physical science basis. Contribution of Working Group I to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change. Cambridge University Press, Cambridge.

IRENA. 2017. Stranded assets and renewables: How the energy transition affects the value of energy reserves, buildings and capital stock. Working Paper based on global REmap analysis. International Renewable Energy Agency (IRENA), July.

Kim, S.Y. and A. Upneja. 2014. Predicting restaurant financial distress using decision tree and AdaBoosted decision tree models. Economic Modelling 36: 354â362. https://doi.org/10.1016/j.econmod.2013.10.005

Klusak, P., M. Agarwala, M. Burke, M. Kraemer and K. Mohaddes. 2021. Rising temperatures, falling ratings: The effect of climate change on sovereign creditworthiness. IMFS Working Paper 158. SSRN Working Paper. http://dx.doi.org/10.2139/ssrn.3811958

Labatt, S. and R.R. White. 2002. Environmental finance: A guide to environmental risk assessment and financial products. Wiley, Oxford.

Lavalle, C., F. Micale, T.D. Houston, A. Camia, R. Hiederer, C. Lazar, C. Conte, G. Amatulli and G. Genovese. 2009. Climate change in Europe. 3. Impact on agriculture and forestry. A review. Agronomy for Sustainable Development 29: 433â446. https://doi.org/10.1051/agro/2008068

Linnenluecke, M.K., A. Griffiths and M.I. Winn. 2012. Extreme weather events and the critical importance of anticipatory adaptation and organizational resilience in responding to impacts. Business Strategy and the Environment 21(1): 17â32. https://doi.org/10.1002/bse.708

Linnenluecke, M.K., A. Griffiths and M.I. Winn. 2013. Firm and industry adaptation to climate change: a review of climate adaptation studies in the business and management field. WIREâs Climate Change 4: 397â416. https://doi.org/10.1002/wcc.214

Long, S. and J. Freese. 2001. Regression models for categorical dependent variables using Stata. Stata Press, College Station, TX.

McKnight, B. and M.K. Linnenluecke. 2019. Patterns of firm responses to different types of natural disasters. Business and Society 58(4): 813â840. https://doi.org/10.1177/0007650317698946

Mengze, H. and L. Wei. 2015. A comparative study on environment credit risk management of commercial banks in the Asia-Pacific region. Business Strategy and the Environment 24(3): 159â174. https://doi.org/10.1002/bse.1810

Monasterolo, I. 2020. Climate Change and the Financial System. Annual Review of Resource Economics 12: 299â320. https://doi.org/10.1146/annurev-resource-110119-031134

Natural Capital Coalition. 2016a. Natural capital protocol. Available online at www.naturalcapitalcoalition.org/protocol

Natural Capital Coalition. 2016b. Natural capital protocol. Food and beverage sector guide. Available online at https://capitalscoalition.org/guide_supplement/food-beverage-sector-guide/

Natural Capital Coalition (NCC). 2016c. Connecting finance and natural capital. A supplement to the natural capital protocol. Available online at https://capitalscoalition.org/guide_supplement/finance-sector-supplement/

Nguyen, Q., I. Diaz-Rainey and D. Kuruppuarachchi. 2023. In search of climate distress risk. International Review of Financial Analysis 85: 1â26. https://doi.org/10.1016/j.irfa.2022.102444

Nyberg, D., G. Ferns, S. Vachhani and C. Wright. 2022. Climate change, business, and society: Building relevance in time and space. Business and Society 61(5): 1322â1352. https://doi.org/10.1177/00076503221077452

Ouazad, A. and M. Kahn. 2021. Mortgage finance and climate change: Securitization dynamics in the aftermath of natural disasters. NBER Working Paper. NBER, Cambridge, MA.

Romilly, P. 2007. Business and climate change risk: A regional time series analysis. Journal of International Business Studies 38(3): 474â480. https://doi.org/10.1057/palgrave.jibs.8

Sun, J., H. Li, Q.H. Huang and K.Y. He. 2014. Predicting financial distress and corporate failure: a review from the state-of-the-art definitions, modeling, sampling, and featuring approaches. Knowledge-Based Systems 57: 41â56. https://doi.org/10.1016/j.knosys.2013.12.006

Sutanto, S.J., C. Vitolo, C. Di Napoli, M. DâAndrea and H.A.J. Van Lanen. 2020. Heatwaves, droughts, and fires: Exploring compound and cascading dry hazards at the pan-European scale. Environment International 134: 1â10. https://doi.org/10.1016/j.envint.2019.105276

Teuling, A.J. 2018. A hot future for European droughts. Nature Climate Change 8 : 364â365. https://doi.org/10.1038/s41558-018-0154-5

Tian, S., Y. Yu and H. Guo. 2015. Variable selection and corporate bankruptcy forecasts. Journal of Banking and Finance 52: 89â100. https://doi.org/10.1016/j.jbankfin.2014.12.003

Turco, M., M.C. Llasat, J. von Hardenberg and A. Provenzale. 2014. Climate change impacts on wildfires in a Mediterranean environment. Climatic Change 125(3): 369â380, https://doi.org/10.1007/s10584-014-1183-3

UNEP FI. 2002. Climate change and the financial services industry: Module 2 â A blueprint for action. UNEP FI, Geneva.

UNEP FI. 2007. Banking on value: A new approach to credit risk in Africa. UNEP FI, Geneva.

Wang, G., J. Ma, L. Huang and K. Xu. 2012. Two credit scoring models based on dual strategy ensemble trees. Knowledge-Based Systems 26: 61â68. https://doi.org/10.1016/j.knosys.2011.06.020

Weber, O. 2005. Sustainability benchmarking of European banks and financial service organizations. Corporate Social Responsibility and Environmental Management 12(2): 73â87. https://doi.org/10.1002/csr.77

Weber, O. 2012. Environmental credit risk management in banks and financial service institutions. Business Strategy and the Environment 21(4): 248â263. https://doi.org/10.1002/bse.737

Weber, O., M. Fenchel, and R.W. Scholz. 2008. Empirical analysis of the integration of environmental risks into the credit risk management process of European banks. Business Strategy and the Environment 17(3): 149â159. https://doi.org/10.1002/bse.507

Weber, O., R.W. Scholz and G. Michalik. 2010. Incorporating sustainability criteria into credit risk management. Business Strategy and the Environment 19(1), 39â50. https://doi.org/10.1002/bse.636

White, M.A. 1996. Environmental finance: Value and risk in the age of ecology. Business Strategy and the Environment 5(3): 198â206. https://doi.org/10.1002/(SICI)1099-0836(199609)5:3<198::AID-BSE66>3.0.CO;2-4

Winn, M., M. Kirchgeorg, A. Griffiths, M. Linnenluecke and E. Gunther. 2011. Impacts from climate change on organizations: A conceptual foundation. Business Strategy and the Environment 20(3): 157â173. https://doi.org/10.1002/bse.679

Zhang, F. 2022. Not all extreme weather events are equal: Impacts on risk perception and adaptation in public transit agencies. Climatic Change 171: 1â21. https://doi.org/10.1007/s10584-022-03323-0

Appendix

List of variables

Citation: International Food and Agribusiness Management Review 28, 1 (2025) ; 10.22434/ifamr1170

Correlation analysis of full sample.

Citation: International Food and Agribusiness Management Review 28, 1 (2025) ; 10.22434/ifamr1170

Correlation analysis of healthy firms.

Citation: International Food and Agribusiness Management Review 28, 1 (2025) ; 10.22434/ifamr1170

Correlation analysis of failed firms

Citation: International Food and Agribusiness Management Review 28, 1 (2025) ; 10.22434/ifamr1170

Corresponding author

Some characteristics make climate risks different from other financial risks: non-linear impacts, forward-looking nature, large uncertainty, and complexity due to heterogeneous agentsâ behaviour (Linnenluecke et al., 2013).

The Mediterranean Area of the European Union comprises regions in the Mediterranean basin, including the following member countries (some partially): Bulgaria, Cyprus, Croatia, France, Greece, Italy, Malta, Portugal, Slovenia and Spain. Notably, Greece was initially considered in our selection; however, it was ultimately excluded due to the low quality of available data. The rest of the EU countries in the Mediterranean area were excluded from the sample due to insufficient data.

âFire weatherâ alludes to weather conditions triggering and sustaining wildfires. As global warming intensifies, scientists estimate more frequent fire weather conditions in the Mediterranean area with high confidence (IPPC, 2021, p. 1600).

The abovementioned variables are identified in the equation as CRP, a climate risk variable proxy that includes MAX_TEMP, PRECIPI and FIRES.

In non-tabulated results we obtain values lower than 2 for the Variance Inflation Factor (VIF) in all models, indicating the absence of multicollinearity between the studied variables.

We re-estimate the model by using probit and obtain similar results that support our hypotheses (results available upon request).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}